Debt Matters

(This is a draft of an oped. I got done and saw it's 1500 words, so I'm posting it for your enjoyment rather than go through a painful 600 word diet. Diet later. Maybe. )

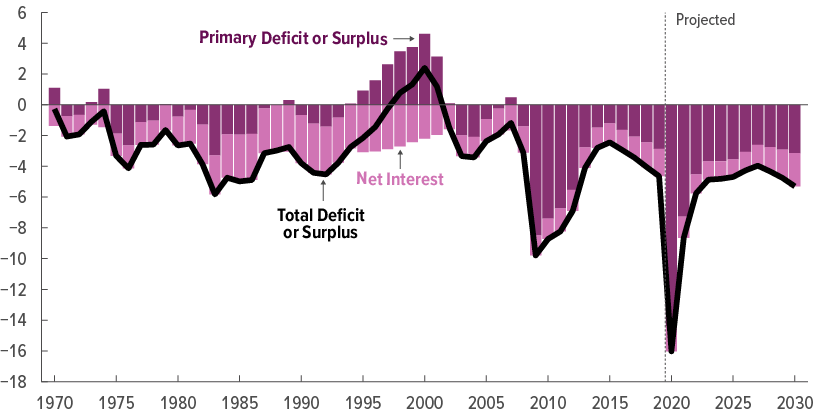

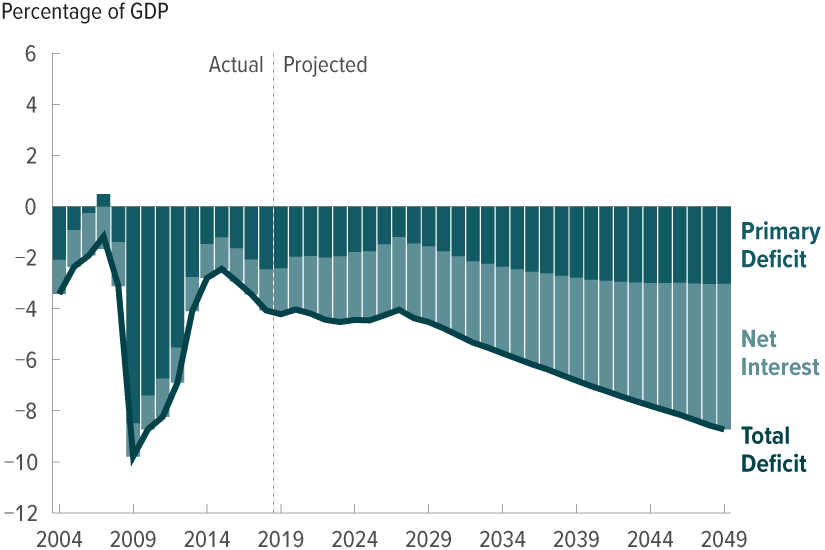

Last week, the U.S. passed a milestone — US federal debt in private hands exceeded 100% of GDP. But does all this debt matter, or is worrying about debt passé?

This debate has been going on among economists for a while. One does not need to go to the incoherence of "modern monetary theory" to find support for the view that debt has few consequences. Olivier Blanchard, of MIT and the IMF, in his Presidential Address to the American Economic Association, (excellent summary here) declared that “there may be no fiscal costs” of additional debt. The core of his argument is that the interest rate on government debt may be lower than the growth rate of the economy so the US can roll over debt forever.

Larry Summers, ex treasury secretary, President of Harvard, and adviser to presidents, surely the preeminent policy economist of our generation, has advocated that additional debt-financed spending may have so strong a multiplier as to pay for itself. (Paper here) As a result “expansionary fiscal policies may well reduce long-run debt-financing burdens," a super-Keynesian version of the Laffer curve

(I don’t mean to pick on Blanchard and Summers — they are only superbly distinguished representatives of widely held views.)

Unlike MMT, these are logically consistent possibilities. But are they right?

The interest rate on government debt is indeed slightly lower than good guesses of the economy’s growth rate, as sadly low as the latter is, so that if we roll over debt with no additional deficits, the debt to GDP ratio will slowly decline and the US can indeed run this slow-rolling Ponzi scheme.

But how long will this happy circumstance of ultra-low interest rates continue? More to the point, how scaleable is this opportunity? Bond market investors lend 100% of GDP to the US government at 1% interest. Will they lend 200% of GDP at the same low interest rate, or will they start to require higher interest rates? A government that finances itself only with money and no debt need not pay back the money -- but, obviously, cannot double the opportunity.

What happens when, rather than grow out of a given debt, the US piles on larger and larger debt to GDP ratios each year? The analysis is about sustainability of a large, but steady debt to GDP ratio. It does not justify a debt to GDP ratio that grows 10 percentage points per year. At what debt to GDP ratio must the party stop and the growing out of it begin?

Blanchard recognizes these limits are out there somewhere, and that debt crowds out private investment. But just where the limits are is less clear. That finding the limits will be unpleasant is clear.

Summers’ view is likewise limited to a period of “secular stagnation” with perennially deficient demand, sticky prices and wages, and the other requirements of extreme Keynesianism. Are we in such a period, or is covid a supply shock? Was the economy really suffering lack of demand when unemployment hit 50 year lows last February?

Washington knows no such sophistication, but our politicians have grasped the logical implications of the proposition that debt does not matter with more clarity than have economists.

The notion that debt matters, that spending must be financed sooner or later by taxes on someone, and that those taxes will be economically destructive, has vanished from Washington discourse on both sides of the aisle. The covid response resembles a sequence of million-dollar bets by non-socially distanced drunks at a secretly reopened bar: I’ll spend a trillion dollars! No, I’ll spend two trillion dollars! That anyone has to pay for this is un-mentioned. Well, perhaps nobody does have to pay.

And who is to blame them, really? Markets offer 1% long-term interest rates. Blowout spending financed by the Fed printing money — which is no different from debt — has resulted in no inflation so far. Faced with the deep concerns of current voters, worry that our children and grandchildren might have to pay off debt is not particularly salient. They’re either in the basement playing video games or out protesting for the end of capitalism anyway. Politicians will take the cheap money as long as markets are happy to provide it.

The economists, even the modern monetary theorists, envision debt issued to finance worthy investments, or valuable spending, all undertaken with a careful green eyeshade approach. Washington has figured out the logical conclusion of the idea that Federal debt doesn’t matter, in a way these economists have not: If debt and money printing have no fiscal cost, why be careful about how you spend money? Send checks to voters. Why not? It’s costless. No boondoggle project is objectionable. Send billions to prop up dying businesses. Why not? It’s costless. Why bother fixing the post office? Send them another $25 billion. Or $100.

Deeper: Why should citizens have to pay back debts if the Federal government does not have to do so? Bail out student loans. Bail out bankrupt states and locals and their pensions. Cancel the rent. Cancel the mortgage. Why should anyone have to pay any debt if the Federal government has access to a money machine? Why work? Why should the federal government not just keep printing money and sending it to us? Other countries are not so lucky as we are. Why should emerging markets pay back debt if the US does not have to? Bail them out.

Why indeed should anyone pay taxes? Here Stephanie Kelton, MMT proponent, has followed the logic. The only reason to charge taxes at all, in her view, is to expropriate the wealthy to rob them of political power.

These are inescapable logical conclusions of the view that federal debt has no fiscal cost. If you’re uncomfortable with the end of the trip, perhaps you should revisit the assumption from which it inexorably follows. At least, you recognize that the opportunity to borrow with little fiscal cost is limited, so should be preserved.

Advocates point to WWII. It is true, that the US exited an even greater debt to GDP ratio. It was not painless. Growth higher than interest rates was part of it, but not all. Two bouts of inflation, in the late 1940s and in the 1970s devalued much debt. The US ran steady primary (excluding interest costs) surpluses from the 1940s through the mid 1970s. Spending was low in the pre-entitlement economy, and nobody was totting up hundreds of trillions in unfunded promises. The war, and its spending, was over. Statutory personal taxes and actual corporate taxes were high. Financial repression and closed international capital markets kept interest rates on government bonds low, and deprived Americans of better investment opportunities and our and the world’s economies much needed investment capital. And we had an international debt crisis in the early 1970s, prompting the abandonment of Bretton woods and depreciation of the dollar.

In short, the US grew out of WWII debt by not borrowing any more, by decades of fiscal probity, and by strong supply-side growth in a deregulated economy. We have none of these reassurances going forward. And this, and the UK exit from Napoleonic War debt in the 1800s by starting the industrial revolution are about the only historical examples of a semi-successful repayment of this much debt. Otherwise, the history of large sovereign debts is one long sorry tale of default, inflation, devaluation, and consequent financial chaos. The UK did not exit WWII debt successfully, leading to crisis after crisis, and everyone else did worse.

Still, what should we be afraid of? The vision of grandchildren saddled with taxes, or even just unable to borrow more while the economy sits at its limit, of, say, 200% debt to GDP, is indeed not a salient brake to spending.

That is not the danger. The danger the US faces, the danger we should repeat and keep in mind, is a debt crisis. We print our own money, so the result may be a sharp inflation that wipes away the value of debt rather than an even more disruptive default, but the consequences will be almost as dire.

Imagine that 5 or even 10 years from now we have another crisis, which we surely will. It might be another, worse, pandemic; a war involving china, Russia or the Middle East. Imagine the US follows its present trends of partisan government dysfunction, so an impeachment is going on, a contested election, and even militias roaming the streets of still boarded up cities. Add a huge economic recession, but unreformed spending promises.

At this point, the US has, say, 150% debt to GDP. It needs to borrow another $5 - $10 trillion, or get people to hold that much more newly-printed money, to bail out once again, and pay everyone’s bills for a while. It will need another $10 trillion or so to roll over maturity debt. At some point bond investors see the end coming, as they did for Greece, and refuse. Not only must the US then inflate or default, but the firehouse of debt relief, bailout and stimulus that everyone expects is absent, together with our capacity for military or public health spending to meet the shock that sparks the crisis.

Yes, I've warned about this before, and no, it hasn't happened yet. Well, if you live in California you live on an earthquake fault. That the big one hasn't happened yet doesn't mean it never will.

No, interest rates do not signal such problems. (Alan Blinder, covering such matters in the Wall Street Journal, "if the U.S. Treasury starts to supply more bonds than the world's investors demand, the markets will warn us with higher interest rates and a sagging dollar. No such yellow lights are flashing.) They never do. Greek interest rates were low right up until they weren’t. Interest rates did not signal the inflation of the 1970s, or the disinflation of the 1980s. Lehman borrowed at low rates until it didn’t. Nobody expects a debt crisis, or it would have already happened.

We cannot tell when the conflagration will come. But we can remove the kindling and gasoline lying around. Reform long-term spending promises in line with long run revenues. Reform the tax code to raise money with less damage to the economy. And today, spend only as if someone has to pay it back. Because someone will have to pay it back.

Blanchard concludes with “public debt.. can be used but it should be used right.” I agree. We are in a crisis, and thoughtful spending with borrowed or printed money is necessary. (How about a test a week for every American?) But keep constantly in mind, it will be paid back, steadily or chaotically. There really is no argument. Most of these points are in Blachard's Presidential Address.

Whether a steady debt/GDP ratio can life with small steady primary deficits, rather than small steady primary surpluses is not the interesting question. There is a limit, a debt/GDP beyond which markets will not lend. On this, I think, we all agree. There is a finite fiscal capacity. Even though in theory the r<g argument would allow a 1,000% debt to GDP ratio, or 10,000%, at some point the party stops. The closer we are to that limit, the closer we are to a real crisis when we need that fiscal capacity and it is no longer there.

***********

And now, dear fellow Americans, enjoy your Labor Day. Please listen to Dr. Fauci and don't run out to party like you did on Memorial Day. Let's be sensible and get this thing over with.

Update: A new and better post More on Debt follows.