Following my last post on debt I've thought a bit more, and received some very useful emails from colleagues.

A central clarifying thought emerges.

The main worry I have about US debt is the possibility of a debt crisis. I outlined that in my last post, and (thanks again to correspondents) I'll try to draw out the scenario later. The event combines difficulty in rolling over debt, the lack of fiscal space to borrow massively in the next crisis. The bedrock and firehouse of the financial system evaporates when it's needed most.

To the issue of a debt crisis, the whole debate about r<g, dynamic inefficiency, sustainability, transversality conditions and so forth is largely irrelevant.

We agree that there is some upper limit on the debt to GDP ratio, and that a rollover crisis becomes more likely the larger the debt to GDP ratio. Given that fact, over the next 20-30 years and more, the size of debt to GDP and the likelihood of a debt crisis is going to be far more influenced by fiscal policy than by r-g dynamics.

In equations with D = debt, Y = GDP, r = rate of return on government debt, s = primary surplus, we have* \[\frac{d}{dt}\frac{D}{Y} = (r-g)\frac{D}{Y} - \frac{s}{Y}.\] In words, growth in the debt to GDP ratio equals the difference between rate of return and GDP growth rate, less the ratio of primary surplus (or deficit) to GDP.

Now suppose, the standard number, r>g, say r-g = 1% or so. That means to keep long run average 100% debt/GDP ratio, the government must run a long run average primary surplus of 1% of GDP, or $200 billion dollars. The controversial promise r<g, say r-g = -1%, offers a delicious possibility: the government can keep the debt/GPD ratio at 100% forever, while still running a $200 billion a year primary deficit!

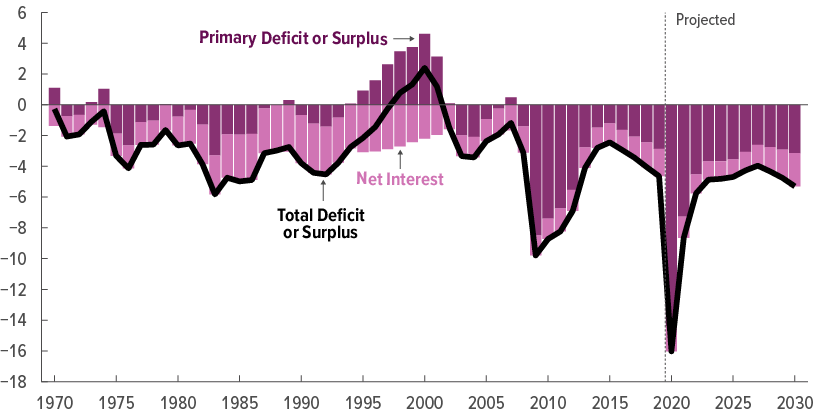

But this is couch change! Here are current deficits from the CBO September 2 budget update

Now that this is clear, I realize I did not emphasize enough that Olivier Blanchard's AEA Presidential Address acknowledges well the possibility of a debt crisis:

Fourth, I discuss a number of arguments against high public debt, and in particular the existence of multiple equilibria where investors believe debt to be risky and, by requiring a risk premium, increase the fiscal burden and make debt effectively more risky. This is a very relevant argument, but it does not have straightforward implications for the appropriate level of debt.

See more on p. 1226. Blanchard's concise summary

there can be multiple equilibria: a good equilibrium where investors believe that debt is safe and the interest rate is low and a bad equilibrium where investors believe that debt is risky and the spread they require on debt increases interest payments to the point that debt becomes effectively risky, leading the worries of investors to become self-fulfilling.

Let me put this observation in simpler terms. Let's grow the debt / GDP ratio to 200%, $40 trillion relative to today's GDP. If interest rates are 1%, then debt service is $400 billion. But if investors get worried about the US commitment to repaying its debt without inflation, they might charge 5% interest as a risk premium. That's $2 trillion in debt service, 2/3 of all federal revenue. Borrowing even more to pay the interest on the outstanding debt may not work. So, 1% interest is sustainable, but fear of a crisis produces 5% interest that produces the crisis.

Brian Riedi at the Manhattan Institute has an excellent exposition of debt fears. On this point,

... there are reasons rates could rise. ...

market psychology is always a factor. A sudden, Greece-like debt spike—resulting from the normal budget baseline growth combined with a deep recession—could cause investors to see U.S. debt as a less stable asset, leading to a sell-off and an interest-rate spike. Additionally, rising interest rates would cause the national debt to further increase (due to higher interest costs), which could, in turn, push rates even higher.

***********

So how far can we go? When does the crisis come? There is no firm debt/GDP limit.

Countries can borrow a huge amount when they have a decent plan for paying it back. Countries have had debt crises at quite low debt/GDP ratios when they did not have a decent plan for paying it back. Debt crises come when bond holders want to get out before the other bond holders get out. If they see default, haircuts, default via taxation, or inflation on the horizon, they get out. r<g contributes a bit, but the size of perpetual surplus/deficit is, for the US, the larger issue. Again, r<g of 1% will not help if s/Y is 6%. Sound long-term financial strategy matters.

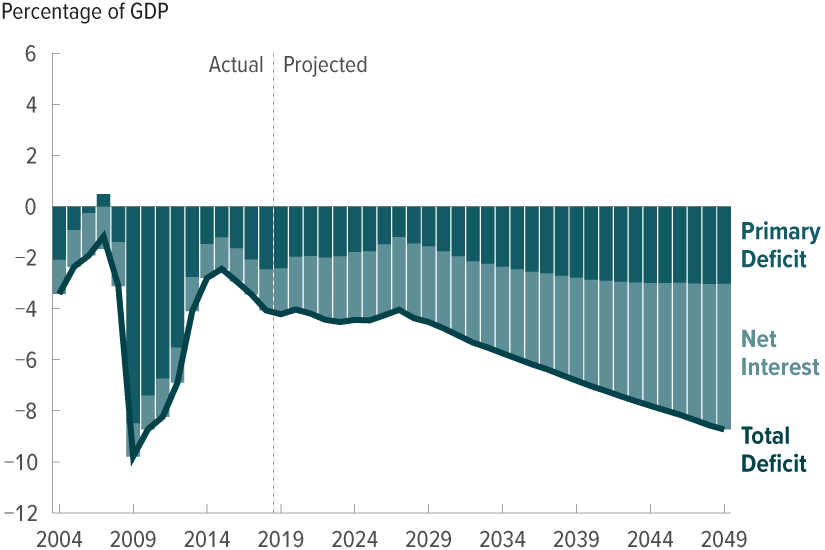

From the CBO's 2019 long term budget outlook (latest available) the outlook is not good. And that's before we add the new habit of massive spending.

******

Policy.

As Blanchard points out, small changes do not make much of a difference.

a limited decrease in debt—say, from 100 to 90 percent of GDP, a decrease that requires a strong and sustained fiscal consolidation—does not eliminate the bad equilibrium. ...

Now I disagree a bit. Borrowing 10% of GDP wasn't that hard! And the key to this comment is that a temporary consolidation does not help much. Lowering the permanent structural deficit 2% of GDP would make a big difference! But the general point is right. The debt/GDP ratio is only a poor indicator of the fiscal danger. 5% interest rate times 90% debt/GDP ratio is not much less debt service than 5% interest rate times 100% debt/GDP ratio. Confidence in the country's fiscal institutions going forward much more important.

At this point the discussion usually devolves to "Reform entitlements" "No, you heartless stooge, raise taxes on the rich." I emphasize tax reform, more revenue at lower marginal rates. But let's move on to unusual policy answers.

Borrow long. Debt crises typically involve trouble rolling over short-term debt. When, in addition to crisis borrowing, the government has to find $10 trillion new dollars just to pay off $10 trillion of maturing debt, the crisis comes to its head faster.

As blog readers know, I've been pushing the idea for a long time that especially at today's absurdly low rates, the US government should lock in long-term financing. Then if rates go up either for economic reasons or a "risk premium" in a crisis, government finances are much less affected. I'm delighted to see that Blanchard agrees:

to the extent that the US government can finance itself through inflation-indexed bonds, it can actually lock in a real rate of 1.1 percent over the next 30 years, a rate below even pessimistic forecasts of growth over the same period

contingent increases in primary surpluses when interest rates increase.

I'm not quite sure how that works. Interest rates would increase in a crisis precisely because the government is out of its ability or willingness to tax people to pay off bondholders. Does this mean an explicit contingent spending rule? Social security benefits are cut if interest rates exceed 5%? That's an interesting concept.

Or it could mean interest rate derivatives. The government can say to Wall Street (and via Wall Street to wealthy investors) "if interest rates exceed 5%, you send us a trillion dollars." That's a whole lot more pleasant than an ex-post wealth tax or default, though it accomplishes the same thing. Alas, Wall Street and wealthy bondholders have lately been bailed out by the Fed at the slightest sign of trouble so it's hard to say if such options would be paid.

Growth. Really, the best option in my view is to work on the g part of r-g. Policies that raise economic growth over the next decades raise the Y in D/Y, lowering the debt to GDP ratio; they raise tax revenue at the same tax rates; and they lower expenditures. It's a trifecta. In my view, long-term growth comes from the supply side, deregulation, tax reform, etc. Why don't we do it? Because it's painful and upsets entrenched interests. For today's tour of logical possibilities if you think demand side stimulus raises long term growth, or if you think that infrastructure can be constructed without wasting it all on boondoggles, logically, those help to raise g as well.

********

*Start with \(\frac{dD}{dt} = rD - s.\) Then \( \frac{d}{dt}\frac{D}{Y} = \frac{1}{Y}\frac{dD}{dt}-\frac{D}{Y^2}\frac{dY}{dt}.\)

***

Update: David Andolfatto writes, among other things,

"Should we be worried about hyperinflation? Evidently not, as John does not mention it"

For these purposes, hyperinflation is equivalent to default. In fact, a large inflation is my main worry, as I think the US will likely choose default via inflation to explicit default. This series of posts is all about inflation. Sorry if that was not clear.

also

Is there a danger of "bond vigilantes" sending the yields on USTs skyward? Not if the Fed stands ready to keep yields low.

All the Fed can do is offer overnight interest-paying government debt in exchange for longer-term government debt. If treasury markets don't want to roll over 1 year bonds at less, than, say, 10%, why would they want to hold Fed reserves at less than 10%? If the Fed buys all the treasurys in exchange for reserves that do not pay interest, that is exactly how we get inflation. And mind the size. The US rolls over close to $10 trillion of debt a year. Is the Fed going to buy $10 trillion of debt? Who is going to hold $10 trillion of reserves, who did not want to hold $10 trillion of debt.

In a crisis, even the Fed loses control of interest rates.

One interesting thought that this provoked: The more one is confident that Piketty-type theories are what generate increasing inequality, the more one should be concerned about deficit spending. The correlation instead seems to be the reverse.

ReplyDeleteRegardless of debt level, bond investors can never really drive up interest rates by themselves as long as the Fed is willing to do QE. They need an alternative to invest or stash their savings in and that alternative has to drive up consumer prices for the interest rate to shoot up.

ReplyDeleteA generalized panic and inflation can happen if everyone (not just bond investors) starts abandoning the dollar, and the USD currency notes become hot potato so everyone wants to exchange it as soon as they get hold of it. As you've said, there's no predictable debt-to-gdp that triggers this, but a collapse in the faith of US institutions at any debt level can cause this.

That's the drama, I think: the bond interest rates, due to the FED intervention, do not include any more, any useful "information" on the sustainability of the US government debt.

DeleteContrary to what John says in this post, I think that the FED intervention also means that the government can issue all the debt it wants (not only the prices but also the volumes are now "information less" to evaluate sustainability)

Once the interest rate (and the ability to issue additional debt) has been stripped down of its "information providing features" by the FED intervention, they could not be the mechanisms that introduce rationality again.

The question are:

(1) does the fed intervention solve the "fever" (the price of the bonds or the volumes that the government can issue) or the "illness" (the increased allocation of resources to economically useless government driven activities and the negative impact in economic growth and well-being)?

(2) Are there "other information mechanisms" that the FED can not control (at least at the same time it controls goverment debt prices and volumes)? (ie inflation)

(sensible people can disagree on which the "illness" actually is)

The missing link in this discussion is the Federal Reserve's balance sheet (or the Bank of Japan's).

ReplyDeleteIf the Fed accumulates, say, 50% of outstanding federal debt, then about the half the burden of making interest payments is met by incoming interest on bonds owned by the Fed.

This is not so outlandish--it has already happened in Japan. The Fed's balance sheet seems to ratchet up in every recession too (in relation to GDP).

Japan's outlook right now is for mild deflation, and property has been deflating there for decades.

Little discussed is the Swiss National Bank, which to fight an appreciating currency, printed up Swiss francs and accumulated a balance sheet of non-Swiss sovereign bonds, equal to about $100,000 per Swiss resident, or about equal to Swiss GDP. The Swiss franc stopped appreciating for a while, but they are having problems again. The Swiss central banking system is even more convoluted than that of the US, but I guess they are collecting interest on the sovereign bonds holdings.

Which raises a delicious possibility: What if the Fed began accumulating foreign sovereign bonds, say $500 billion a year, by printing dollars and buying sovereigns.

Some dollar depreciation? A huge bulwark stored up to service debts? Inquiring minds want to know.

Doesn't the Swiss National Bank also charge negative rates on the base money it created to purchase the sovereign bonds it holds? So it gets paid back twice for expanding base money. That tells me a lot about the demand for a secure ("hard") monetary asset among humans.

DeleteIt makes me wonder why 100 years ago this government abandoned the more primitive method of letting some holders play with bullion? (Greedy sovereigns did not not to pay out any; it was considered a loss of face or something. Nixon was worried about the Soviets having a larger gold penis than the USA.)

Why not simply have Congress authorize an optional Kilogram gold bond, for perhaps 100 years at 1% (consoles would be better)? Investors could swap UST for 'USG' at current daily exchange rates for USD. It would be a toy for investors - and foreign governments - but it could replace some of the burden of Treasuries on a saturated market and potentially raise funds for pensions like mine.

You are presuming that sovereign debt holders are willing to sell $500 billion a year - they can always say no thanks (Nein, Danke).

DeleteIt is even worse. If you read John's comment (or Blanchard AEA Presidential Address) keeping in mind that "investors" does not mean anything anymore, then the whole argument about sustainability or about the mechanisms of the debt crisis do not make any sense and are not, in any way, related with the “real” world we are living in.

DeleteThe FED is "the investors". A deep pocket one. But with totally different incentives. I do not even know what their incentives are, academic praise? a political career? ... I feel extremely uncomfortable with the fact that huge amounts of money are allocated following a "political” (or even worse, “academic”) criteria.

The FED can buy any amount of debt the government is willing to issue as far as the banks trust the FED enough to hold the government debt for hours in their balance sheets ... and there is always a commission that could get them doing so (and if not the limit of the FED no buying debt in the primary market can be removed).

And the FED (or the BoJ) intervention is not limited to government debt, corporate debt too.

More money allocated following political criteria, the "creative destruction" stopped by the FED because the public is not willing to accept bankruptcies as a healthy mechanism for growth anymore, no mechanism in place ("investors" is just a "figure of speech" with no economical meaning) to force back a rational allocation of capital ... The end game is not pretty, and it is a "boiling frog" kind of situation. The symptoms: slow growth, capital misallocation, government economic dependence ... they are all here already, with no self-balancing mechanism in place they can only get worse.

Unfortunately, there is no possible "debt crisis" in sight ... that is the real drama.

Or is there? can the FED really buy any amount of debt the government will issue? The real “institutional crisis” is POTUS and the FED president getting into a confrontation with the latter refusing to back-up the former expending program … that is, indeed, a really interesting war-game!

"Or is there? can the FED really buy any amount of debt the government will issue?"

DeleteThe answer to that is - IF the FOMC bought up all the federal debt, why would taxpayers and voters continue to make payments on that debt or authorize the sale of that debt?

Remember there are three parties to this game (bond buyers including the FOMC, taxpayers, and voters). If two of the three walk away the jig is up.

Very interesting. "Taxpayers" don´t pay taxes anymore to payback the debt not even to cover the government expenses. As a matter of fact, tax rates have gone down while expenses and debt have gone up.

DeleteThe "taxpayer idea" is now all about social justice and equality. Tax rates are stablished and modified as a "political game" with the main objective of getting votes thru a "narrative".

Once you have the "buffer" of the FOMC buying the debt, there is not any link any more between the budget needs and the tax income. That is a fact. John has said many times that the logical conclusion of the MMT is that taxes can be eliminated. The proponents of the MMT don´t say that because taxes serve a partisan purpose.

And I don´t see the voters stopping this "FED buying the debt" game … everybody likes free money. The same way that voters in Venezuela didn´t reject the oil financed social programs from the early Hugo Chavez. "Voters" are all about narratives. Bryan Caplan did a great job explaining this in "The Myth of the Rational Voter".

There is no mechanism that can stop the growing of the FED balance. It is very convenient, short-term for the politicians, the taxpayers, the voters ... But long term is devastating. The signs are everywhere, the Gosplan is back in fashion in France, the French government stopping the LVHM-Tiffany deal, the European Green New Deal being implemented with the investments aproved and controlled by the burocrats ... we know how a government controlled economy ends, we are going to visit that place again ... it is the "democratic" (by the time being) version of the "great leap forward".

El emperador,

Delete"Once you have the buffer of the FOMC buying the debt, there is not any link any more between the budget needs and the tax income."

That is incorrect. Just because the FOMC buys debt, that does not eliminate the taxpayer liability. You are presuming that once the FOMC buys the debt, it is extinguished. Not true. The central bank can turn around and sell that debt any time it chooses.

"John has said many times that the logical conclusion of the MMT is that taxes can be eliminated."

And John/MMT is wrong because they fail to understand that the primary purpose of taxation is to create a demand for a commonly used currency. It is a network effect. Governments tax so that people will use their currency (instead of

sea shells, small bits of metal, or other means) in the purchasing and selling of goods.

"And I don´t see the voters stopping this FED buying the debt game … everybody likes free money."

If everyone (including the voters) loved free money, there would not be a FED or government debt at all. And I never insisted that voters will end the game of government debt. I only stated that they (the voters and taxpayers) can end the game of government debt regardless of what the FOMC or the bond market as a whole wants to do.

"There is no mechanism that can stop the growing of the FED balance."

The FED operates under legal constraints set by Congress and ultimately the voters and taxpayers. And the FED is one of numerous central banks. So yes, there are several mechanisms that could end the FED - they could be removed/constrained by legal / political means or monetary policy for the U. S. could be offshored.

"It is very convenient, short-term for the politicians, the taxpayers, the voters..."

You must be talking to different taxpayers and voters.

El emperador,

Delete"Once you have the buffer of the FOMC buying the debt, there is not any link any more between the budget needs and the tax income. That is a fact."

Incorrect. Even when the FOMC buys the federal debt, it is still a liability to the taxpayer. John also discusses banks being paid interest on reserves held at the Fed. That interest on reserves is the very same interest income (courtesy of the taxpayer) that the Fed receives on the government bonds that it holds.

"John has said many times that the logical conclusion of the MMT is that taxes can be eliminated."

And John and his logical conclusion are wrong. Taxes create an incentive for people to use government sponsored money in day to day transactions. That is what is meant by taxes create a demand for the government's money. People will use dollars because they don't want to carry around two (or more) types of money - one for paying taxes and the other for purchasing goods. It is a network effect.

"And I don´t see the voters stopping this FED buying the debt game … everybody likes free money....There is no mechanism that can stop the growing of the FED balance. It is very convenient, short-term for the politicians, the taxpayers, the voters."

You must be talking to the wrong voters.

Frestly,

DeleteAfter Arrow's theorem, we know any taxpayer or voters aggregated preferences are either dictatorial or incoherent, so claiming to know this impossible aggregated preference is "populist" to say the least, I give you that. But, still, a significant number of individual "voters" are more than happy with the government checks coming their way and/or with the reductions in taxes they have seen in their paychecks. They do not care a bit whether this has been financed thru fresh debt or not. Actually, they don’t even have a political option that advocates debt reduction in the coming elections.

Let me reword my point in a way I think it’s easier to agree (even if we don’t in the theories leading to this conclusions).

• the FED buying the government debt reduces the risk of a debt crisis (it was actually design just for that!)

• The possibility of this risk reduction being transformed in an effort to “eliminate” this risk is very real. I do see the FED trying this. It does not make any sense reducing the risk of a debt crisis when the debt is, let’s say 80% of GDP, and letting this very same crisis unfold when it is 120%. And I really don’t see taxpayers and voters "forcing" this unfolding at the 120% level (why did not they at the 80% level?).

• I hope you are right, and the FED cannot eliminate debt crisis forever. I just really do not see why or when or how. In any case “delaying’ the crisis means making it much worse. Totally avoiding the crisis (if possible) will, likely, result in a disaster in terms of capital allocation and growth. It could be that we are already in “autopilot” down this road. Taxpayers and voters, much less politician, stopping the car seems wishful thinking.

On your comments:

If I own money to the bank, I have a liability, if I own money to my wife you can argue I also have a liability but using the same term for both is misleading (divorce between the government and the FED will be a very interesting situation).

Saying that the purpose of taxes is to create demand for money is a very stylized elegant type of theory. In the real world nobody works to pay taxes. I do not see people being less willing to get government's money in a world free of taxes, quite the contrary.

The real political debate around taxes is the conflict of two narratives: a) Let's redistribute by taxing the "rich" and giving to the "poor" vs b) Let's provide the right incentive for people to create new companies and work harder making them to pay less taxes. I haven't heard any politician saying: Let's increase taxes to pay back the debt we already have or (even less) let's increase taxes to give a boost to the demand for government's money (you can be sure this last one will look like a lunatic to voters).

Same way that whatever Ricardo and Barro say, people do not save today to pay taxes tomorrow. They don't adjust their expenses looking at tha last report of the CBO. Actually, the vast majority of them are totally unaware of the amount they own thru the government. You do not save to payback I liability you are unaware of.

El emperador,

Delete"After Arrow's theorem, we know any taxpayer or voters aggregated preferences are either dictatorial or incoherent, so claiming to know this impossible aggregated preference is populist to say the least, I give you that."

I don't claim to know the aggregated preference of taxpayers and voters. I do know that the phrase "the validity of the public debt shall not be questioned" in the 13th amendment to the Constitution was placed there precisely because the voters and taxpayers in the southern states were prepared to walk away from debts incurred by the Union during the Civil War.

And so to say that "aggravated preferences of voters" are dictatorial or incoherent misses the obvious historical example.

If you want to understand how a debt crisis might happen - find out where the cracks in the system are.

"The FED buying the government debt reduces the risk of a debt crisis (it was actually design just for that!)"

Incorrect. The federal reserve banks and board of governors were created in 1913 under the Federal Reserve Act. The federal open market committee (FOMC) was not created until 20 years in the Banking Act of 1933.

The reason for creation of the FOMC is unclear, however even to this day, the FOMC is precluded from purchasing government debt when it is auctioned by the Treasury Department.

So how does the FOMC stop a government debt crisis if they can't buy that debt at auction when the auction does not draw enough buyers?

"Saying that the purpose of taxes is to create demand for money is a very stylized elegant type of theory. In the real world nobody works to pay taxes. I do not see people being less willing to get government's money in a world free of taxes, quite the contrary."

You are confusing the actions and intent of government (those who levy taxes) and the actions and intent of people living under that government (those who pay taxes). I never said that people work to pay taxes. I said people accept government money for the work that they perform because their taxes must be paid in government money. Absent taxes, people would likely choose any medium of exchange that is convenient. That could still be government money or be it could be something else.

And where is this world free of taxes that you are witness to?

"I haven't heard any politician saying: Let's increase taxes to pay back the debt we already have or (even less) let's increase taxes to give a boost to the demand for government's money (you can be sure this last one will look like a lunatic to voters)."

No instead you have heard politicians like George Bush Sr. say "NO NEW TAXES" and turn around and raise taxes precisely because of the government debt that was being built up. I never said that politicians are the most honest of people.

The problem with r>g, is that r-g is a function of how selective you are in your investments.

ReplyDeleteIf you only invest in S&P companies, you're investing in the most profitable and successful companies in the economy, ignoring the myriad failed companies, startups, and lemonade stands around the world.

Any VC or HF can tell you that beating the market by being selective in your investments is easy: just take on additional risk. In that case, r>g.

But, as your capital grows, you have trouble being selective. r approaches g. At the point where you are managing all the money in the world, r=g. There's just no way you could own the entire world and outperform yourself. It's impossible.

Similarly, a government's return on investment will approach g based on the amount of debt or investments relative to the size of the economy. As the return on investments approaches g, and the interest on its debt is greater than g (because selective investors only buy government debt when r>g) the government inevitably defaults.

This selectivity function is common knowledge among any serious seeker of alpha. I see it in my own work. You see it in any fund that's growing.

Incorporate that into the equation and we have: r-g = s, that is: the difference in your return relative to the economy is your "selectivity." This is a much more sensibly equation and explains exactly how the economy self-corrects for wealth concentration.

Your original post and subsequent elaboration are a real public service. I hope they are widely read.

ReplyDeleteYour concerns are shared by me and most of my (former) IMF colleagues who worked on the US. The r-g argument has been misleading to those who don't follow the data closely insofar as, even with r<g, the primary deficit required to stabilize or reduce the debt ratio is far from that at present or realistically in prospect. Moreover, if you look at the most recent IMF report on the US you will find that the focus is on general government (rather than only federal government), that the baseline foresees a continuing rise in the debt ratio, and that with a bit of fiddling it is not unlikely that we'll see a general government debt ratio above 150% (and rising) in the next 5-10 years.

Logically there are three options for containing, and eventually reducing, the debt ratio (an objective on which I concur with you for all the reasons you adduce):

(i) Higher real growth. I doubt that the rate of growth of US potential GDP can be raised much above 1.5 - 2% without some dramatic supply side changes to boost TFP plus substantial immigration. Moreover, the government seems incapable of effective and efficient investment in infrastructure--both physical and social--which could boost TFP.

(ii) Inflation, which will increase nominal growth relative to effective nominal interest rates on medium- and long-term government debt. The new Fed framework could help. I suspect most economists would be prepared to swallow the insidious distribution effects of inflation at, say, 5% for a while. But there are dangers: sustained low real interest rates will exacerbate asset price bubbles, corporate leverage, and misallocated investment, keep zombie companies alive, circumscribe monetary policy options in the next crisis, and lead to the same financial fragility we saw at the beginning of the current crisis. (At an IMF seminar I led a few years ago for central bankers and prudential authorities, it was startling to see the disconnect: central bankers wanted to focus narrowly on goods-and-services inflation and leave leverage and asset price issues to the prudential authorities; the latter tried valiantly to explain that very easy monetary conditions created incentives for leverage and financial innovation around regulations that no periodic adjustment of regulations could contain.)

(iii) A major tax overhaul on the argument that it may be easier to do something large than small. Imagine a less opaque tax system with a broader base, lower marginal rates, fewer loopholes, and, ideally, a VAT and substantial taxes on petroleum and other pollutants.

Ideally we would aim at a combination of these solutions. But sadly only the second and least desirable seems congruent with the politics of the time, and even that may be difficult to engineer.

Thanks for your posts.

Leslie Lipschitz

Thanks for this very helpful comment. I did not know that such good sense is common inside the IMF!

DeleteMr. Lipschitz,

DeleteThere is a fourth option not on your list that should be considered - Government Equity.

Inflation (your option ii) is a risk born by all money / bond holders, whether they chose to carry that risk or not.

What if instead, individuals were able to purchase risk assets (equity) from the government of their own volition and without that risk spreading to other portions of the economy (material, labor, and other markets)?

Mr. Lipschitz,

DeleteI hope you understand that a program like Social Security has an equity like aspect in that benefits are not transferred between generations. Meaning as soon as someone dies, the benefits they receive die with them. The risk to a Social Security recipient is that he/she will not live long enough to receive benefits comparable to the contributions.

In that sense, from a government finance perspective, Social Security is superior to marketable government bonds. Bonds can be transferred (as an asset) from generation to generation. The only way they can be eliminated is through direct government action (raising taxes, cutting spending, or converting them to equity).

Mr. Lipschitz,

DeleteI hope you also understand that a program like Social Security is superior to marketable government bonds in that enrollment into the Social Security program is offered on demand rather than as a consequence of government deficits.

It doesn't matter what the government's fiscal position is (deficit or surplus), when someone starts working for a living they can start contributing to the social security system.

If I wanted to buy the longest dated federal government security (currently 30 years), the federal government must run a deficit for me to do so. Otherwise, on the secondary market, I am relegated to buying 17 year or 23 year or some other prior 30 year bond issue that has aged.

Social Security is fundamentally a progressive idea (equality of opportunity, not equality of outcome). Some individuals may not live long enough to collect any benefits, some may live long enough to collect what they contribute and more.

This comment has been removed by the author.

ReplyDelete"China is pushing to make the Yuan into a reserve currency to rival the U.S. dollar."

DeleteNot sure whether it will rival the US dollar but it already is a reserve currency. It's one of the currencies in the IMF's SDR basket after all.

"growth in the debt to GDP ratio equals the difference between rate of return and GDP growth rate, less the ratio of primary surplus (or deficit) to GDP".

ReplyDeleteThis does not take into account possible changes in the "tax income to GDP" ratio for a given tax code due to the increase in debt.

If one of the purpose of the additional debt, like, for example, in the case of the Green New Deal, is to "reduce inequality" (let's translate that, for the sake of clarity, as "to reduce taxable income inequality") then, given the progressivity of the actual tax code, the increase in debt to finance a "successful” Green New Deal, will mean the total tax income will not increase at the GDP growth rate. Differences of more than 1% in the tax income to GDP ratio are not difficult to imagine if the GND significantly reduce "taxable income inequality" as its propaganda says it will do.

John,

ReplyDelete"So how far can we go? When does the crisis come? There is no firm debt/GDP limit."

That is correct.

But recognize first that interest paying government debt is an entitlement program. Neither the legislature nor the executive branch of government is legally obligated to borrow. In fact, government debt is the first entitlement program before Social Security, Medicare, Medicaid, and all the rest came into existence. And so if "reforming entitlements" is part of the magic elixir to returning to stable government finances, then the easiest place to start is with the debt itself.

Recognize also that when a government borrows at any interest rate it puts itself at potential loggerheads with monetary policy stance.

Finally recognize that there are three parties to the debt that the U. S. has issued - tax payers (that make the debt payments), voters (that legitimize the issuance and payments on the debt), and bond buyers (interest and principal payment recipients). There is some overlap between these groups and there are individuals that may belong only to one or none of these groups.

In any three party relationship, it takes a majority vote of two parties to hold the relationship together. If voters and taxpayers walk away from the relationship, then bondholders are left with nothing. If voters and bond buyers walk away, then taxpayers can continue making the payments on existing debt (of their own volition) but won't be able to roll over existing debt or issue new debt. If bond buyers and tax payers walk away, then voters won't be able to approve the issuance of new debt.

A debt crisis happens when two of the parties walk away from the relationship.

And so your solutions to the debt "problem" are all wrong. They don't address the entitlement aspect of interest paying debt, they don't address the potential for fiscal / monetary conflict, and they don't address the possibility of the tri-party relationship breaking down.

Solution #1: Borrow long. Debt crises typically involve trouble rolling over short-term debt. When, in addition to crisis borrowing, the government has to find $10 trillion new dollars just to pay off $10 trillion of maturing debt, the crisis comes to its head faster. As blog readers know, I've been pushing the idea for a long time that especially at today's absurdly low rates, the US government should lock in long-term financing.

Questions / Concerns

1. Are today's absurdly low interest rates an effect of the US government keeping a short duration on it's debt and or an effect of monetary policy stance? And so, as soon as the government borrows more long term, does that wipe out any perceived benefit?

2. Borrowing long term does nothing if coupon interest payments are made on all government debt. Borrowing long term with zero coupon debt delays the interest payments until the debt reaches maturity.

Solution #2: Contingent plans? Blanchard's concise summary adds another interesting option. Contingent increases in primary surpluses when interest rates increase.

And what - wait for when the party in office, running for re-election, tells Treasury to shorten maturity who then tells the Fed to accommodate?

The Answer is government equity. Specifically the answer is government equity in the form of fixed term, zero coupon, non-transferrable securities that can only be redeemed against a future tax liability. Realized returns on this equity rise and fall with economic growth, they are non-persistent government liabilities (when the owner dies, the government's liability dies with them), and they don't make cash payments - meaning the Executive branch of government / Treasury department would not require Congressional approval to begin selling them.

A few more comments on government debt.

DeleteQuestion: Why does government debt exist in the first place?

Answer: It exists to allow banks to manage their credit risk. In that sense it acts as an entitlement program (or insurance program if you prefer).

Question: If banks need government debt to manage credit risk, then don't budget surpluses impede that ability?

Answer: Absolutely. That was the mistake of the Clinton / Rubin / Greenspan era. They were celebrated for the era of prosperity they helped create, but their (Rubin / Greenspan's) plan for mitigating credit risk (especially in the banking sector) was - "Trust us, we know what we are doing". Which turned into, we can't bail everyone out, so we will let some fail (Lehman Bros, Merrill Lynch) and some remain (JP Morgan, Goldman Sachs).

Question: Given the need for government debt as a credit management tool for banks, can and should governments sell new debt (in addition to what is rolled over) regardless of fiscal position (surplus / deficit).

Answer: Governments should be able to sell securities on demand (rather than as a consequence of deficits) but they can't because of the central bank (lender of last resort) and the nature of government debt itself.

A government that sold debt on demand would soon find banks borrowing from the central bank at a short term rate and demanding enough bonds such that all available tax revenue would be spent making the interest payments.

Can a government sell equity on demand? Absolutely. Because the risk inherent to the government equity buyer lies entirely with that buyer (see risk profile described above), the government can sell as much equity as being demanded at any time regardless of fiscal position.

A private bank even with access to the Fed would be foolish to buy more government equity than what the projected tax liability is for that bank.

Question: And so how does government equity succeed where Rubin / Greenspan failed?

Answer: Government equity could be used as collateral in a lending arrangement between a borrower and a private bank.

In this way, rather than a private bank buying government debt to manage credit risk (bank buys the insurance), the private borrower pledges the government equity he has purchased as collateral on a loan from a bank (borrower buys the insurance).

Government equity (unlike other forms of collateral) can be as divisible as money and bonds. Meaning that partial defaults (a borrower misses some payments) are simply handled by the bank retaining a portion of the collateral until the borrower catches up with the payments.

Should a complete default occur (based upon some reasonable time frame), then and only then, the collateral provided by the private borrower could be converted to U. S. government bonds.

Of course there are some finer details to work out that would prevent banks from making sham loans for the sole purpose of obtaining government bonds.

One thing to consider is that if the rate of return on the government equity is always greater than the interest rate on the loan, the private borrower would have a pretty serious incentive to keep current on his / her loan payments.

More on the "three party" relationship.

DeleteSome economists (Paul Krugman for instance) view government programs as essentially Ponzi schemes. In a Ponzi scheme existing investors (beneficiaries) are paid from money obtained from new investors. But what Paul fails to understand is that in a true Ponzi scheme, there are no voters, whereas with government programs like interest paying bonds and Social Security, there are voters.

In a Ponzi scheme with two groups (investors and beneficiaries), if either group decides to call things off, then the Ponzi scheme collapses. Normally, the scheme collapses in this situation when there are not enough new investors to make the payments to beneficiaries.

Any two party financial arrangement is unstable in this fashion because when only one party withdraws, the arrangement falls apart.

Three party arrangements tend to be much more stable because it takes two parties walking away for the arrangement to collapse.

Ever wonder why the pyramids are made in a triangular shape, why structural steel beams are comprised of triangles, why we have three branches of government, why the "stable" family unit consists of man / women / and child, or why triangular diplomacy was a success for Henry Kissinger?

If more equity is the right solution for banking finance in addressing debt overhang - see here:

ReplyDeletehttps://johnhcochrane.blogspot.com/2016/05/equity-financed-banking.html

Then it stands to reason that equity is the right solution for government finance in addressing debt overhang.

John, let me do a thought experiment using Solow and DDM. Crowding out investment in enterprises. Output of capital, labor and technology = 1.2 trillion. GDP = 20T. r-g =.06 (.08 -.02). Now; 20 = 1.2/(.08-.02). If g is reduced to .015 because of investment declining GDP is 18.46 = 1.2/(.08-.015). On an absolute basis, GDP declined 1.54 trillion with a .005 point decline in growth. dGDP/dg = .308. My assumptions are greatly simplified so as to help me think through this.

ReplyDeleteI don't find the idea that the US government will be unable to roll its debt convincing. If the Fed's repo rate peg is credible, then there's arbitrage between cash and short-term debt if the rates on debt rise. There should never be a scenario where the government can't get people to exchange cash for bills. Greece is not the United States. The Euro is not a liability of the Greek government. The United States having a debt crisis is like saying that a company is having a "stock crisis".

ReplyDeleteThere are really two questions to ask. The first is "What is the expected path of primary deficits that the market is pricing?"

Right now the market is perfectly content charging the government -0.4% to borrow in real terms for 30 years when everyone seems to expect primary deficits to remain permanent.

The second is "Where does the market think r-g will go?".

We don't know the answer to either of those questions.

Anonymous,

Delete"I don't find the idea that the US government will be unable to roll its debt convincing. If the Fed's repo rate peg is credible, then there's arbitrage between cash and short-term debt if the rates on debt rise. There should never be a scenario where the government can't get people to exchange cash for bills."

That is because you are only thinking about things from a bond buyers perspective. There are two other parties to consider - tax payers and voters.

Suppose that some combination of the FOMC and the rest of the world owned all of the U. S. federal debt (or some large portion of it). At what point do both U. S. taxpayers and voters simply say - "We are done. Payments on the US debt and the sale of that debt are suspended indefinitely."? Through a Constitutional Amendment, this is entirely possible.

Notice in that situation, it would not matter what either the Fed or the bond market does.

"The United States having a debt crisis is like saying that a company is having a stock crisis".

That is your opinion because you believe that government bonds do carry / should carry the same level of risk as corporate equities (stocks)?

You do realize that corporations (most large ones anyway) are financed through a mix of bonds (less risky) and stocks (more risky)?

You do realize that corporations once they sell equity shares are under no legal obligation to buy back those shares? This is quite unlike the debt that the federal government sells that must legally pay interest on and buy back at maturity.

And so your comparison between government bonds and corporate equities seems misplaced but raises a couple of fundamental questions.

Should governments (like companies) also rely on a mix of less risky debt and more risky equity, and what should the risk profile of that equity look like? My own opinions on that are in another post on this page.

There is a coherent postulation of a mechanism for price inflation and Government debt. When the holders of money issued by the Fed or bonds issued by the treasury spend the money or spend the bonds directly or by hypothecaton, that constitutes a coherent postulation of a mechanism.

ReplyDeleteI had a simple policy idea for controlling the debt:

ReplyDelete1) Set a maximum debt-to-GDP ratio. When GDP is measured, this sets a budget cap.

2) If the government wants to breach this cap, all spending beyond the cap must be financed by a poll tax (i.e. everyone pays the same dollar amount).

We accept the argument that there are times when extra spending is called for. But doing this would be done with prudence, as a poll tax is going to be quite unpopular. A trillion dollar "deficit" would mean a poll tax of about $4000 per adult.

People with limited resources could request an exemption. But the tax would be counted as a debt they must repay, should their economic situation improve.

Think im starting to get an allergic reaction every time i hear or see the word debt.

ReplyDeletehttps://aab-edu.net/

My head is pounding with all the charts and formulas. How about an outside the box solution like My Fair Share USA Pledge. MFS will reduce the existing debt, provide a fund to pay off maturing Ts when they are redeemed and eliminate the $7 trillion projected interest for the next ten years. Please contact me.

ReplyDeleteHow can a country, such as the U.S., which denominates its bond issues in U.S. dollars possibly default on its debt obligations? It won't. Why? Because it controls the U.S. dollar issuance. Your treasury bond of $1,000 face value is worth exactly 1,000 U.S. dollars at maturity. You receive exactly what you contracted to receive at maturity, not a penny less. No default, no dishonour.

ReplyDeleteSecond issue: during 2020 (year to date) treasury real return bonds (5-30 years constant maturity) are priced to yield negative rates of interest, not 1%/year as the blog article appears to imply. Would that they did yield a 1% per annum real rate of return to maturity--we'd all be in there like 'Flint' in a Texas heart beat, but that anomolous pricing situation wouldn't last half the span of time of a Texas heart beat, a.s.

Third issue: The charts shown in the blog article send a silver spike through the heart of the premise that today's bond valuation is equal to the net present value of stream of future primary surpluses. By the reasoning of the FTPL, today's bonds are likely of negative value, even when measured on a nominal dollar basis. Could FTPL be wrong?

Old Eagle Eye,

Delete"How can a country, such as the U.S., which denominates its bond issues in U.S. dollars possibly default on its debt obligations?"

By choice, the same way that you or I could refuse to pay a mortgage or a credit card bill. Except in the case of a country like the U. S., there is no bankruptcy court to worry about.

Old Eagle Eye,

Delete"How can a country, such as the U.S., which denominates its bond issues in U.S. dollars possibly default on its debt obligations?"

It can by political / economic choice. Consider if all of the federal debt was owned by some combination of the FOMC / foreign investors. What would stop U. S. taxpayers and voters from simply deciding to stop making payments on that debt? The incentive for the U. S. to continue making payments on that debt comes from the overlap between bond holders who are also taxpayers and voters. Eliminate that overlap, and there is nothing to stop taxpayers and voters from walking away.

"It won't. Why? Because it controls the U.S. dollar issuance."

Yes it controls that U. S. dollar issuance. No those newly issued dollars do not have to be spent making debt payments.

"Your treasury bond of $1,000 face value is worth exactly 1,000 U.S. dollars at maturity. You receive exactly what you contracted to receive at maturity, not a penny less."

My treasury bond of $1000 is worth that because I (as both a U. S. taxpayer and voter) support the 13th amendment to the Constitution. If there are not enough U. S. taxpayers and voters owning treasury bonds, would political support of payments on those bonds fall apart?

>Again, r<g of 1% will not help if s/Y is 6%.

ReplyDeleteThe official projections of long-run s/Y under current law are around 2.5%. At a 250% debt-to-GDP ratio, aka Japan's, that exactly balances an r-g of -1%. Financial repression (liquidity rules, compulsory savings programs etc.) gets you there. I don't see political will for a 5+% turnaround in revenues and/or spending in the boomers lifespan and probably not the next generation's either. Of course, financial repression itself is basically just a tax.

"If treasury markets don't want to roll over 1-year bonds at less, than, say, 10%, why would they want to hold Fed reserves at less than 10%?"

ReplyDeleteThat is a very interesting addition, providing a scenario in which the USA government debt crisis takes place.

But what are the reasons why anybody is going to ask 10% to treasuries?

a) because there is a risk that they cannot get back their principal. But if the FED have credibility saying that it will do "whatever it takes" to keep the debt markets working properly, acting as a buyer of last resort at prices well below that, this risk does not exist. We have been there before, and with a central bank with less credibility than the FED.

b) because there are alternative investments yielding more than 10%. In a stagnant economy with always higher regulatory barriers and little willingness for competition (particularly foreign one) and no stomach for "creative disruption" this is very unlikely (actually, less unlikely by the year).

Last week The Economist had an interesting article on that:

https://www.economist.com/schools-brief/2020/09/12/governments-can-borrow-more-than-was-once-believed

c) inflation: but if this is the mechanism to get inflation and the mechanism does not work, then the inflation will not happen. It is a bootstrapping that does not spark.

I do not see it and the markets either.

El Emperador,

Delete"a) because there is a risk that they cannot get back their principal. But if the FED have credibility saying that it will do whatever it takes to keep the debt markets working properly, acting as a buyer of last resort at prices well below that, this risk does not exist."

Except the FOMC (FED) cannot legally purchase Treasuries when they are auctioned. If there is a risk that bond buyers will not get their principle back, they simply won't bid on the bonds at auction and there is nothing the FED can do about it.

And it goes beyond even that. Maybe bond buyers don't like what the government is doing with the borrowed money (irrespective of the rate of return they may be receiving).

Bond markets can blow up for political reasons (genocide, nuclear escalation, etc.) just as easily as they can for economic reasons.

The legal limit is irrelevant as far as the buyers in the auction are confident in the FED role as secondary market maker. Confidence in the FED bond buying program sure is a condition.

DeleteGenocide and nuclear escalation can blow up the bond market at any debt to GDP level.

As far as the FOMC likes what the government is doing with the borrowed money and keeps a 'whaterver it takes' kind of compromise to 'hold' the bond market, there is no political reason (sort of a serious threath of an asteroid hitting the Earth near Washington) that can blow up the bond market.

Government bond market participants know very well that betting against the central banks are a reliable losing money strategy

El emperador,

DeleteNot only is the FOMC precluded from buying government debt at auction, they are also precluded from buying any security that does not guarantee the return of principle and interest.

See: https://www.federalreserve.gov/aboutthefed/section14.htm

"Every Federal reserve bank shall have power to buy and sell in the open market, under the direction and regulations of the Federal Open Market Committee, any obligation which is a direct obligation of, or fully guaranteed as to principal and interest by, any agency of the United States."

Most legal interpretations would say this is a limiting statement on the powers of the FOMC - if interest and principle on a security are not guaranteed, the FOMC cannot buy that security.

And so confidence in the FED is irrelevant when the FOMC is precluded from buying securities (even in the secondary market) where principle repayment is in question.

John, maybe it would be helpful to do a post titled something like: "High inflation would be bad, and here's why".

ReplyDeleteIsn't it quite easy to expand the use of indexed contracts (e.g. bond payments, wages, or real estate rentals)?

Currency holdings are negligible (and so are shoe leather costs).

Retailers don't need ink and paper to quote / change prices.

Many (but not all) tax brackets are inflation-adjusted.

I have to say, Dr Cochrane, when you introduce formalism into your blog posts it makes the read so much more enjoyable! You are one of the few economists that I've encountered that is not shy to introduce equations to your blog posts. It makes the literature far more accessible for the non-academic, like myself. Please keep up the great work!

ReplyDelete