With President Milei's election in Argentina, dollarization is suddenly on the table. I'm for it. Here's why.

Showing posts with label Trade. Show all posts

Showing posts with label Trade. Show all posts

Friday, November 24, 2023

Tuesday, May 24, 2022

Sloar panel tariffs

T.J Rodgers in the Wall Street Journal is classic:

Solar panels are key to the transition to carbon-free energy. Since the Earth will be unlivable due to the climate catastrophe if we don't move now, at least according to the Administration, you would think they would be doing everything to encourage solar panel installation. Since mother Gaia does not care where panels are produced, you would think the Administration would not either. If China can produce them cheaper, all the better for the Earth. If China wants to tax its citizens to subsidize our solar panels better still. It's the least they could do in return for adding a new coal-fired power plant about once a week. You would be wrong. Our policy is

a punitive 2012 tariff levied by the U.S. Commerce Department.

That raises the price substantially:

Our politicians disingenuously campaign for conversion to solar energy, but their propensity for top-down economic controls is forcing American homeowners to pay $2.65 per watt on average to install a residential solar system today, according to Clean Energy Associates. The equivalent fully installed residential solar costs are $1.50 in Europe, $1.25 in Australia and $1 in India—because these places practice, and get the benefits of, free-market capitalism in their solar markets.

Oh, those pesky free-market capitalists in Europe, Australia and India.

Saturday, April 16, 2022

Regulatory capture: trucking edition

Dominic Pino has a lovely National Review article on Mexican trucks. Watch the sausage in the making. Excerpts with commentary

Congress banned Mexican truckers from entering the U.S. in 1982. NAFTA, which came into effect in 1994, committed the U.S. to removing that restriction by 2000.

1994 was 28 years ago.

The U.S. left the restriction in place anyway, and was found to be in violation of the agreement in 2001... The Bush administration said it would remove the restriction.

But organized labor and environmental groups...sued to keep the restriction in place. The environmentalists claimed that Mexican trucks did not meet American safety and environmental regulations. The Teamsters and other unions had an obvious motive: keeping out the competition....

In 2004.. the Supreme Court ruled against the environmentalists and unions and said that the Bush administration could remove the restriction and bring the U.S. in line with its obligations under NAFTA. Clarence Thomas wrote for the unanimous court.

Unanimous.

Wednesday, March 9, 2022

Irwin on trade reform

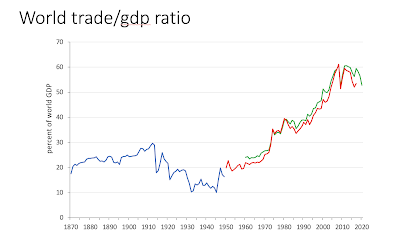

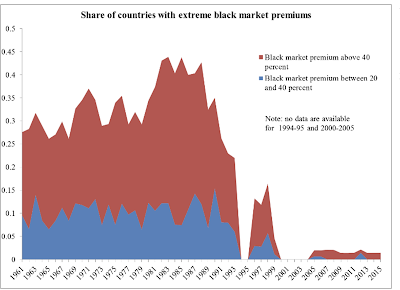

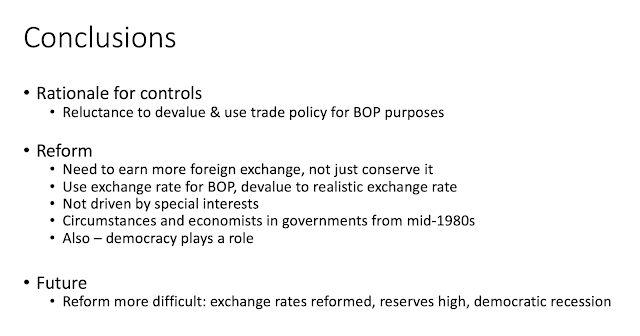

Doug Irwin of Dartmouth gave a really informative talk at the Hoover Economic Policy Working Group, based on his paper The Trade Reform Wave 1985-1995, AER May 2022. Embed (hopefully) below, or go to the link here.

Doug opened my eyes, hence this post. I love learning something new. I'm a resolute Free Trader. So, naturally, I jump to the answer: Stop protecting industries. Get rid of tariffs. Don't bother with the negotiated mercantilism of trade deals -- the "you can sell to us if our exporters can sell to you" deals. The point of a foreign country's exports is to get dollars, and the point of dollars is for them to buy from the US. Full stop.

Doug reveals that this story is far too simplistic to understand the closed economies of the 1950s through 1970s, and the great trade liberalization that the world experienced starting in the 1980s -- and which we are very sadly likely to lose in the years ahead. A little reminder of what we gained, and a sad peak:

The process of liberalization started with money, not tariffs: Countries first devalued overvalued currency, usually to a floating rate. Then they eliminated quantitative restrictions on imports including import licenses. Then they reduced tariffs.

In turn, how did they get there, and why did they not reform earlier? The standard story pits domestic industry vs. consumers. Domestic industries have concentrated interest in protection, consumers are diffuse. That accounts for status quo bias, but not why they eventually changed.

The source of the problem, and reason for the change is different. Countries (especially in the "developing" world) were hit with a "terms of trade" shock -- they exported commodities, say, to import goods; the commodity price went down so they could not buy imports. Many countries were financing imports with foreign aid and borrowing, and those transfers dried up.

What do they do? They have to choose between deflation, currency depreciation, or import controls. Deflation at the same exchange rate makes foreign goods more expensive. Depreciation does the same, without changing the domestic price level. Or, stop imports by direct controls, and by rationing foreign exchange leading to a black market. In the early postwar view, consistent with Bretton Woods, they chose the latter. (Why is there so much nostalgia for Bretton Woods? It was a rotten system.)

Naturally, it didn't work. Eventually they gave up and devalued or floated the exchange rate. Now there is no need to ration foreign exchange or to restrict imports by license. (Tariffs are bad, but quantitative restrictions are worse, since you never know what the cost is, and then imports are allocated by political rather than economic reasons. Just paying a tax is more efficient!) They moved to exports in order to generate foreign exchange to buy imports.

So, Doug answers the central question:

Why no reform in 1970s? “foreign exchange reserves kill the will to reform”

Oil and commodity export countries were flush with cash to buy imports. Foreign aid recipients had cash to buy imports.

Why reform in 1980s?

Era of scarce foreign exchange – all three BOP shocks.

Goal: increase foreign exchange earnings by increasing exports.

Learning from experience – cost of import controls, benefit of exports

Shift from import repression to export promotion to overcome foreign exchange shortage

And, later,

Michael Bruno (World Bank): “We did more for Kenya by cutting off aid for one year than by giving them aid for the previous three decades”

Aid lets a country put off reform.

I asked one question, about the importance of an open capital account. That also used to be gospel, now under debate. Doug's answer was interesting: In these cases, a free currency market was crucial, but free capital markets less so.

Ideas matter.

This process did not just play out in standard political economy terms, one interest group gains power over another. The shift of ideas in universities, the IMF, central banks, and countries was crucial. I find this heartwarming as a producer of ideas, and terrifying as I watch these successful ideas crumble around me.

Doug discusses the process of reform in Mexico, (which first had disaster under some bad ideas, then reform when a new group of economists came in), India, South Korea and others. Listen to the talk!

Concluding slide:

Thursday, March 3, 2022

Time for Supply

At Project Syndicate essay, with Jon Hartley. It's not the first, and it won't be the last on the issue!

Now that surging inflation has refocused everyone's attention on the long-ignored supply side of the economy, the question is how best to support broad-based growth, efficiency, and innovation. The answer is not necessarily deregulation, but the need for smarter regulation is increasingly apparent – even to progressives.

STANFORD – The return of inflation is an economic cold shower. Governments can no longer hope to solve problems by throwing money at them. Economic policy must now turn its attention to supply and its cousin, economic efficiency.

The issue is deeper than delayed goods deliveries and a year’s worth of sharp price increases. From the end of World War II to 2000, US real (inflation-adjusted) GDP per capita grew 2.3% per year, from $14,171 to $44,177 (in 2012 dollars). Americans became healthier, lived longer, reduced poverty, and paid for a much cleaner environment and a vast array of social programs. But since 2000, that post-war growth rate has fallen almost by half, to 1.4% per year. And it’s worse in Canada and Europe, where many countries have not grown at all since 2010 on a per capita basis.

Nothing matters more for human flourishing than long-term economic growth. So, no economic trend is more worrisome than growth falling by half, especially for the well-being of the less fortunate.

The eruption of inflation settles a long debate. Sclerotic growth is not the result of demand-side “secular stagnation,” fixable only with massive fiscal and monetary stimulus. Sclerotic growth is a supply problem. We need policies to increase the economy’s productive capacity – either directly or by reducing costs.

How? The simplest and most important thing governments can do is to get out of the way. Byzantine regulations and capricious regulatory authorities stymie business. We do not need thoughtless deregulation, but rather smarter regulation that is simple, effective, avoids disincentives and unintended consequences, and is not distorted to protect current business and prop up regulatory empires. That means adding sunset clauses to regulations, regularly re-evaluating existing measures, and instituting a right to external appeal.

Monday, October 25, 2021

Supply

The Revenge of Supply, at Project Syndicate

Surging inflation, skyrocketing energy prices, production bottlenecks, shortages, plumbers who won’t return your calls – economic orthodoxy has just run smack into a wall of reality called “supply.”

Demand matters too, of course. If people wanted to buy half as much as they do, today’s bottlenecks and shortages would not be happening. But the US Federal Reserve and Treasury have printed trillions of new dollars and sent checks to just about every American. Inflation should not have been terribly hard to foresee; and yet it has caught the Fed completely by surprise.

The Fed’s excuse is that the supply shocks are transient symptoms of pent-up demand. But the Fed’s job is – or at least should be – to calibrate how much supply the economy can offer, and then adjust demand to that level and no more. Being surprised by a supply issue is like the Army being surprised by an invasion.

The current crunch should change ideas. Renewed respect may come to the real-business-cycle school, which focuses precisely on supply constraints and warns against death by a thousand cuts from supply inefficiencies. Arthur Laffer, whose eponymous curve announced that lower marginal tax rates stimulate growth, ought to be chuckling at the record-breaking revenues that corporate taxes are bringing in this year.

Equally, one hopes that we will hear no more from Modern Monetary Theory, whose proponents advocate that the government print money and send it to people. They proclaimed that inflation would not follow, because, as Stephanie Kelton puts it in The Deficit Myth, “there is always slack” in our economy. It is hard to ask for a clearer test.

But the US shouldn’t be in a supply crunch. Real (inflation-adjusted) per capita US GDP just barely passed its pre-pandemic level this last quarter, and overall employment is still five million below its previous peak. Why is the supply capacity of the US economy so low? Evidently, there is a lot of sand in the gears. Consequently, the economic-policy task has been upended – or, rather, reoriented to where it should have been all along: focused on reducing supply-side inefficiencies.

One underlying problem today is the intersection of labor shortages and Americans who are not even looking for jobs. Although there are more than ten million listed job openings – three million more than the pre-pandemic peak – only six million people are looking for work. All told, the number of people working or looking for work has fallen by three million, from a steady 63% of the working-age population to just 61.6%.

We know two things about human behavior: First, if people have more money, they work less. Lottery winners tend to quit their jobs. Second, if the rewards of working are greater, people work more. Our current policies offer a double whammy: more money, but much of it will be taken away if one works. Last summer, it became clear to everyone that people receiving more benefits while unemployed than they would earn from working would not return to the labor market. That problem remains with us and is getting worse.

Remember when commentators warned a few years ago that we would need to send basic-income checks to truck drivers whose jobs would soon be eliminated by artificial intelligence? Well, we started sending people checks, and now we are surprised to find that there is a truck driver shortage.

Practically every policy on the current agenda compounds this disincentive, adding to the supply constraints. Consider childcare as one tiny example among thousands. Childcare costs have been proclaimed the latest “crisis,” and the “Build Back Better” bill proposes a new open-ended entitlement. Yes, entitlement: “every family who applies for assistance … shall be offered child care assistance” no matter the cost.

The bill explodes costs and disincentives. It stipulates that childcare workers must be paid at least as much as elementary school teachers ($63,930), rather than the current average ($25,510). Providers must be licensed. Families pay a fixed and rising fraction of family income. If families earn more money, benefits are reduced. If a couple marries, they pay a higher rate, based on combined income. With payments proclaimed as a fraction of income and the government picking up the rest, either prices will explode or price controls must swiftly follow. Adding to the absurdity, the proposed legislation requires states to implement a “tiered system” of “quality,” but grants everyone the right to a top-tier placement. And this is just one tiny element of a huge bill.

Or consider climate policy, which is heading for a rude awakening this winter. This, too, was foreseeable. The current policy focus is on killing off fossil-fuel supply before reliable alternatives are ready at scale. Quiz: If you reduce supply, do prices go up or go down? Europeans facing surging energy prices this fall have just found out.

In the United States, policymakers have devised a “whole-of-government” approach to strangle fossil fuels, while repeating the mantra that “climate risk” is threatening fossil-fuel companies with bankruptcy due to low prices. We shall see if the facts shame anyone here. Pleading for OPEC and Russia to open the spigots that we have closed will only go so far.

Last week, the International Energy Agency declared that current climate pledges will “create” 13 million new jobs, and that this figure would double in a “Net-Zero Scenario.” But we’re in a labor shortage. If you can’t hire truckers to unload ships, where are these 13 million new workers going to come from, and who is going to do the jobs that they were previously doing? Sooner or later, we have to realize it’s not 1933 anymore, and using more workers to provide the same energy is a cost, not a benefit.

It is time to unlock the supply shackles that our governments have created. Government policy prevents people from building more housing. Occupational licenses reduce supply. Labor legislation reduces supply and opportunity, for example, laws requiring that Uber drivers be categorized as employees rather than independent contractors. The infrastructure problem is not money, it is that law and regulation have made infrastructure absurdly expensive, if it can be built at all. Subways now cost more than a billion dollars per mile. Contracting rules, mandates to pay union wages, “buy American” provisions, and suits filed under environmental pretexts gum up the works and reduce supply. We bemoan a labor shortage, yet thousands of would-be immigrants are desperate to come to our shores to work, pay taxes, and get our economy going.

A supply crunch with inflation is a great wake-up call. Supply, and efficiency, must now top our economic-policy priorities.

*********

Update: I am vaguely aware of many regulations causing port bottlenecks, including union work rules, rules against trucks parking and idling, overtime rules, and so on. But it turns out a crucial bottleneck in the port of LA is... Zoning laws! By zoning law you're not allowed to stack empty containers more than two high, so there is nowhere to leave them but on the truck, which then can't take a full container. The tweet thread is really interesting for suggesting the ports are at a standstill, bottled up FUBARed and SNAFUed, not running full steam but just can't handle the goods.

Disclaimer: To my economist friends, yes, using the word "supply" here is not really accurate. "Aggregate supply" is different from the supply of an individual good. Supply of one good increases when its price rises relative to other prices. "Aggregate supply" is the supply of all goods when prices and wages rise together, a much trickier and different concept. What I mean, of course, is something like "the amount produced by the general equilibrium functioning of the economy, supply and demand, in the absence of whatever frictions we call low 'aggregate demand', but as reduced by taxes, regulations, and other market distortions." That being too much of a mouthful, and popular writing using the word "supply" and "supply-side" for this concept, I did not try to bend language towards something more accurate.

Monday, September 9, 2019

Intellectual property and the trade deficit

"The IP Commission estimates that between $200 billion and $500 billion a year of intellectual property is stolen from the U.S." I found this interesting tidbit in The Atlantic interview of Kevin Hassett, ex CEA chair. (HT Marginal Revolution)

Well, suppose China were to pay up, and pay the $200 to $500 billion a year in royalty payments. Where would it get the money from? Hmm. It would have to sell us an additional $200 to $500 billion worth of exports, that's how. The trade deficit would have to increase.

China could sell us $200 to $500 billion a year of assets instead. Maybe we would like to hold lots of Chinese stocks, bonds, or government bonds rather than buy more boatloads of goods? But if we bought worthwhile Chinese assets, those are only claims on future Chinese profits. And the only use we have for lots and lots of Chinese currency profits is to... buy things in China and send them here. If we bought worthless assets, bonds that default, or stocks whose legal rights evaporate, then, well, we're back where we started.

Or maybe we don't want to license IP, we just think US owned firms operating in China could make an additional $200 to $500 billion per year profits operating in China without Chinese competition. And what do US owners want to do with $200 to $500 billion of Chinese profits per year? Go on a shopping trip, and put it on boats, sooner or later.

One way or another, the only way that China can properly pay for intellectual property, is to put more stuff on boats and send it to us. Paying for intellectual property must increase the trade deficit.

Being a free trader, I think this is great. The point of trade is to get the imports. The point of intellectual property is to force China to send us boatloads of stuff.

Somehow I don't think the Administration sees it that way. But you can't escape addition.

Well, suppose China were to pay up, and pay the $200 to $500 billion a year in royalty payments. Where would it get the money from? Hmm. It would have to sell us an additional $200 to $500 billion worth of exports, that's how. The trade deficit would have to increase.

China could sell us $200 to $500 billion a year of assets instead. Maybe we would like to hold lots of Chinese stocks, bonds, or government bonds rather than buy more boatloads of goods? But if we bought worthwhile Chinese assets, those are only claims on future Chinese profits. And the only use we have for lots and lots of Chinese currency profits is to... buy things in China and send them here. If we bought worthless assets, bonds that default, or stocks whose legal rights evaporate, then, well, we're back where we started.

Or maybe we don't want to license IP, we just think US owned firms operating in China could make an additional $200 to $500 billion per year profits operating in China without Chinese competition. And what do US owners want to do with $200 to $500 billion of Chinese profits per year? Go on a shopping trip, and put it on boats, sooner or later.

One way or another, the only way that China can properly pay for intellectual property, is to put more stuff on boats and send it to us. Paying for intellectual property must increase the trade deficit.

Being a free trader, I think this is great. The point of trade is to get the imports. The point of intellectual property is to force China to send us boatloads of stuff.

Somehow I don't think the Administration sees it that way. But you can't escape addition.

Monday, August 12, 2019

Letter from Argentina

My friend Alejandro Rodriguez, at Universidad del CEMA, sends the following report:

Oops we did it again. Macri (the current president) lost in the open primary elections (all parties present their candidates in an open general election so it is like a very big poll). The formula Alberto Fernandez- Cristina Fernandez (the ex president who ruled between 2007 and 2015 is the candidate to vice president) is expected to win in October.

The peso is falling like a rock (down 25%) and interest rates are up by 1000 bps. The Central Bank has to 1.3 trillion ARS (22 billion USD at the current FX) in short term debt (all expires in the next 5 days). Today it has to roll 250 billion ARS and in the first round it only managed to roll 14 billion ARS. Argentine.

Argentina stocks in NY are down 50% to 60% and President Macri will adress the nation at 16:30 local time. The Central Bank has a lot of internatinal reserves (over 60 billion USD) but nearly 1/4 are the counterpart of dollar deposits at commercial banks. The remaining reserves are mostly borrowed from the IMF and China... We can surely screw over the IMF but I don't think that messing up with the Chinese is a smart move... so nobody knows how much fire power the Central Bank has to hold the FX. I don't know what can be done to stop a major currency crisis which might in turn into a debt crisis (if we are not in one already).

Wednesday, August 7, 2019

Trade and the Fed

Nina Karnaukh of Ohio State sent along this lovely graph of the 6 month Fed Funds futures around the beginning of August. Read this as the market's guess about what is happening to the Federal Funds rate over the next 6 months.

The first drop in price occurs with the FOMC announcement 2 PM July 31. The price drop is equivalent to a a rise in expected future interest rates of about 5 basis points or 0.05%. This has been read as market disappointment that the Fed did not signal more future rate cuts.

The subsequent price spike is this,

That statement caused a 10 bps rise in price, i.e. decline in expected interest rate. The natural interpretation: The markets expect the Fed to lower rates in a trade war, either directly or in response to the economic damage the trade war will cause.

I had read the Fed's recent actions as just a case of late expansion jitters, perhaps with a mild response to slightly lowered inflation. But this is clear evidence that the market sees the Fed reacting to trade news.

************

Should central banks offset trade wars? I think this is a question nobody is asking but it needs to be asked. Central banks including the US Fed and ECB seem to take for granted that any reduction in economic activity demands "stimulus" to offset it. But stimulus can only provide "aggregate demand." What if the problem is "aggregate supply" -- an economy humming along at full demand, and then someone throws a wrench in the works, be it a trade war, a bad tax code, or a regulatory onslaught? (I'll stop using quotes, to signal my dislike for these terms.)

Conventional wisdom ways that central banks should not offset reductions in aggregate supply. You can fight a lack of aggregate demand, but monetary policy cannot fight a decline in aggregate supply. The first job of a central bank should be to distinguish demand from supply shocks, so it can react to the former, but not to the latter. This standard wisdom emanates from the 1970s, where central banks kept rates low to offset the effects of oil price shocks -- supply shocks -- and ended up producing worse recessions and inflation.

Yet expressing this view at central banks these days, people stare at me with blank expressions. Distinguish... supply... from... demand... shocks....why would we do that? The view from about 1960s Keynesianism that all fluctuations in output, employment and prices come from demand, seems to have flowered again.

Now, in this conventional (i.e. 1980 Keynesianism vs 1965 Keynesianism) view the problem with offsetting a "supply" shock is that the monetary stimulus causes inflation. And now we have inflation once again drifting slightly lower. So perhaps the trade war is a "demand" shock? It's hard to see how though.

More plausibly, perhaps the policy uncertainty about the trade war is causing a decline in "demand." Why build a factory if any day now another tweet could render it unprofitable? The prospect of a trade war -- or the kind of serious political and trade turmoil that would follow Tianamen II in Hong Kong -- is a "confidence" shock. But the uncertainty is genuine. A rise in risk premium in an uncertain environment is genuine. People should hold off building factories that depend on a Chinese supply chain until we know if there is going to be a trade war. Unless the Fed is stepping more and more into the role of psychologist in chief, to decree that such fears are irrational, it's not obvious that the Fed should try to goose investment by artificially lowering the short term rate in response to a rise in trade fears.

A second possibility arises from more 1980s economics. A "supply" or productivity shock also lowers the expected return on investment. So the real interest rate should decline in response to such a shock. That is another reason perhaps for some interest rate decline in response to a negative supply shock. But how much? This still does not justify the same response to all sources of output decline, or (in our case) fear of output decline that has not happened yet.

The other possibility is that the Fed is now watching the exchange rate, as most other central banks do. The one thing that still does seem to work is that raising interest rates raises the value of the currency. The trade war raises the value of the dollar, and the US clearly wants to manipulate the dollar back down again.

Thursday, June 6, 2019

Institutionalized nonsense

When, last week, the Treasury issued its currency manipulation report, I thought it was a joke. Treasury put Germany and Italy on its "monitoring list" of countries suspected of "currency manipulation."

Germany and Italy are, of course, part of the Euro, the whole point of which is that they cannot, individually, "manipulate" their currencies, whatever that means. It is precisely this inability to devalue -- to "manipulate" the Drachma to regain "competitiveness" (another meaningless term) -- that conventional wisdom bemoaned of Greece.

I had a little chuckle, envisioning some frustrated mid-level Treasury economist bemoaning the trade and currency idiocy floating around Washington, putting this little message in a bottle to see if anyone noticed the reductio ad absurdum. If so, hello there, somebody noticed.

But then read the report.

Germany and Italy are, of course, part of the Euro, the whole point of which is that they cannot, individually, "manipulate" their currencies, whatever that means. It is precisely this inability to devalue -- to "manipulate" the Drachma to regain "competitiveness" (another meaningless term) -- that conventional wisdom bemoaned of Greece.

I had a little chuckle, envisioning some frustrated mid-level Treasury economist bemoaning the trade and currency idiocy floating around Washington, putting this little message in a bottle to see if anyone noticed the reductio ad absurdum. If so, hello there, somebody noticed.

But then read the report.

Wednesday, December 5, 2018

Taylor on China and Trade and Ideas

Tim Taylor, also reviewing Summers on China, makes a few excellent points.

Growth comes from within. Trade is not conquest.

Growth comes from within. Trade is not conquest.

The formula for economic growth is to invest in human capital, physical capital, and technology, in an economic environment that provides incentives for hard work, efficiency, and innovation. China has made dramatic changes in all of these areas, and they are the main drivers behind China's extraordinary economic growth in the last four decades, and its expectation of above-global-average growth heading into the future.

No matter your views of China's trade surplus, there's no sensible economic theory which suggests that China's trade surplus, which as a share of GDP is relatively small, is a major driver of China's growth....

Conversely, the US economy has not done a great job of investing in the fundamentals of economic growth.

Tuesday, December 4, 2018

Summers on China

(Continues from my last post on China trade)

Larry Summers has a good Financial Times oped on the same subject, titled "Washington may bluster but cannot stifle the Chinese economy." He puts well the point of my previous post:

At the heart of the US’s problem in defining an economic strategy towards China is the following awkward fact. Suppose China had been fully compliant with every trade and investment rule and had been as open to the world as the most open countries at its income level. China might have grown faster because it reformed more rapidly or it might have grown more slowly because of reduced subsidies or more foreign competition. But it is highly unlikely that its growth rate would have been altered by as much as 1 percentage point.

Equally, while some US companies might earn more profits operating in China [IP sharing requirements] and some job displacement in American manufacturing due to Chinese state subsidies may have occurred, it cannot be argued seriously that unfair Chinese trade practices have affected US growth by even 0.1 per cent a year.

Larry gives more voice to China critiques than I do, which is excellent. One should listen to what people are saying, understand their objectives, and if one disagrees on outcomes -- tariffs -- usually it is because one believes a common objective has a preferable means of achievement.

Yes, China misbehaves, to the annoyance mostly of producers in other countries and their mercantilist governments:

Flowers not tariffs

I wrote a little commentary on trade for The Hill, which they titled "The US should give China Flowers not Tariffs." Chocolates too.

|

| Source: The Hill |

(The facial expressions in the picture are priceless)

The US should Give China Flowers not Tariffs

Trump and Xi met, and declared a 90 day cease fire. Where will this end? It’s hard to forecast. Our commander in chief is less predictable than the stock market. But we can opine on what should happen. And we can look for interest — what is in everybody’s interest to have happen?

That answer is clear: Come to a quick deal, declare victory, and get back to work fixing real economic problems. China makes some commitments about intellectual property (reasonably good for both sides, though not as important as all the fuss makes it seem); China makes some promises to buy American goods (crony capitalist mercantilism, but it makes politicians feel good); the US announces the 25% tariffs are off the table. Both politicians announce a great triumph. In sum, roughly what happened with NAFTA. Better still, we could do some reciprocal opening: repeal the 25% tariff on pickup trucks, and our own restrictions on foreign investments.

Large additional tariffs would be terrible for the US economy. Tariffs are taxes. Traditionally anti-tax Republicans, fresh off a hard-won victory to lower corporate taxes, should get that. And these taxes are starting to bite. For just one example, GM’s decision to close car plants was not completely unaffected by the price of steel and aluminum needed to make cars. And the constant threat of tariffs is in some ways worse than tariffs themselves. Companies managing global supply chains need to know where and how to invest. Big uncertainty postpones those investments. The point of the corporate tax cut was to encourage companies to invest. The threat of tariffs undoes that incentive.

Big tariffs, with exemptions granted on a discretionary basis, are corrosive to our political system. The rest of the admirable deregulatory effort is trying to get government agencies out of this racket.

If it ever was true that China stole our jobs, that’s not today’s problem. With a 3.9% unemployment rate, employers can’t find enough qualified workers. Our economy needs efficiency and productivity to grow, not protection for some and high prices for others.

The US economy is doing well, but it’s an iffy time. When does the long expansion end and the next recession come? Storm clouds are gathering. The stock market is dribbling down. Auto sales, home prices and sales are softening. America remains waist-deep in debt. With split government, there will be no significant economic legislation legislation for the next two years, and the House will do everything they can to stymie the deregulation effort. A big disruption of trade and immigration is a self-inflicted wound at a bad time.

It’s an even iffier time for China. Be careful what you wish for. A major downturn in China, which could well lead to financial crisis, could be just the spark for a global recession.

What’s the long run goal? The right approach to trade is simple: zero tariffs or restrictions. Americans are free to buy from the cheapest and best supplier. Whether foreigners put in tariffs or not is irrelevant to that conclusion.

Trade is no different than new companies that can produce things cheaper or better. And just as hurtful to old companies and their workers, but we generally see that it’s unwise to stop innovation. Trade between countries is no different than trade between states, and we all recognize that tariffs between states are a terrible idea.

Any money that goes to China to buy goods must — must, this is arithmetic, not economics — come back. It just comes back to a less politically favored industry. To the extent that trade is “imbalanced,” that means China works hard, puts goods on boats, and takes our government bonds in return. Would we really be better off if we worked hard, put the fruits of our labor on boats, in exchange for Chinese government bonds? Paper and promises are cheap.

If China wants to tax her citizens to subsidize goods for US consumers, the right answer is flowers, chocolates and a nice thank-you card, as you would for any gift. Even intellectual property protection is an iffy cause. Theft is bad. But if selling the technology isn’t worth the market access, US companies don’t have to do it. Moreover, much intellectual property protection is the right to just the kind of continuing profits that we bemoan at home, in the new worry about increasing monopoly. Just how enthusiastic are we about defending pharmaceutical companies’ right to charge whatever they want in the US for their intellectual property?

If one wants to help the US economy, effort is far best spent at home — fix health care, financial regulation, the obscene tax code, zoning, occupational licensing, labor laws and on and on. The rewards are infinitely larger than any imaginable benefit from trade threats.

US GDP per capita is $60,000. China’s is $9,000. The average American is more than six times better off than the average Chinese. The air in Beijing is unbreathable. For the US to complain about China hurting us is like the captain of the football team complaining that a six grader cheated him out of lunch money.

Even in the best case, tariffs and trade restrictions are zero sum — they make the US better off by making China worse off. There is no case that they increase the size of the pie. In fact they make us all worse off. Is this America’s place in the world? Would we send in the marines to take wealth from Chinese people to benefit Americans? That’s the case for tariffs.

The idea that we can use tariffs to threaten China into freer trade is dangerous. It’s hard to credibly threaten to do something that hurts us, without denying that it does hurt us, and then getting trapped doing it. It took decades to get rid of the trade restrictions of the 1930s.

We should get a grip, set a standard for good self-interested free-trade behavior, and work with our allies to get China to obey the same rules. Such a China is far more likely to cooperate on security issues than one already at war with us over trade.

Update:

I left out lots of obvious pot shots. An obvious one: Sanctions on North Korea, Iran, Cuba, Russia, and so forth are designed to.. reduce imports. So we are doing to ourselves exactly what we are doing to them.

Update:

I left out lots of obvious pot shots. An obvious one: Sanctions on North Korea, Iran, Cuba, Russia, and so forth are designed to.. reduce imports. So we are doing to ourselves exactly what we are doing to them.

Monday, August 13, 2018

Trade uncertainty and investment

My colleague Steve Davis has a nice post quantifying economic uncertainty due to the trade war, and its emerging impact on investment.

Steve (and Nick Bloom) have done a great job quantifying policy uncertainty over time. To be clear, policies can have two effects -- there is the certainty of damaging policy, but there is also the damaging uncertainty of what policy will be. If a trade war seems to be looming, and you don't know if you will get tariff protection (raw steel) or be hurt by the tariff (steel users, competing with tariff-free steel products from abroad), that's uncertainty. Businesses hold off investing when they know things will be bad. But they also hold off when they're not sure what will happen. That's uncertainty.

Our little (so far) trade war is full of uncertainty

As of July, this uncertainty is only having a small effect on investment, and the economy is still booming -- in my view from the corporate tax rate cuts and deregulation efforts. It is true that the US is so big that most of the economy does not live on exports or directly compete with imports.

Steve (and Nick Bloom) have done a great job quantifying policy uncertainty over time. To be clear, policies can have two effects -- there is the certainty of damaging policy, but there is also the damaging uncertainty of what policy will be. If a trade war seems to be looming, and you don't know if you will get tariff protection (raw steel) or be hurt by the tariff (steel users, competing with tariff-free steel products from abroad), that's uncertainty. Businesses hold off investing when they know things will be bad. But they also hold off when they're not sure what will happen. That's uncertainty.

Our little (so far) trade war is full of uncertainty

Trade policy under the Trump administration also has a capricious, back-and-forth character... Less than three months after withdrawing from the TPP, the President said he would consider rejoining for a substantially better deal, only to throw cold water on the idea a few days later. Initially, the administration justified steel tariffs on the laughable grounds that Canada, for example, presents a national security threat. Later, President Trump tweeted that tariffs on Canadian steel were a response to its tariffs on dairy products. Some countries get tariff exemptions, some don’t. Exemptions vary in duration, and they come and go in a head-spinning manner. Two days ago (August 10), the President tweeted that he “just authorized a doubling of Tariffs on Steel and Aluminum with respect to Turkey” for reasons unclear. For a fuller account of tariff to-ing and fro-ing under the Trump administration, see the Peterson Institute’s “Trump Trade War Timeline.”The arbitrariness, including the waivers, means

Crony capitalism, political favoritism, and extra sand in the gears of commerce – here we come!But to the point, what's the Davis-Bloom quantitative measure of uncertainty doing? Answer: it is higher than even around the election -- whose outcome, and the nature of the Trump presidency certainly led to a vast amount of uncertainty.

As of July, this uncertainty is only having a small effect on investment, and the economy is still booming -- in my view from the corporate tax rate cuts and deregulation efforts. It is true that the US is so big that most of the economy does not live on exports or directly compete with imports.

Let’s sum up the U.S. survey evidence: About one-fifth of firms in the July 2018 SBU say they are reassessing capital expenditure plans in light of tariff worries. Among this one-fifth, firms have reassessed an average 60 percent of capital expenditures previously planned for 2018–19. ..Only 6 percent of the firms in our full sample report cutting or deferring previously planned capital expenditures in reaction to tariff worries. These findings suggest that tariff worries have had only a small negative effect on U.S. business investment to date.But it could get worse. Steve closes with a nice list of recent trade outbursts from our part of the economics blog world:

In closing, I should note that the harmful consequences of tariff hikes and trade policy uncertainty extend well beyond short-term investment effects. For other critiques of the Trumpian approach to trade policy, see the worthy commentaries by Robert Barro, Alan Blinder, John Cochrane, Doug Irwin, Mary Lovely and Yang Liang, Greg Mankiw and Adam Posen, among others.

Intellectual property and China

Let's transfer more technology to China, writes Scott Sumner, with approving comments from Don Boudreaux. They're exactly right, skewering one of the common backstop defenses of protectionists on both left and right.

The question is whether China can buy US technology, or require technology transfer to Chinese partners as a condition of the US firm entering China. Scott and Don have sophisticated versions of my reaction: If Chinese access isn't worth it to you, don't do the deal.

It stands to reason that stealing technology and IP is bad, and should be stopped. Whether imposing tariffs is the smart way to do that, we will discuss another day. But on an economic basis, even that is questionable!

A key point: Selling technology is not like selling a car. If you sell a car, you can't use it. If someone steals your car, you can't use it. But everyone can use knowledge. Scott:

The question is whether China can buy US technology, or require technology transfer to Chinese partners as a condition of the US firm entering China. Scott and Don have sophisticated versions of my reaction: If Chinese access isn't worth it to you, don't do the deal.

It stands to reason that stealing technology and IP is bad, and should be stopped. Whether imposing tariffs is the smart way to do that, we will discuss another day. But on an economic basis, even that is questionable!

A key point: Selling technology is not like selling a car. If you sell a car, you can't use it. If someone steals your car, you can't use it. But everyone can use knowledge. Scott:

The beauty of information is that use by one person does not preclude use by othersIf I know how to wax my car in half the time it takes you, and you sneak in to my house to learn my secret, you wax your car in half the time too. But so do I.

Saturday, August 11, 2018

Links: trade, housing, taxes

Three interesting links caught my attention today:

1) Prefab housing in Berkeley and Alex Tabarrok Commentary on Marginal Revolution.

Housing should be manufactured. As Tabarrok points out, it is one place where productivity has not improved much. I gather Ikea is now moving in to manufacture housing (I lost the link). Economies of scale should make a big difference. Once Ikea does to housing what they did to the Poang chair, steadily refining it, they can bringing the price down a lot.

But, manufactured houses have to obey local building codes too, and planning review and design review, and inspections, and all the other little local obstacles. Getting a uniform code will be a big fight, but strikes me as necessary to reap those economies of scale.

The prefab houses are made in China, using steel. A bunch of obvious meditations follow.

As I understand it, we now have import taxes (tariffs) on raw steel from China, but not taxes on products made out of steel. Why does the Trump administration so obviously provide an incentive for manufacturing to move to China? I've read a lot of stories about keg manufacturers, steel locker manufacturers, and so on going out of business over this difference. Is there some part of trade law that I don't know about that forces this outcome, and forbids them to also tax steel content of imports?

It nicely illustrates the point, that if you don't let people come to the US, the capital can go there. Even homebuilding.

2) Greg Mankiw makes an excellent point about marginal tax rates.

Phil Gramm and Robert B. Eklund wrote a great WSJ oped pointing out that inequality in the US really is not as large as it seems, because most measures left out government transfers, even cash transfers. (They cite the CATO study by John F. Early.) Once you add transfers back in again, the US has a much flatter income distribution. We have a more progressive tax system than Europe, with no VAT and lower payroll tax rates, and we do a lot of income transfers.

Greg points out a clever implication of this fact. From the pre- and post-tax and transfer income distribution, we can measure the average marginal tax rate, including the loss of benefits due to program phase out with income:

Greg says something about heterogeneity that I did not understand, but it strikes me that heterogeneity makes matters worse. Hetereogeneity means people are different. Some people are at a cliff: make one more dollar, lose medicaid or another service. Some people are not.

But if 76 percent on average means half the people face a 100% marginal tax rate and half face a 50% marginal tax rate, I think this means the overall disincentive effects are worse than if everyone faces 75% tax rate. In that circumstance half the people will not work at all. Sometimes in economics heterogeneity makes things worse, sometimes better. I think this is a case of worse, but I would be curious to know if there is a standard answer.

While we're on income transfers and disincentives, back to Berkeley

3) Back to trade, Tim Taylor the conversable economist has an excellent post on the Jones act. The Jones act is the law that requires all shipping between US ports to be on US made ships staffed by US merchant marines. (Tim builds on another Cato report by Colin Grabow, Inu Manak, and Daniel Ikenson.)

If you want evidence on whether protection makes an industry thrive, this is it

I hear even from formerly sensible correspondents now mad for tariffs that we need steel tariffs for national security, so we can fight WWII again, I guess. Well, the Jones act is a nice test case since much of its rationale is to keep a merchant marine going to staff all those liberty ships. Tim (and, really, Colin, Inu and Daniel) demolishes even the national security argument.

1) Prefab housing in Berkeley and Alex Tabarrok Commentary on Marginal Revolution.

Imagine a four-story apartment building going up in four days, and from steel. It happened in Berkeley, a city known for its glacial progress in building housing.Four days? Well, not really

The modules were stacked on a conventional foundation. Electricity, plumbing, the roof, landscaping and other infrastructure were added.That didn't take 4 days. And

The project, initially approved by the city in 2010 as a hotel, then re-approved in 2015 as studio apartments,So, really, 10+ years! (In my personal one data point, getting permits can take as long as building.)

Housing should be manufactured. As Tabarrok points out, it is one place where productivity has not improved much. I gather Ikea is now moving in to manufacture housing (I lost the link). Economies of scale should make a big difference. Once Ikea does to housing what they did to the Poang chair, steadily refining it, they can bringing the price down a lot.

But, manufactured houses have to obey local building codes too, and planning review and design review, and inspections, and all the other little local obstacles. Getting a uniform code will be a big fight, but strikes me as necessary to reap those economies of scale.

The prefab houses are made in China, using steel. A bunch of obvious meditations follow.

As I understand it, we now have import taxes (tariffs) on raw steel from China, but not taxes on products made out of steel. Why does the Trump administration so obviously provide an incentive for manufacturing to move to China? I've read a lot of stories about keg manufacturers, steel locker manufacturers, and so on going out of business over this difference. Is there some part of trade law that I don't know about that forces this outcome, and forbids them to also tax steel content of imports?

It nicely illustrates the point, that if you don't let people come to the US, the capital can go there. Even homebuilding.

2) Greg Mankiw makes an excellent point about marginal tax rates.

Phil Gramm and Robert B. Eklund wrote a great WSJ oped pointing out that inequality in the US really is not as large as it seems, because most measures left out government transfers, even cash transfers. (They cite the CATO study by John F. Early.) Once you add transfers back in again, the US has a much flatter income distribution. We have a more progressive tax system than Europe, with no VAT and lower payroll tax rates, and we do a lot of income transfers.

Greg points out a clever implication of this fact. From the pre- and post-tax and transfer income distribution, we can measure the average marginal tax rate, including the loss of benefits due to program phase out with income:

The bottom quintile earned 2.2% of all earned income in 2013, but after adjusting for taxes and transfer payments, its share of spendable income rose to 12.9%... The second quintile’s share more than doubled, rising from 7% of earned income to 13.9% of spendable income. For the third quintile, middle-income Americans, the increase was much smaller, from 12.6% to 15.4%.Thus

.. the effective marginal tax rate when a person moves from the bottom to the middle quintile is 1 - (15.4-12.9)/(12.6-2.2), or 76 percent.76 percent! The average person in the lowest quintile of the income distribution who earns an extra dollar, gets to keep only 24 cents. Can you spot the disincentive to work, or get an education?

Greg says something about heterogeneity that I did not understand, but it strikes me that heterogeneity makes matters worse. Hetereogeneity means people are different. Some people are at a cliff: make one more dollar, lose medicaid or another service. Some people are not.

But if 76 percent on average means half the people face a 100% marginal tax rate and half face a 50% marginal tax rate, I think this means the overall disincentive effects are worse than if everyone faces 75% tax rate. In that circumstance half the people will not work at all. Sometimes in economics heterogeneity makes things worse, sometimes better. I think this is a case of worse, but I would be curious to know if there is a standard answer.

While we're on income transfers and disincentives, back to Berkeley

In lieu of providing affordable units on site, Kennedy will pay a fee to the city of Berkeley’s Affordable Housing Trust Fund, as required under the city’s affordable housing laws. The amount is around $500,000, he said.Someone needs to write an expose of "affordable housing" programs. Who gets them and how? And once in, disincentives to earn more money, or take a better job in another city must be immense. It's also another hidden cross-subsidy driving up prices.

3) Back to trade, Tim Taylor the conversable economist has an excellent post on the Jones act. The Jones act is the law that requires all shipping between US ports to be on US made ships staffed by US merchant marines. (Tim builds on another Cato report by Colin Grabow, Inu Manak, and Daniel Ikenson.)

If you want evidence on whether protection makes an industry thrive, this is it

If susttained protection from foreign competition was a useful path to the highest levels of efficiency and cost-effectiveness, then US ship-building and shipping should be elite industries. But in fact, US ship-building and shipping--safely protected from competition-- have fallen far behind foreign competition, with negative costs and consequences that echo through the rest of the US economy--and probably diminish US national security, too.

...After nearly a century of protection from foreign competition, costs of ship-building in the US are far above the international competition.

"American-built coastal and feeder ships cost between $190 and $250 million, whereas the cost to build a similar vessel in a foreign shipyard is about $30 million.High shipping costs induce substitution

This shift away from water-based transportation to overland road and rail has a variety of costs, like greater congestion and wear-and-tear on the roads. It also has environmental costs like higher carbon emissions:

Unsurprisingly, the high cost of shipping by water means that in the US, freight is instead shipped overland. Consider, for example, all the trucks and trains that run up and down the east coast or the west coast.A long time ago when I was a CEA junior staffer, I got to see a bright idea die. The idea: Let's allow the US to export oil from Alaska to Japan. (There was an oil export ban, part of the legacy of 1970s energy policies.) Then use the money to buy oil from Saudi Arabia to send to the east coast. It's the same thing as sending Alaskan oil to the east coast but much cheaper. Everyone said great idea until the congressional liason said those ships from Alaska to the east coast are Jones act ships, and here is their list of threats if you do it. End of idea.

I hear even from formerly sensible correspondents now mad for tariffs that we need steel tariffs for national security, so we can fight WWII again, I guess. Well, the Jones act is a nice test case since much of its rationale is to keep a merchant marine going to staff all those liberty ships. Tim (and, really, Colin, Inu and Daniel) demolishes even the national security argument.

if that [national defense] is the goal, the Jones Act is sorely failing to accomplish it. Instead, the Navy can't afford the extra ships it wants, the number of available US civilian ships and the knowledgeable workers to run them is shrinking, and military operations have had to find ways to make use of foreign ships. Some anecdotes drive home the point:

"When U.S. forces were deployed to Saudi Arabia during Operations Desert Shield and Desert Storm, a much larger share of their equipment and supplies was carried by foreign-flagged vessels (26.6 percent) than U.S.-flagged commercial vessels (12.7 percent). Only one U.S.-flagged ship was Jones Act compliant. In fact, the shipping situation was so desperate that on two occasions the United States requested transport ships from the Soviet Union and was rejected both times. ... At the time, Vice Admiral Paul Butcher, who was then deputy commander of the U.S. Transportation Command, remarked that without the availability of foreign-flag sealift, `It would have taken us three more months to complete the sealift ourselves.' ...As with steel, if the goal is national defense, let the defense department ask for appropriations to staff a mothball merchant marine, don't force a hidden cross subsidy into the price of everything else.

Wednesday, August 8, 2018

Free Trade or Managed Mercantilism

Mary Anastasia O'Grady's WSJ coverage of Nafta talks included the following tidbit

Of course, they are far better than the alternative, in which everything is tariffed, protected, managed, and individually negotiated.

auto-sector “rules of origin,” which dictate how much of a vehicle must be made in North America to qualify as duty-free when it crosses continental borders.

In May, Team Trump proposed a new North American content requirement of 75%, up from the current 62.5%. It also wanted a new requirement that 70% of the steel and aluminum in Nafta vehicles be North American and new wage regulations that would require 40% of the value of North American cars and sport-utility vehicles—and 45% of Nafta trucks—be produced by workers making between $16 and $19 an hour.

Mexico countered with 70% North American content, a 30% regional steel requirement and 20% regional aluminum. Market-based labor rates are important for Mexican competitiveness, but Mexico showed flexibility by proposing $16 an hour for 20% of the value of vehicles it makes. The U.S. rejected that offer. Now the two sides are trying to find middle ground.Nafta and the like are often called "free trade agreements." Economists like me wonder, why does that take tens of thousands of pages? "We do not charge border taxes (tariffs), nor restrict quantities, nor will government purchases favor American companies." "We do the same." Done. That's free trade. This little snippet reminds us what trade pacts really are.

Of course, they are far better than the alternative, in which everything is tariffed, protected, managed, and individually negotiated.

Tuesday, July 31, 2018

Trade War 1914

The analogy between our looming trade war and August 1914, when events quickly spun out of control, led to this opinion essay at thehill.com. It brings together some themes from recent blog posts, so faithful readers may find some repetition. For reasons of space, a desire not to personalize things too much, and not to strain real history vs. the the superficial stories we retell, I didn't overdo the 1914 analogy. But it's easy enough to do if you want to. An impulsive leader, sensitive to personal sleights, started something that spiraled out of control. The idea that opponents will quickly surrender, rather than stiffen their resolve, has proved wrong over and over again in history.

104 years ago this August, the war to end wars broke out. It was a war that nobody wanted. The world stumbled in to it almost by accident, and then could not get out. “Wars are easy to win,” leaders thought. “We’ll be in Paris (or Berlin) by fall.” They were equally wrong, and equally befuddled once the trenches filled with bodies.

This August, the trade war to end tariffs looms, and the world seems to be stumbling towards an economic calamity that nobody wants, propelled by similar entanglements.

The trade war to end trade wars will end badly

104 years ago this August, the war to end wars broke out. It was a war that nobody wanted. The world stumbled in to it almost by accident, and then could not get out. “Wars are easy to win,” leaders thought. “We’ll be in Paris (or Berlin) by fall.” They were equally wrong, and equally befuddled once the trenches filled with bodies.

This August, the trade war to end tariffs looms, and the world seems to be stumbling towards an economic calamity that nobody wants, propelled by similar entanglements.

Friday, July 27, 2018

Trade war off?

Events move quickly in the Trump era. Since my last post, President Trump met with European Commission President Jean-Claude Juncker and announced a cease-fire with Europe. A correspondent sends this link to Marc Thiessen at Fox news on the subject

Could this trade war really be in the service of a completely free trade agenda -- either very well hidden, or newly discovered? There is nothing I would like to see more than a pure free trade world, and it is heartening to see this president or any president come close to endorsing such.

"Non-auto industrial goods" is already a big qualifier. US' 25% import tax on pickup trucks remains, and Europe's auto protection as well. Europe's big barriers against agricultural goods remain, along with the US' too. (Sugar quotas on and off since the 1790s, lots of Mexican produce barred even under Nafata.) Services, more important in the modern world than industrial goods, are off the table. So pure free trade this is not.

"it [europe] agreed to immediately buy more American soybeans -- which helps Trump in his trade battle with China." Free trade this is not. In a free trade world, European governments do not stop private European people and companies from buying US soybeans. In a free trade world, government ministers do not agree to buy more American soybeans! That's government run trade 101. Especially to gang up on a third party.

Valentina Pop and Vivian Salama at the Wall Street Journal add some reporting

"We can do stupid too" said Mr. Junckers, and he is right. This is stupid. We can shoot holes in the bottom of the boat to try to get you to stop shooting holes in the bottom of the boat. But if this is going to work, it had better work darn fast before the boat sinks.

Does President Trump really believe in a free trade world? Is this where it is all heading? In my last post I questioned the lack of a public goal to all this. Only two days ago -- yes, an eternity in Trump time, but fairly recent for the rest of us, the President tweeted

$817 seems to represent the overall trade "deficit" (I hate that word!) and Mr. Trump has consistently labeled trade deficits a "loss" for the US. (No, just as your trade deficit with the grocery store is not a loss -- you get the food!) If his hope is that the point and success of completely free trade is to eliminate trade "deficits," Mr. Trump will be sorely disappointed, as will any of his supporters who view this as a goal.

Completely free trade will open up many slowly dying industries to quick death from international competition. It will open up many new industries to tremendous growth. But is Mr. Trump really prepared to accept the former? In his tour through steel country, he did not say, "In six months I hope to see you all unemployed and this mill shut down again. But the opportunities for the country in software development, banking services, and intellectual property are so huge, I want you to support it."

The big question is, when does this stop? If it stops when we have global free trade, great. If we are going to keep plowing forward with tariffs, managed trade, countervailing subsidies, and so on until the trade "deficit" is eliminated, not so good.

OK, skepticism aside, yes he has twice said that the goal is totally free trade. I suggest the rest of the world call the bluff, if it is one, or give him what he wants, if not, immediately!

Tariffs, quotas, managed trade, arbitrary waivers, will damage the economy and our political system quickly. If this is going to work, it had better work fast.

it appears Trump is being proved right. On Wednesday, he and European Commission President Jean-Claude Juncker announced a cease-fire in their trade war and promised to seek the complete elimination of most trade barriers between the United States and the European Union. "We agreed today ... to work together toward zero tariffs, zero non-tariff barriers, and zero subsidies on non-auto industrial goods," declared the two leaders in a joint statement.

.... contrary to what his critics allege, Trump is not a protectionist; rather, he is using tariffs as a tool to advance a radical free-trade agenda.

... during the G-7 summit he made a sweeping proposal. "I said, 'I have an idea, everybody. I'll guarantee you we'll do it immediately. Nobody pay any more tax, everybody take down your barriers. No barriers, no tax. Everybody, are you all set?' ...

Now Trump's hard-line trade strategy is being vindicated. Not only is the E.U. negotiating zero tariffs, but also it agreed to immediately buy more American soybeans -- which helps Trump in his trade battle with China.

If Trump succeeds in using trade wars to bring down European and Chinese trade barriers, he may end up being one of the greatest free-trade presidents in history.The question always remains with our President's dramatic moves. Crazy like a fox or just plain crazy? To his credit, it helps if your opponents think the latter.

Could this trade war really be in the service of a completely free trade agenda -- either very well hidden, or newly discovered? There is nothing I would like to see more than a pure free trade world, and it is heartening to see this president or any president come close to endorsing such.

"Non-auto industrial goods" is already a big qualifier. US' 25% import tax on pickup trucks remains, and Europe's auto protection as well. Europe's big barriers against agricultural goods remain, along with the US' too. (Sugar quotas on and off since the 1790s, lots of Mexican produce barred even under Nafata.) Services, more important in the modern world than industrial goods, are off the table. So pure free trade this is not.

"it [europe] agreed to immediately buy more American soybeans -- which helps Trump in his trade battle with China." Free trade this is not. In a free trade world, European governments do not stop private European people and companies from buying US soybeans. In a free trade world, government ministers do not agree to buy more American soybeans! That's government run trade 101. Especially to gang up on a third party.

Valentina Pop and Vivian Salama at the Wall Street Journal add some reporting

Mr. Juncker stuck closely to the negotiating mandate handed to him by leaders of big EU countries including Germany, France and the Netherlands. Germany, which is heavily dependent on exports, was from the onset open to a trade arrangement, including abolishing EU tariffs on U.S. car imports. France, meanwhile, was vehemently opposed to opening EU agricultural markets.

Mr. Juncker told Mr. Trump and Mr. Lighthizer that any talk of including agriculture would kill prospects of a deal. He countered with a threat to drag public procurement into negotiations, which would question the Buy American Act, a nonstarter for the U.S. side.Well so much for unfettered free trade. Plus, as widely reported, this was a cease fire. There is no schedule for talks or any other implementation of the free trade niravna.

"We can do stupid too" said Mr. Junckers, and he is right. This is stupid. We can shoot holes in the bottom of the boat to try to get you to stop shooting holes in the bottom of the boat. But if this is going to work, it had better work darn fast before the boat sinks.

Does President Trump really believe in a free trade world? Is this where it is all heading? In my last post I questioned the lack of a public goal to all this. Only two days ago -- yes, an eternity in Trump time, but fairly recent for the rest of us, the President tweeted

$817 seems to represent the overall trade "deficit" (I hate that word!) and Mr. Trump has consistently labeled trade deficits a "loss" for the US. (No, just as your trade deficit with the grocery store is not a loss -- you get the food!) If his hope is that the point and success of completely free trade is to eliminate trade "deficits," Mr. Trump will be sorely disappointed, as will any of his supporters who view this as a goal.

Completely free trade will open up many slowly dying industries to quick death from international competition. It will open up many new industries to tremendous growth. But is Mr. Trump really prepared to accept the former? In his tour through steel country, he did not say, "In six months I hope to see you all unemployed and this mill shut down again. But the opportunities for the country in software development, banking services, and intellectual property are so huge, I want you to support it."

The big question is, when does this stop? If it stops when we have global free trade, great. If we are going to keep plowing forward with tariffs, managed trade, countervailing subsidies, and so on until the trade "deficit" is eliminated, not so good.

OK, skepticism aside, yes he has twice said that the goal is totally free trade. I suggest the rest of the world call the bluff, if it is one, or give him what he wants, if not, immediately!

Tariffs, quotas, managed trade, arbitrary waivers, will damage the economy and our political system quickly. If this is going to work, it had better work fast.

Wednesday, July 25, 2018

Trade War

I am encouraged by the reported Senate reaction (Politico) to the latest salvo in the trade war, the agriculture department's announcement to ramp up Roosevelt-era farm subsidies to offset the Administration's tariffs.

I'm even more delighted to see signs of Congress waking up

The answer is, because the Congress handed him that power. Congress likes to pass laws that make it look protectionist, and then count on the fact that no sane Administration would ever enforce them.

The regular trade law basically says that the Administration should impose tariffs if any industry is hurt. That's basically any industry that has any imports, i.e. all of them. We have counted for decades on no administration being nutty enough to actually do that.

The national security provisions under which the Trump administration is acting are even vaguer.

By now, both parties ought to be sick of the imperial presidency. Take back the power to impose tariffs. Or at least write a reasonable statute: that tariffs and quotas may only be imposed if consumers are harmed.

If national security is an issue, then write that the defense department must ask for it and pay for it. Do we need steel mills so we can re-fight WWII? If so, put subsidized steel mills on the defense budget. If defense prefers to use the money for a new aircraft carrier rather than a steel mill, well, that's their choice.

We are told that the trade war is all a game on the way to freer trade. I am dubious. From WSJ coverage,

I fear the goal is a bilateral trade surplus with every nation. That cannot happen without a massive change in our saving rate and federal deficit. In the meantime, if you impose a lot of tariffs on a country, its exchange rate depreciates so that the overall amount of trade is exactly the same. As is already happening with China, and now currency manipulation charges are back in vogue.*

Wars are hard to win, and they are only won if you have a clear objective, and know to stop when you reach the objective.

----------

* Update: A blog reader asked for an explanation.

You run a trade deficit with the grocery store. They sell you more food than you sell them. You run a surplus with your employer. You sell him or her more services than they sell you. Bilateral deficits are not a bad thing! If your garden is anything like mine, growing your own is a bad idea.

If you earn more from your employer than you spend at the store, then you are saving money. You run a net trade surplus with the world, and save it. You are accumulating financial assets. If you run a net trade deficit with the world, you are dissaving or borrowing.

So, we have the ironclad law. Savings - Investment = Net Exports. If you want to sell everything to the world, you have to save more than you are investing at home, and use the money you get from selling stuff to the world to buy foreign assets.

If your saving and investment do not change, your export position cannot change.

Now, what happens if the Administration puts a 100% tariff on everything imported, but we do not change savings and investment? Well, the total volume of imports - exports can't change. So the dollar has to go up relative to foreign currencies so that the after tax price of exports has not changed.

I hope that is not too simplified -- Im holding a lot of general equilibrium effects constant. Trade experts feel free to chime in in the comment if I am not clear or screwed that up somehow.

-------

Update 2: The Washington Examiner does a much better and more detailed job on economic policy by fiat and waiver, though still missing, I think, the greatest danger:

------------

“Taxpayers are going to be asked to initial checks to farmers in lieu of having a trade policy that actually opens and expands more markets. There isn’t anything about this that anybody should like,” said Sen. John Thune of South Dakota, the No. 3 GOP leader....

You put people in the poorhouse and provide them aid. What you need to do is not put them in the poorhouse,” Corker saidThese views are good, but not really in my mind the largest danger. The closest is Sen. Ron Johnson:

“This is becoming more and more like a Soviet type of economy here: Commissars deciding who’s going to be granted waivers, commissars in the administration figuring out how they’re going to sprinkle around benefits,” said Sen. Ron Johnson (R-Wis.). ...”

It's not really Soviet, which was more do what you're told or go to Siberia. It's a darker system, which leads to crony capitalism.

Everyone depends on the whim of the Administration. Who gets tariff protection? On whim. But then you can apply for a waiver. Who gets those, on what basis? Now you can get subsidies. Who gets the subsidies? There is no law, no rule, no basis for any of this. If you think you deserve a waiver, on what basis do you sue to get one?

Well, it sure can't hurt not to be an outspoken critic of the administration when the tariffs, waivers, and subsidies are being handed out on whim.

This is a bipartisan danger. I was critical of the ACA (Obamacare) since so many businesses were asking for and getting waivers. I was critical of the Dodd Frank act since so much regulation and enforcement is discretionary. Keep your mouth shut and support the administration is good advice in both cases. And to my mind, our drift to an economy in which every successful business needs a special waiver or dispensation from the government, granted at the government's pleasure or displeasure, is our greatest danger.

I'm even more delighted to see signs of Congress waking up

... a number of senators have been itching to tie the president’s hands from making unilateral tariff policy with legislation that would require Congress to approve of unilateral tariffs that are imposed with the justification of national security.Yes, but that's only the beginning. Tariffs are a tax. Why does the President have unilateral power to impose a tax? The president can't change the income tax code (except for some interpretation issues. Index capital gains for inflation now!)

The answer is, because the Congress handed him that power. Congress likes to pass laws that make it look protectionist, and then count on the fact that no sane Administration would ever enforce them.

The regular trade law basically says that the Administration should impose tariffs if any industry is hurt. That's basically any industry that has any imports, i.e. all of them. We have counted for decades on no administration being nutty enough to actually do that.

The national security provisions under which the Trump administration is acting are even vaguer.

By now, both parties ought to be sick of the imperial presidency. Take back the power to impose tariffs. Or at least write a reasonable statute: that tariffs and quotas may only be imposed if consumers are harmed.

If national security is an issue, then write that the defense department must ask for it and pay for it. Do we need steel mills so we can re-fight WWII? If so, put subsidized steel mills on the defense budget. If defense prefers to use the money for a new aircraft carrier rather than a steel mill, well, that's their choice.

We are told that the trade war is all a game on the way to freer trade. I am dubious. From WSJ coverage,

What’s the strategy, what’s the end game here? At what point do we start seeing things move out of the chaotic state they are in now and to where we actually see new trade agreements?” asked Sen. Mike Rounds (R., S.D.).

Mr. Trump, addressing a gathering of veterans groups on Tuesday, urged patience on trade, despite concerns raised by critics: “Just stick with us,” he said. “It’s all working out.”Well, what is the end game? If it is a world of zero tariffs -- a suggestion the G7 should have taken and run with -- fine, but say so. If it is for China to reform intellectual property treatment, fine, say so. You cannot expect a negotiating adversary to move unless that adversary understands that if you do X, the problem really will be solved. If the goal posts always shift, they have no reason to budge.

I fear the goal is a bilateral trade surplus with every nation. That cannot happen without a massive change in our saving rate and federal deficit. In the meantime, if you impose a lot of tariffs on a country, its exchange rate depreciates so that the overall amount of trade is exactly the same. As is already happening with China, and now currency manipulation charges are back in vogue.*

Wars are hard to win, and they are only won if you have a clear objective, and know to stop when you reach the objective.

----------

* Update: A blog reader asked for an explanation.

You run a trade deficit with the grocery store. They sell you more food than you sell them. You run a surplus with your employer. You sell him or her more services than they sell you. Bilateral deficits are not a bad thing! If your garden is anything like mine, growing your own is a bad idea.