A bloggable insight: Itamar Drechsler, and Qingyi F. Drechsler "The Shorting Premium and Asset Pricing Anomalies." They carefully found the cost to short-sell stocks.

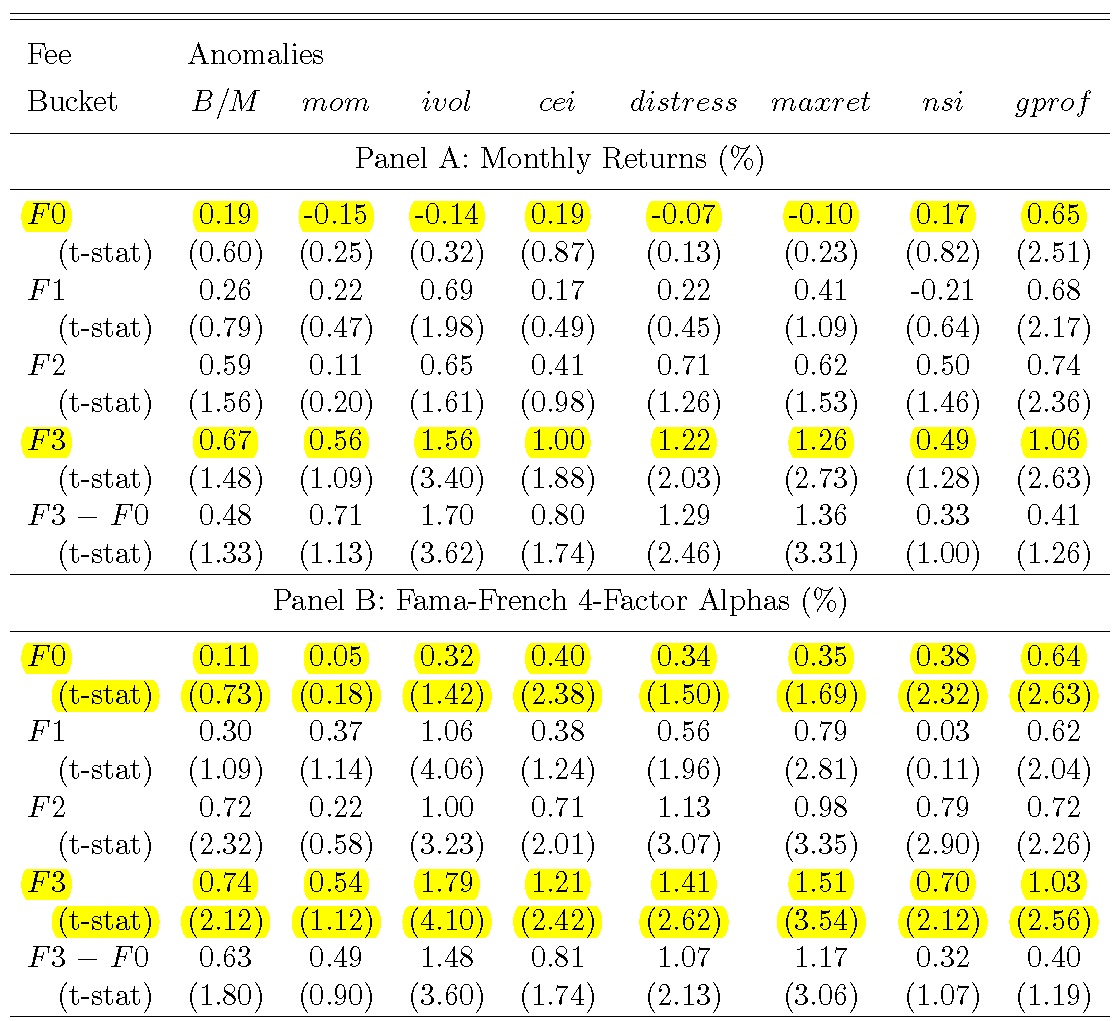

Here's their Table 5. F0 are all the easy to short stocks. F3 are the hardest to short stocks. They construct long-short anomaly portfolios in each group. "F 0 Mom" for example is the average monthly return of past winners minus that of past losers, among the easy to short stocks. Now compare the F0 row to the F3 row. The anomaly returns only work in the hard-to-short portfolios.

The second panel shows Fama-French alphas, which are better measured. The sample is alas small. But the result is cool.

The implication is that a lot of anomalies exist only in hard to trade stocks. There is a lot more in the paper, of course.

Table 5: Anomaly Returns Conditional on Shorting Fees

We divide the short-fee deciles from Table 2 into four buckets. Deciles 1-8, the low-fee stocks, are placed into the F0 bucket. Deciles 9 and 10, the intermediate- and high-fee stocks, are divided into three equal-sized buckets, F1 to F3, based on shorting fee, with F3 containing the highest fee stocks. We then sort the stocks within each bucket into portfolios based on the anomaly characteristic and let the bucket's long-short anomaly return be given by the di erence between the returns of the extreme portfolios. Due to the larger number of stocks in the F0 bucket, we sort it into deciles based on the anomaly characteristic, while F1 to F3 are sorted into terciles. Panel A reports the monthly anomaly long-short returns for each anomaly and bucket. Panel B reports the corresponding FF4 alphas. Panel C reports the FF4 + CME alphas. The sample period is January 2004 to December 2013.

(From Table 4 caption) The anomalies are: value-growth (B=M), momentum (mom), idiosyncratic volatility (ivol), composite equity issuance (cei), nancial distress (distress), max return (maxret), net share issuance (nsi), and gross pro tability (gprof). The sample is January 2004 to December 2013.

John,

ReplyDeletea) Is looking at the anomalies within different “hard vs. easy to short buckets” the right way, or would you rather look at it broadly (as people implement it) and adjust for (remove, place a higher cost on) the harder to short guys? While perhaps indicative, perhaps not, it doesn’t seem that how well anomalies work entirely long and short within these buckets is the point.

b) My more important point (to me!), and admittedly this is an old obsession of mine, you highlight momentum as your example in your text (perhaps just to explain the table but still singling it out). In the actual tables (raw or 4-factor) it actually holds decently better (F3 – F0 t-stat) than the other anomalies (“nsi” is close). For some reason we don’t understand, people keep finding things (e.g., factors work better in small caps!) and using momentum as their poster child, often (though not in this particular case) even completely leaving out the other factors even if the issue is bigger there! At the least this leaves the implication it’s a bigger problem for momentum when the truth seems often, or even usually, to be the opposite. I’m baffled as to why… We had thought we had put this bias to bed (regarding many other issues not this study of shorting costs) with the paper referred to in this brilliant blog entry http://johnhcochrane.blogspot.com/2014/05/aqr-on-momentum.html... :)

-- Cliff Asness

Within asset pricing literature, I was wondering why not more researchers are mentioning long only (and short only for that matter) results? And for example turnover figures?

ReplyDeleteThe title of your post is timeless and has been a source of inspiration to me. Factors are useful, but how can we go about judging whether the price is likely to be efficient?.

ReplyDelete