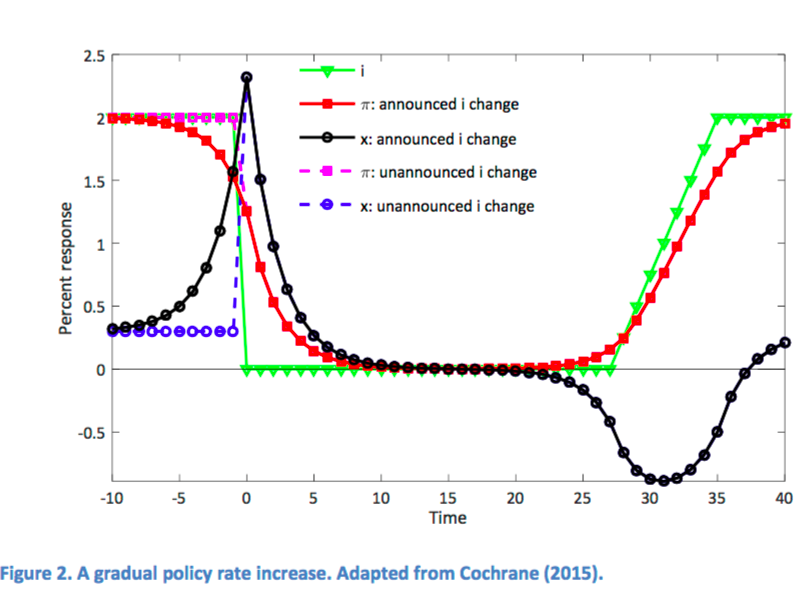

Jim starts with this great picture. It's a simulation of the standard three equation new Keynesian model as we go from 2% interest rate to zero. This is an upside down version of the first graph in my "Do higher interest rates raise or lower inflation." (Blog post) But Jim makes a new and insightful point with it, that had not occurred to me.

Jim reads this as an account of what happened in 2008, not (my) tentative prediction for what might happen in 2016 in the other direction. It's compelling: The Fed lowers rates. This boosts output (black line) over what it would otherwise be, overcoming the horrendous negative shocks to the economy from a financial crisis. Inflation gently declines, which is also what inflation did after a one time shock in 2009, related to the output shock which the Fed was offsetting.

Jim then ties that together with my Figure 3 in an artful way. The same model that accounts well for slow disinflation in the recovery suggests that raising rates now, in the absence of other shocks, would just raise inflation and lower output.

Jim goes on to present some data averaged across a variety of countries. Here you see a pattern quite similar to the model's prediction. After recovering from the severe shock, inflation starts its gentle decline.

Like me, Jim is nervous about these conclusions. The data seem to be telling us that interest rate pegs are not unstable. The standard model turns out to have that prediction, but also predicts that raising interest rates, while lowering output as we have long been told, will just smoothly raise inflation. It's very hard to turn around decades of contrary doctrine -- that pegs are unstable, and raising rates lowers inflation. One should be nervous about such conclusions. Maybe inflation is, finally, just around the corner. So Jim makes very clear he's not yet recommending a rate rise to cause more inflation!

But one should also start thinking about what these conclusions mean if they are right, and Jim summarizes with a number of such implications. A few that seem especially important, with comment:

Third, longer‐run economic growth would still be driven by human capital accumulation and technological progress, as always, but without the accompanying stabilization policy as conventionally practiced from 1984‐2007. In principle, the economy would still be expected to grow at a pace dictated by fundamentals.A little more bluntly, Japan-bashers cannot blame 20 years of poor growth on the zero bound. Nor should we worry that permazero will cause lower growth. (The other way around is much more likely: low marginal product of capital leads to low rates.) Japan's growth and inflation, like our own for the last seven years, has also been quite stable, raising the next question of just how much stabilization this policy was doing.

Fourth, the celebrated Friedman rule would arguably be achieved, so that household and business cash needs are satiated. In many monetary models this is a desirable state of affairs.Yes!! Shout it from the rooftops.

Just what is so terrible about zero rates and very low inflation? Zero rates are the optimum quantity of money. They have financial stability benefits too. Banks sitting on huge piles of cash don't go under.

Conventional modeling has been treating the zero bound as a "trap," or a terrible outcome to be avoided. But it's a honey trap, at least in these models. The main complaint one could make is that they don't last, that they lead to spiraling deflation or hyperinflation. But the models said "trap" -- they last -- and the data seem to agree.

Fifth, the risk of asset price fluctuations may be high. In the New Keynesian model, the near‐zero interest rate policy with little or no response to incoming shocks is associated with equilibrium indeterminacy. This means there are many possible equilibria, all of which are consistent with rational expectations and market clearing. In a nutshell, a lot of things can happen. Many of the possible equilibria are exceptionally volatile. One could interpret this theoretical situation as consistent with the idea that excessive asset price volatility is a risk.This is spot on. In the models, the trouble with the zero bound "trap" is not high unemployment, low growth, or spiraling inflation or deflation -- it has none of these. The problem is "indeterminacy," the possibility that inflation can bounce around a bit, each time returning stably back again. That's also what we seem to see, and it hasn't been a huge problem: We don't see any more inflation, output, or asset market volatility in the last 7 years than in the period before the crisis.

And this is a simple problem to solve in the theory. Add back the missing fiscal theory of the price level -- deliberately thrown out in the theory -- and you have determinacy again. In words, a jump to an alternative equilibrium requires that fiscal policy expectations also jump. If people's expectations of long-term fiscal policy are stable, then we have determinacy and no more volatility at the zero bound too.

Sixth, and finally, the limits on operating monetary policy through ordinary short‐term nominal interest rate adjustment in this situation would surely continue to fire a search for alternative ways to conduct monetary stabilization policy. The favored approach during the past five years within the G‐7 economies has been quantitative easing, and there would surely be pressure to use this or related tools.I.e. in permazero, eventually markets get tired of reacting to whispers that the Fed might someday raise rates. Monetary policy overall becomes ineffective, leading central banks to try other levers. Which may not be such a great idea!

With this article you imply that what has happened is a good thing. No discussion of effects on savers, elderly, declining birth rates, or huge expansion of government. It seems that academic economists seem to believe that the Fed can do no wrong and have no effect on the people. Why no discussion of these issue? Too complicated or political?

ReplyDeleteI can't do everything in one blog post.

DeleteBeing a relatively uninformed follower ... It seems that all this zero rates (and I hear talk of minus zero as well), and the National Debt whether we pay it down or continue to let it grow, lead me and David to the same place ... how does all this effect what we have spent our lives saving?

DeleteThe Fed can do wrong. The Fed may also be able to do good. Honestly, though, it is not the proper function of the Fed to do good or to do evil; it is the function of the Fed to determine the proper amount of money in the system. Regardless of congressional mandates, it is the proper fumcion of Congress, elected by the people, to make policy decisions. Why should Congress be spared the effects of policy if the Federal Reserve is actively reversing those decisions?

DeleteArtificially low rates also increase the present value of future liabilities, so that pensions funds and social security are all more underfunded than they need to be. Let the market decide!

ReplyDeleteIt's possible - actuarially - for the same average return to be reached by 2 pension funds where one of the 2 incurs losses at the start of the period while the other incurs the same losses towards the end of the period, with the same profits, inverted, and have the fund with the early losses end up bankrupt. This is a little-understood function of exponentials but it's real and that's what worries me on the federal debt - when do we recognize contingent and accrued liabilities?

DeleteAs in your previous posts, you write the NK model assuming that the natural rate is zero at equilibrium (in your post http://johnhcochrane.blogspot.fr/2015/08/whither-inflation.htmlwriting the intertemporal IS equation (1), you should have the natural rate) ... I was wondering whether it affects your simulations in any way.

ReplyDeleteAll of these graphs are impulse-response functions -- how much inflation and output change if monetary policy changes. So a positive natural rate, or other shocks, make no difference to the plots, since they are the same under the old and new monetary policy. Granted, I didn't make that clear.

DeleteThe reason why zero rates are called "Trap" is that rate cannot go below zero, at least not much. So in case of crisis, you can only go up. If rates are at, let's say 4%, and economy is doing well, you can go to 0% (in case of demand crisis) or 8% (in case of overheating) and produce some soothing effect. That means that impact of the crisis, mostly on most needy, will be harder if there is no maneuvering space.

ReplyDelete"The reason why zero rates are called "Trap" is that rate cannot go below zero, at least not much."

DeleteIs that true even after you allow for effective exchange rate premium or discount, whether officially quoted or not? Looking at the Swiss franc, bond buyers have been buying long Swiss franc-denominated bonds in the belief that by the time they pay back principal, the franc will have appreciated sufficiently to more than make up for the low interest coupon. This is an observation made at least since Keynes (on the unique determination of the forward rate once the interest rate is known for credits of equal risk, and as a result Swiss borrowers have in effect been paying heavily negative rates though they do lose out on principal repayments. I wonder whether it's a numeraire differential blinding us in the calculations.

I'm a software developer and I started reading economics blogs just after the financial crisis / mobile app gold rush. I wanted to make a mobile game with a realistic macroeconomics simulation. I didn't realize how far the rabbit whole went and never finished the game. It was going to have some kind of monte carlo simulation of agents, firms, government and central bank.

ReplyDeleteRecently I had a bit of spare time and I thought maybe I could have a go at it again. I almost bought Woodford's textbook to get some ideas. But I got stuck again with this whole Neo-Fisherian debate.

For what it's worth, looking at the different moving parts of my little simulation, I reached the same conclusion:

When excess reserves start to accumulate at the ZLB and the amount of money in the economy gets too disconnected from the amount useful as liquidity for day to day transactions. The value of this stock of idle money is, in a very tautological way, essentially worth whatever people think it's worth .

There isn't anything substantial enough to anchor the value of vast amount of idle cash disconnected from economic activity.

This is another hurdle to finishing my simulation as it boils down to money's worth being determined mostly by human psychology and I am unsure how to simulate that.

The only lesson I can draw here is that central banks should never allow this to happen or they risk losing control. Inflation should always be kept high enough that the economy never accumulates an excessive amount of idle reserves.

Well...okay if the central banks can hold interest rates at zero and thereby tame inflation, it seems the next step is aggressive QE and to seek extremely low unemployment rates or even "labor shortages."

ReplyDeleteAfter all, it has also been doctrine for generations that we must tolerate unemployment to tame inflation.

One question: if property zoning is universal in cities, and the supply of housing is restricted, how can we not see inflation in housing, yet robust economic growth? And if housing is 40% of PCE price index....

Does not this fit NGDP targeting? The economy is at the optimal quantity. There is real growth. After a while, because there was growth, agents collectively hold more cash balances, therefore the monetary authority does monetary policy by doing another round of QE. The "thermometer" is stable NGDP growth.

Delete

ReplyDeleteWhat your doing isn't even close to science.

Regarding your paper, I think one fruitful place to look for why raising rates might initially reduce inflation is in term debt. I included some long term debt (in the form of annuities) into your model and looked at the impact of an unexpected increase in rates.

ReplyDeletehttp://monetaryreflections.blogspot.co.uk/2015/11/neo-fisherism-and-term-debt.html

How would this model apply to the strange phenomena listed in this article?

ReplyDeletehttp://www.bloomberg.com/news/articles/2015-11-12/five-strange-things-that-have-been-happening-in-financial-markets

1. Negative swap spreads

ReplyDelete2. Fractured repo rates

3. Corporate bond inventories below zero

4. Synthetic credit is trading tighter than cash credit

5. Market moves that aren't supposed to happen keep happening

6. Volatility is itself more volatile

This is the list of the strange phenomena, at least 2 is explained by previous writings of prof. Cochrane where he notes counterparty risk is also important, but the others are harder to explain.

Perhaps the interest rate is only the supply versus demand for debt?

ReplyDeleteZero interest rates (high priced debt / low yielding) are symptomatic of a limited debt supply versus a high demand for debt. Income is scarce at the zero lower bound, in other words.

Expansionary monetary policy is supposed to increase nominal incomes. Higher interest rates are a consequence of expansionary monetary policy, not a cause. On the other hand, low interest rates are symptomatic of tight money and scarce income.

Interest rates are mere symptom of monetary policy, not a cause. How do central banks price-fix short term interest rates? Debt versus the monetary base versus nominal output should be the modelling agenda.

By definition the interest rate is the price of credit so if the interest rate for zero-risk credit is itself zero or negative the thing to do is look at what the higher-risk creditors have to pay, of course denominated in the same currency. Catastrophe bonds are a useful benchmark http://query.nytimes.com/gst/fullpage.html?res=9C05E1DE103FF935A1575BC0A9619C8B63&pagewanted=all

DeleteYour 1-6 strange phenomena are all symptoms of low liquidity in financial markets, i.e. homogeneous balance sheets. Heterogeneous balance sheet positions drive heterogeneous opinions and investments -- weak hands sell to strong hands, which is liquidity. Heterogeneity = liquidity.

DeleteZero interest rates suggest homogeneous overleveraged balance sheets -- the marginal borrower is already indebted and all leveraged up. When everybody is overleveraged, everyone is a weak hand, and there is little secondary liquidity in the marketplace.

The solution? Reverse the current stance of monetary policy:

Tight monetary policies slow nominal growth and lower interest rates. Income-generating asset prices rise, and balance sheets lever up.

Expansionary monetary policy would boost nominal growth, raise interest rates, damage asset prices, and deleverage governments, consumers, and business.

John, would you say you share Jim's "framework?" What is your framework anyway? (Here's a summary of recently blogged about frameworks)

ReplyDelete