The Social Security Trust fund is set to run out in a few years. Who cares? Is the total US Federal debt $31,456,554,630,496.28, including Treasury debt held by the Social Security trust fund and other agencies? or is it "only" $24,629,050,125,670.81 held by the public? (Source.)

I've been mulling these questions over, prodded by conversations with some colleagues.

The "trust fund" exists because for a while, Social Security taxes were larger than Social Security payments. Social Security used the extras to buy Treasury debt. Now there are fewer workers, more retirees and more generous benefits, so Social Security taxes are smaller than payments. Social Security sells off its "trust fund." And it seems we're in trouble when the "trust fund" runs out.

But that's not how it works at all. Treasury debt is not an asset like a stock or bond, or Uncle Scrooge's pool of gold coins. Treasury debt is a claim against future income taxes. Cashing in Treasury debt just means paying for benefits with income taxes.

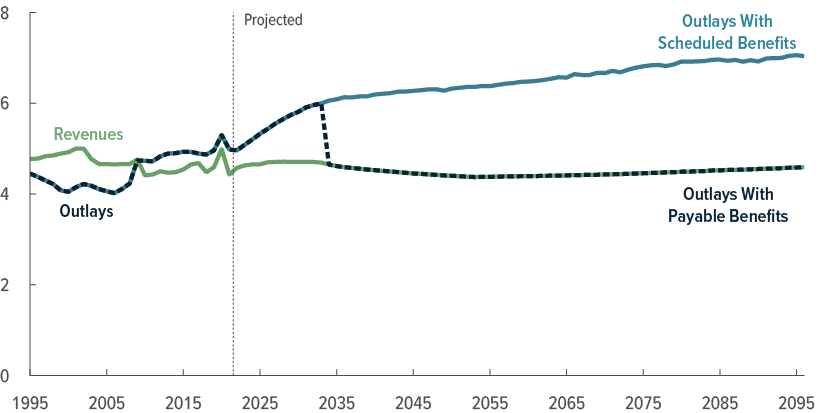

The ups and downs of the trust fund just reflect a change in how we finance spending. While payroll taxes > social security spending, which was the case until 2007, then payroll taxes are financing other spending. When payroll taxes < social security spending, then income taxes or increases in debt are financing social security spending, which (graph below) was the case after 2008.* The trust fund just adds up this change over time. But exhausting the trust fund is, in this view, really irrelevant.

That doesn't mean we can all go to sleep, for two reasons. First, when payroll taxes < Social Security outlays, and the trust fund is winding down, then income taxes or additional public debt must finance the shortfall. The government has to spend less on other things, raise income tax receipts, or borrow which means raising future taxes. And, per the graph, the numbers are not small. 1% of GDP is $230 billion. The extra strain on income taxes, other spending, or debt, happens right now, when the trust fund is positive but decreasing.

Zero matters only because by law, when the trust fund goes to zero, Social Security payments must be automatically cut to match Social Security taxes. That's the sudden drop in the graph. The program was set up as if the trust fund were buying stocks and bonds, real assets, and would not lay claim on income tax revenues. But it was not; social security taxes were used to cover other spending, and now income taxes must start to pay social security benefits.

What happens when the trust fund runs out, then? Congress has a choice: automatically cut benefits, as shown, or change the law so that the government can pay Social Security benefits from income taxes, or, more realistically, by issuing ever more debt, until the bond vigilantes come. (Or raise payroll taxes, or reform the whole mess.) I bet on change the law.

So what's the right measure of debt? It's conventional to look only at debt in public hands. But there is a case to look at the total debt, i.e. including the trust funds. Those are the total claims against the income tax. Looking at it this way, however, one could also go on and count unfunded future social security benefits as a debt -- the present value of the difference between the two lines above, which leads to immense numbers, per Larry Kotlikoff.

I have usually not considered the present value of unfunded promises as "debt," because Congress can change the payments at any time. Changing debt repayment to the public is a default, with financial and legal consequences; changing social security benefits is legislation. You can't sell your future social security benefits as you can sell your treasury debt. The trust fund is half way on this scale. What would be the consequence of a haircut or rescheduling of trust fund debt? Would that trigger something like cross-default clauses in corporate debt? I don't know. The event is unlikely anyway. The left pocket defaulting on the right pocket doesn't help pay the bills. The trust fund is certainly unlikely to run, and its debt is not used as collateral in financial transactions. As a somewhat meaningless accounting identity, it's a lot less "debt" than the debt in public hands.

I think this all goes to remind us that paying off the existing debt is not the US central fiscal problem. The central problem is vast unfunded future promises. Defaulting or inflating away current debt does nothing to fund those promises.

I look forward to comments on this one, especialy if there are standard views on these apparently simple questions that I'm not aware of.

*In the end,

payroll taxes + income & other taxes + increase in public debt = Social Security spending + other spending.

The trust fund nets out.