Ken Rogoff has an interesting NBER Working paper "Costs and Benefits to Phasing Out Paper Currency."

Ken would like to get rid of paper currency in favor of all electronic transactions. I'm a big fan of low-cost electronic transactions using interest-paying electronic money. But I'm not ready to give up cash.

Ken has two basic points: The zero bound, and tax evasion / illegal economy.

Tuesday, December 30, 2014

Ruble Trouble

On Russia, the fall of the Ruble.

This is an interesting event on which to test out our various frameworks for thinking about macroeconomics and monetary economics.

Theories

There are three basic perspectives on exchange rates.

1. Multiple equilibria. Lots of words are used here, "speculative attacks," "sudden stops," "hot money," "self-confirming equilibria" "self-fulfilling prophecies" "contagion" and so on. Basically, the exchange rate can go up or down on the whims of traders. There is often some news sparking or coordinating the bust. Some of the mechanism is like bank runs, pointing to "illiquidity" rather than "insolvency" as the basic problem.

This has been a dominant paradigm since the early 1990s. I've been a bit suspicious both on the nebulousness of the economics (lots of buzzwords are always a bad sign), and since the analysis seems a bit reverse engineered to justify capital controls, currency controls, (i.e. expropriation of middle-class savers and poor currency-holders), IMF rescues, and lots of nannying by self-important institutions and their advisers who will monitor "imbalances," "control" who can buy or sell what, and so forth. But models are models and facts are facts.

2. Monetary. Exchange rates come from monetary events, and primarily the actions of central banks. For example, much of the analysis of the dollar strengthening relative to euro and yen attributes it to the idea that the US Fed has stopped QE and will soon raise rates, while the ECB and Japan seem about to start QE and keep rates low.

3. Fiscal theory. Exchange rates come fundamentally from expectations of future fiscal balance of governments; whether the governments will be able and willing to pay off their debts. If people see inflation or default coming, they bail out of the currency, which sends the price of the currency down. Inflation follows; immediately in the price of traded goods, more slowly in others.

Craig Burnside, Marty Eichenbaum and Sergio Rebelo's sequence of papers on currency crises, starting with JPE "Prospecitve Deficits and the Asian Currency Crisis" (ungated drafts here) was big in my thinking on these issues. They showed how each crisis involved a big claim on future government deficits. Prices fall, banks get in trouble, governments will bail out banks, so governments will be in trouble. Inflation lowers real salaries of government workers. And so on.

The "future" part is important. Earlier work on crises noticed that current debts or deficits were seldom large, governments in crises often had surprisingly large foreign currency reserves, and there were no signs of sudden monetary loosening. This earlier absence of a cause problem had led to much of the multiple-equilibrium literature. But money is like stock, and its value today depends on future "fundamentals."

Monetary and fiscal views are related. The question really is whether the central bank can stop an inflation and currency collapse by force of will, or whether it will have to cave in to fiscal pressures.

Most basically, a currency, like any asset, has a "fundamental" value, like a present value of dividends; it may have a "liquidity" value, like money; and it may have a "sunspot" or "multiple equilibrium value." The question is, which component is really at work in an event like this one -- or, realistically, how much of each? The money and fiscal views also much more clearly bring the currency into the picture.

So, as I read the stories of Russia's troubles, I'm thinking about which broad category of ideas best helps me to digest it. You can guess which one I think fits best. Yes, everyone likes to read the paper and see how it proves they were right all along. But at least being able to do that is the first step.

This is an interesting event on which to test out our various frameworks for thinking about macroeconomics and monetary economics.

Theories

There are three basic perspectives on exchange rates.

1. Multiple equilibria. Lots of words are used here, "speculative attacks," "sudden stops," "hot money," "self-confirming equilibria" "self-fulfilling prophecies" "contagion" and so on. Basically, the exchange rate can go up or down on the whims of traders. There is often some news sparking or coordinating the bust. Some of the mechanism is like bank runs, pointing to "illiquidity" rather than "insolvency" as the basic problem.

This has been a dominant paradigm since the early 1990s. I've been a bit suspicious both on the nebulousness of the economics (lots of buzzwords are always a bad sign), and since the analysis seems a bit reverse engineered to justify capital controls, currency controls, (i.e. expropriation of middle-class savers and poor currency-holders), IMF rescues, and lots of nannying by self-important institutions and their advisers who will monitor "imbalances," "control" who can buy or sell what, and so forth. But models are models and facts are facts.

2. Monetary. Exchange rates come from monetary events, and primarily the actions of central banks. For example, much of the analysis of the dollar strengthening relative to euro and yen attributes it to the idea that the US Fed has stopped QE and will soon raise rates, while the ECB and Japan seem about to start QE and keep rates low.

3. Fiscal theory. Exchange rates come fundamentally from expectations of future fiscal balance of governments; whether the governments will be able and willing to pay off their debts. If people see inflation or default coming, they bail out of the currency, which sends the price of the currency down. Inflation follows; immediately in the price of traded goods, more slowly in others.

Craig Burnside, Marty Eichenbaum and Sergio Rebelo's sequence of papers on currency crises, starting with JPE "Prospecitve Deficits and the Asian Currency Crisis" (ungated drafts here) was big in my thinking on these issues. They showed how each crisis involved a big claim on future government deficits. Prices fall, banks get in trouble, governments will bail out banks, so governments will be in trouble. Inflation lowers real salaries of government workers. And so on.

The "future" part is important. Earlier work on crises noticed that current debts or deficits were seldom large, governments in crises often had surprisingly large foreign currency reserves, and there were no signs of sudden monetary loosening. This earlier absence of a cause problem had led to much of the multiple-equilibrium literature. But money is like stock, and its value today depends on future "fundamentals."

Monetary and fiscal views are related. The question really is whether the central bank can stop an inflation and currency collapse by force of will, or whether it will have to cave in to fiscal pressures.

Most basically, a currency, like any asset, has a "fundamental" value, like a present value of dividends; it may have a "liquidity" value, like money; and it may have a "sunspot" or "multiple equilibrium value." The question is, which component is really at work in an event like this one -- or, realistically, how much of each? The money and fiscal views also much more clearly bring the currency into the picture.

So, as I read the stories of Russia's troubles, I'm thinking about which broad category of ideas best helps me to digest it. You can guess which one I think fits best. Yes, everyone likes to read the paper and see how it proves they were right all along. But at least being able to do that is the first step.

Monday, December 22, 2014

Inequality at WSJ -- the oped

This is a Wall Street Journal oped on inequality. With 30 days passed, I can post it here. It's a much edited version of my evolving "Why and How we Care About Inequality" essay.

What the ‘Inequality’ Warriors Really Want

Progressives decry inequality as the world’s most pressing economic problem. In its name, they urge much greater income and wealth taxation, especially of the reviled top 1% of earners, along with more government spending and controls—higher minimum wages, “living” wages, comparable worth directives, CEO pay caps, etc.

Inequality may be a symptom of economic problems. But why is inequality itself an economic problem? If some get rich and others get richer, who cares? If we all become poor equally, is that not a problem? Why not fix policies and problems that make it harder to earn more?

What the ‘Inequality’ Warriors Really Want

Progressives decry inequality as the world’s most pressing economic problem. In its name, they urge much greater income and wealth taxation, especially of the reviled top 1% of earners, along with more government spending and controls—higher minimum wages, “living” wages, comparable worth directives, CEO pay caps, etc.

Inequality may be a symptom of economic problems. But why is inequality itself an economic problem? If some get rich and others get richer, who cares? If we all become poor equally, is that not a problem? Why not fix policies and problems that make it harder to earn more?

Sunday, December 21, 2014

Autopsy

Autopsy for Keynesian Economics. (I don't get to pick the titles BTW) A Wall Street Journal Oped. I'm trying for something cheery at Christmas, and a response to the many recent opeds that ISLM is just great and winning the battle of ideas. As usual, the whole thing will be here in a month.

Update: Hoover has an ungated version here; Cato has an ungated version here.

This year the tide changed in the economy. Growth seems finally to be returning. The tide also changed in economic ideas. The brief resurgence of traditional Keynesian ideas is washing away from the world of economic policy.

No government is remotely likely to spend trillions of dollars or euros in the name of “stimulus,” financed by blowout borrowing. The euro is intact: Even the Greeks and Italians, after six years of advice that their problems can be solved with one more devaluation and inflation, are sticking with the euro and addressing—however slowly—structural “supply” problems instead.Read more at WSJ...

Update: Hoover has an ungated version here; Cato has an ungated version here.

Saturday, December 20, 2014

Deflation links

Commenter Zack sent the following Paul Krugman links and quotes, which deserve promotion from the comments section.

"But deflation is a huge risk — and getting out of a deflationary trap is very, very hard. We truly are flirting with disaster."

http://krugman.blogs.nytimes.com/2009/02/04/about-that-deflation-risk/

"So we're really heading into Japanese-style deflation territory"

http://krugman.blogs.nytimes.com/2009/07/02/smells-like-deflation/

"So tell me why we aren’t looking at a very large risk of getting into a deflationary trap, in which falling prices make consumers and businesses even less willing to spend." http://krugman.blogs.nytimes.com/2009/01/10/risks-of-deflation-wonkish-but-important/

"But the risk that America will turn into Japan — that we’ll face years of deflation and stagnation — seems, if anything, to be rising."

http://www.nytimes.com/2009/05/04/opinion/04krugman.html

"What I take from this is that deflation isn’t some distant possibility — it’s already here by some measures, not far off by others."

http://krugman.blogs.nytimes.com/2010/07/11/trending-toward-deflation/

"Worst of all is the possibility that the economy will, as it did in the ’30s, end up stuck in a prolonged deflationary trap."

http://www.nytimes.com/2009/02/06/opinion/06krugman.html?partner=permalink&exprod=permalink&_r=0

As we know, it didn't turn out that way. We have had positive inflation for 6 years.

Why does this matter? Normally, it doesn't and it shouldn't.

"But deflation is a huge risk — and getting out of a deflationary trap is very, very hard. We truly are flirting with disaster."

http://krugman.blogs.nytimes.com/2009/02/04/about-that-deflation-risk/

"So we're really heading into Japanese-style deflation territory"

http://krugman.blogs.nytimes.com/2009/07/02/smells-like-deflation/

"So tell me why we aren’t looking at a very large risk of getting into a deflationary trap, in which falling prices make consumers and businesses even less willing to spend." http://krugman.blogs.nytimes.com/2009/01/10/risks-of-deflation-wonkish-but-important/

"But the risk that America will turn into Japan — that we’ll face years of deflation and stagnation — seems, if anything, to be rising."

http://www.nytimes.com/2009/05/04/opinion/04krugman.html

"What I take from this is that deflation isn’t some distant possibility — it’s already here by some measures, not far off by others."

http://krugman.blogs.nytimes.com/2010/07/11/trending-toward-deflation/

"Worst of all is the possibility that the economy will, as it did in the ’30s, end up stuck in a prolonged deflationary trap."

http://www.nytimes.com/2009/02/06/opinion/06krugman.html?partner=permalink&exprod=permalink&_r=0

As we know, it didn't turn out that way. We have had positive inflation for 6 years.

Why does this matter? Normally, it doesn't and it shouldn't.

Thursday, December 18, 2014

Real or risk-neutral wolf?

I think there are deep lessons from this chart. And not the simple "economists are always wrong," or even "economic forecasts are biased." The chart offers a nice warning about how we interpret surveys.

Expectations matter a lot to modern macroeconomics. But you can't directly see expectations. So many researchers have turned to surveys to measure what people say they "expect." And they find all sorts of weird things. People "expect" stock returns to be implausibly high in booms, and low in busts. Professional forecasters "expect" interest rates always to go up.

The trouble here, I think, is that we have forgotten what "expect" means to the average person.

Wednesday, December 17, 2014

1994?

Torsten Slok at Deutsche Bank sends the graph, along with some musings on the eternal question: When (if?) interest rates rise, will it look like 1994, or like 2004? Will rates rise quickly, leading to a bath in long-term bonds? Or will rates rise slowly and predictability?

The graph shows you actual short term rates (red) and forward curves. As this lovely graph points out, the forward curve has been predicting rises in rates for years now. And it's been wrong over and over again. Economists all over have been forecasting a robust recovery too, and that hasn't happened either.

(To non-finance people: The forward rate is the rate you can lock in today to borrow in the future. So the forward curve ought to reflect where the market expects interest rates to go. If people expect rates to rise more than the forward curve, they rush to lock in now, which drives up the forward curve. Also, the forward curve is a cutoff between making and losing on long-term bonds. If interest rates rise following the forward curve, then long bonds and short bonds give the same return. If rates rise slower, long-term bondholders make more money. If rates rise faster, long bonds make less than short or even lose money. So, should you buy long term bonds? Compare your interest rate forecast to the last dashed line and decide.)

Torsten:

The chart .. makes you humble when it comes to the timing of the first rate hike.Indeed.

But once the Fed starts hiking, they will likely raise rates faster than the market currently is anticipating. Think about it: The Fed has basically decided that they will only start hiking rates once there are signs of inflation.. If the economy is overheating, then raising the fed funds rate to 0.5% is not going to slow the economy down....To cool the economy down, the fed funds rate needs to be above the neutral fed funds rate, which we estimate to be 3.5%...to get inflation under control, the Fed will likely have to raise rates well above the neutral level, potentially above 5%...So his scenario is, interest rates low and more good times for long term bonds until (if) inflation substantially exceeds 2%, then a big rout, as small rises will not do much quickly to dampen inflation. More like 1994.

An interesting view into the brains of bond traders:

Monday, December 15, 2014

Who is afraid of a little deflation? Op-Ed

Who is Afraid of a Little Deflation?

With European inflation declining to 0.3%, and U.S. inflation slowing, a specter now haunts the Western world. Deflation, the Economist recently proclaimed, is a “pernicious threat” and “the world’s biggest economic problem.” Christine Lagarde , managing director of the International Monetary Fund, called deflation an “ogre” that could “prove disastrous for the recovery.”

True, a sudden, large and sharp collapse in prices, such as occurred in the early 1920s and 1930s, would be a problem: Debtors might fail, some prices and wages might not adjust quickly enough. But these deflations resulted directly from financial panics, when central banks couldn’t or didn’t accommodate a sudden demand for money.

The worry today is a slow slide toward falling prices, maybe 1% to 2% annually, with perpetually near-zero short-term interest rates. This scenario would unfold alongside positive, if sluggish, growth, ample money and low credit spreads, with financial panic long passed. And slight deflation has advantages. Milton Friedman long ago recognized slight deflation as the “optimal” monetary policy, since people and businesses can hold lots of cash without worrying about it losing value. So why do people think deflation, by itself, is a big problem?

1) Sticky wages. A common story is that employers are loath to cut wages, so deflation can make labor artificially expensive. With product prices falling and wages too high, employers will cut back or close down.

Loggerheads

Government Debt Management at the Zero Lower Bound is a very nice and interesting paper by

Robin Greenwood,

Sam Hanson,

Josh Rudolph, and Larry Summers.

First point, what the Fed taketh away, the Treasury giveth. (Hence the title of this post). The Fed bought lots of long-term debt, with the idea that this would raise the price, lower the interest rate on the long-term debt, and thus stimulate the economy.

At the same time, however, the Treasury was selling lots of long-term debt. Interest rates are very low, and debts are high, so it's a great time to lock in low-rate financing. Homeowners and businesses are doing the same thing.

|

| Figure 1. Comparing Quantitative Easing and Treasury Maturity Extension, 2007–2014 ...the cumulative change in 10-year equivalents (scaled as a percentage of GDP) associated with the respective balance sheet policies undertaken by the Federal Reserve and the Treasury. Positive values increase the interest rate risk placed in public hands (Treasury policies), while negative values decrease it (typically Fed QE, but also Treasury maturity shortening in 2008–2009). |

First point, what the Fed taketh away, the Treasury giveth. (Hence the title of this post). The Fed bought lots of long-term debt, with the idea that this would raise the price, lower the interest rate on the long-term debt, and thus stimulate the economy.

At the same time, however, the Treasury was selling lots of long-term debt. Interest rates are very low, and debts are high, so it's a great time to lock in low-rate financing. Homeowners and businesses are doing the same thing.

Thursday, December 11, 2014

Level, Slope and Curve for Stocks

"The Level, Slope and Curve Factor Model for Stocks" is an interesting and important empirical finance paper by Charles Clarke at the University of Connecticut.

Charles uses the Fama-French (2008) variables to forecast stock returns, i. e., size, book to market, momentum, net issues, accruals, investment, and profitability. \[ Ret_{i,t+1} = \beta_0 + \beta_1 Size_{i,t} + \beta_2 BtM_{i,t} + \beta_3 Mom_{i,t} + \beta_4 zeroNS_{i,t} + \beta_5 NS_{i,t} + \beta_6 negACC_{i,t} + \] \[ + \beta_7 posACC_{i,t} + \beta_8 dAtA_{i,t} + \beta_9 posROE_{i,t} + \beta_{10} negROE_{i,t} + e_{i,t+1} \] He forms 25 portfolios based on the predicted average return from this regression, from high to low expected returns. Then, he finds the principal components of these 25 portfolio returns.

And the result is... hold your breath... Level, Slope and Curvature! The picture on the left plots the weights and loadings of the first three factors. The x axis are the 25 portfolios, ranked from the one with low average returns to 25 with high average return. The graph represents the weights -- how you combine each portfolio to form each factor in turn -- and also the loadings -- how much each portfolio return moves when the corresponding factor moves by one.

No surprise, the 3 factors explain almost all the variance of the 25 portfolios returns, and the three factors provide a factor pricing model with very low alphas; the APT works.

Now, why am I so excited about this paper?

Charles uses the Fama-French (2008) variables to forecast stock returns, i. e., size, book to market, momentum, net issues, accruals, investment, and profitability. \[ Ret_{i,t+1} = \beta_0 + \beta_1 Size_{i,t} + \beta_2 BtM_{i,t} + \beta_3 Mom_{i,t} + \beta_4 zeroNS_{i,t} + \beta_5 NS_{i,t} + \beta_6 negACC_{i,t} + \] \[ + \beta_7 posACC_{i,t} + \beta_8 dAtA_{i,t} + \beta_9 posROE_{i,t} + \beta_{10} negROE_{i,t} + e_{i,t+1} \] He forms 25 portfolios based on the predicted average return from this regression, from high to low expected returns. Then, he finds the principal components of these 25 portfolio returns.

|

| Source: Charles Clarke |

And the result is... hold your breath... Level, Slope and Curvature! The picture on the left plots the weights and loadings of the first three factors. The x axis are the 25 portfolios, ranked from the one with low average returns to 25 with high average return. The graph represents the weights -- how you combine each portfolio to form each factor in turn -- and also the loadings -- how much each portfolio return moves when the corresponding factor moves by one.

No surprise, the 3 factors explain almost all the variance of the 25 portfolios returns, and the three factors provide a factor pricing model with very low alphas; the APT works.

Now, why am I so excited about this paper?

Monday, December 8, 2014

Policy penance

The last few posts haven't worked out so well, that's for sure. After a too-grumpy reaction to Alan Blinder's review, I wanted to say something nice and find common ground with the "what's wrong with macro" articles and even Krugman's posts. In doing so I was much too quick and superficial in characterizing what's going on at high levels of our policy institutions. The only result was that I managed to annoy all my friends and colleagues at the Fed, IMF, and so on.

As penance, I'll try a blog post that more accurately characterizes the interaction of research and policy, "Keynesian" and modern economics, and so on, as I see it.

If we look one step below the political level, for example at the FOMC minutes and what research staff are up to at institutions like Fed and IMF, you see a very sophisticated interaction between the ideas of modern economic research and policy. The FOMC minutes and speeches by board members (all easy to find on the Fed's website) are a great source. The FOMC seems, to an outsider, like the world's highest-level debating club on modern macroeconomics.

On many of the dividing lines between traditional Keynesian and modern economics, the policy discussion is decidedly modern.

As penance, I'll try a blog post that more accurately characterizes the interaction of research and policy, "Keynesian" and modern economics, and so on, as I see it.

If we look one step below the political level, for example at the FOMC minutes and what research staff are up to at institutions like Fed and IMF, you see a very sophisticated interaction between the ideas of modern economic research and policy. The FOMC minutes and speeches by board members (all easy to find on the Fed's website) are a great source. The FOMC seems, to an outsider, like the world's highest-level debating club on modern macroeconomics.

On many of the dividing lines between traditional Keynesian and modern economics, the policy discussion is decidedly modern.

Friday, December 5, 2014

Uber stars vs. taxi regulators

Uber.gov is a great story about Uber, taxi scams, captured regulation, and so on. Have fun.

...Read the rest here

How The “Sin City Shuffle” Works There are two main routes to get from the Vegas airport to the Strip. One of them is illegal. To figure out which one you’re on, apply this test: Look outside. If you can’t find outside, you’re in a tunnel—which means you’re being ripped off.

The I-215 tunnel adds about $10 to your fare, but one in three cabbies “longhauled” undercover cops through it anyway. The country hasn’t seen this kind of brazenness since Bankerty Robberson opened a Skimask Hut outside Wells Fargo in 1979.

What can possibly be done about such a confounding crime? I had plenty of time to research this on a recent trip to Vegas, while my own cabbie, Mickey, drove me to the Bellagio by way of Montpelier, Vermont.

Uber’s absurd answer to longhauling is straight from your childhood: When a driver behaves badly, he only gets one star. Within hours, Uber adjusts your fare. Their systems can do this automatically because they have everything they need to calculate an “ideal” fare—start point, end point, traffic conditions, and past fares. If the driver keeps scamming others, he automatically gets fired.

But Nevada officials found fault in Uber’s stars. In fact, they kicked the company out of town for not protecting tourists.

Thursday, December 4, 2014

What's wrong with macro?

Reflecting on my overly grumpy last post, as well as many recent Krugman columns, I think there is really a fundamental consensus here.

There is, in fact, a sharp divide between macroeconomics used in the top levels of policy circles, and that used in academia.

There is, in fact, a sharp divide between macroeconomics used in the top levels of policy circles, and that used in academia.

Wednesday, December 3, 2014

Blinders

Alan Blinder has what looked like an interesting-looking essay in the New York Review of Books, "What's the matter with economics?" Alan has usually been thoughtful, the WSJ house liberal columnist, so I approached it hoping for well-reasoned argument I might disagree with, but be interested by and learn something from. And it started well, pointing out the many things on which economists all agree and policy does not.

Alas, then we get to macro. Something about stimulus sends people off the deep end. One little quote pretty much summarizes the tone and (lack of) usefulness of the whole thing:

Am I wrong that graduate programs do not teach any Keynesian economics? I went to look at the Princeton University Economics Department graduate course offerings. Following up on the ones titled "macro," I found

Alas, then we get to macro. Something about stimulus sends people off the deep end. One little quote pretty much summarizes the tone and (lack of) usefulness of the whole thing:

The great Milton Friedman of the University of Chicago, a favorite target of Madrick, may have been right or wrong; but he was certainly far to the right. Much the same can be said of several other economists cited by Madrick as representing the mainstream. For example, he quotes John Cochrane, also of the University of Chicago, as saying in 2009 that Keynesian economics is “not part of what anybody has taught graduate students since the 1960s. [Keynesian ideas] are fairy tales that have been proved false.” The first statement is demonstrably false; the second is absurd. People can and do argue over the macroeconomic views associated with the so-called Chicago School, but it’s clear that the views of that school are far from the mainstream."Demonstrably false" and "absurd" are pretty strong.

Am I wrong that graduate programs do not teach any Keynesian economics? I went to look at the Princeton University Economics Department graduate course offerings. Following up on the ones titled "macro," I found

Tuesday, December 2, 2014

McCloskey on Piketty and Friends

Deirdre McCloskey has written an excellent essay reviewing Thomas Piketty’s Capital in the Twenty-First Century.

As an economic historian and historian of economic ideas, McCloskey can place the arguments into the framework of centuries-old ideas (and fallacies) as few others can. She has read philosophy and "social ethics." She can even knowledgeably review the literary references.

Her central point: "trade-based betterment," (she wisely avoids "capitalism" to emphasize that the focus on "capital" is about a hundred years out of date) has raised living standards by factors of 30 or more -- much more if you think about health, freedom, lifespan, tavel, etc. unavailable at any price in 1800; it has led to much greater equality in many things that count, such as consumption, health and so on; and stands to do so again if we do not kill the goose that laid these golden eggs. From late in the review,

On the long history of fashionable worrying:

As an economic historian and historian of economic ideas, McCloskey can place the arguments into the framework of centuries-old ideas (and fallacies) as few others can. She has read philosophy and "social ethics." She can even knowledgeably review the literary references.

Her central point: "trade-based betterment," (she wisely avoids "capitalism" to emphasize that the focus on "capital" is about a hundred years out of date) has raised living standards by factors of 30 or more -- much more if you think about health, freedom, lifespan, tavel, etc. unavailable at any price in 1800; it has led to much greater equality in many things that count, such as consumption, health and so on; and stands to do so again if we do not kill the goose that laid these golden eggs. From late in the review,

Redistribution, although assuaging bourgeois guilt, has not been the chief sustenance of the poor....If all profits in the American economy were forthwith handed over to the workers, the workers ... would be 20 percent or so better off, right now....But such

one-time redistributions are two orders of magnitude smaller in helping the poor than the 2,900 percent Enrichment from greater productivity since 1800. Historically speaking 25 percent is to be compared with a rise in real wages 1800 to the present by a factor of 10 or 30, which is to say 900 or 2,900 percent.As a too-long post on a far-too-long review of a enormously-too-long book, I'll pass on some particularly good bits with comment.

On the long history of fashionable worrying:

Monday, December 1, 2014

Sequester and vortex redux.

I posted this last week, but I was unaware at the time of the Paul Krugman's "Keynes is slowly winning" post; Tyler Cowen's 15-point response, documenting not only Keynesian failures but more importantly how the policy world is in fact moving decidedly away from Keynesian ideas, right or wrong (that was Krugman's point); and Krugman's retort, predictably snarky and disconnected from anything Cowen said, changing the subject from Keynesian ideas are winning to the standard what a bunch of morons they're not Keynesians though I keep telling them to be. (I like Krugman's chart though. I see a glass half full -- look at all those nominal wage cuts, even in Spain! And look how many people got raises.)

In that context, I added two "Facts in front of our noses." Keynsesians, and Krugman especially, said the sequester would cause a new recession and even air traffic control snafus. Instead, the sequester, though sharply reducing government spending, along with the end of 99 week unemployment insurance, coincided with increased growth and a big surprise decline in unemployment. And ATC is no more or less chaotic than ever. Keynesians, and Krugman especially, kept warning of a "deflation vortex." We and Europe still don't have any deflation, and even Japan never had a "vortex." These are not personal prognostications, but widely shared and robust predictions of a Keynesian worldview. Two strikes. Batter up.

The original: (This is a re-post if you saw it the first time around, but easier to copy and paste than link.)

|

| Multiplier? What multiplier? |

Saturday, November 29, 2014

Frameworks for Central Banking in the Next Century

The special issue of the JEDC containing papers from the conference "Frameworks for Central Banking in the Next Century" is available until Jan 18 online for free. My "monetary policy with interest on reserves" is here. Alas, Elsevier doesn't allow me to post a pdf and only allows free access until Jan 18, so if you want pdfs grab them now.

The lineup is pretty impressive. Of those I have read, I highly recommend Sargent, Prescott, Ohanian, Ferguson and Plosser to blog readers. In particular, if you thought Friedman was always and everywhere MV=PY and 4%, read Sargent.

The lineup:

Wednesday, November 26, 2014

Target the spread?

To send you off with some more Thanksgiving good cheer, here is another out of the box Neo-Fisherian idea.

Perhaps the Fed (or the Treasury) should target the spread between real and nominal interest rates.

Above, I plotted the real (TIPS) and nominal 5 year rates. By the usual relationship \[ i_t = r_t + E_t \left[ \pi_{t+1} \right] \] we typically interpret the difference between real (r) and nominal (i) rate as the expected inflation rate.

Now, the usual Neo-Fisherian idea says, peg the nominal rate (i), eventually the real rate (r) will settle down, and inflation will follow the nominal rate. It's contentious, among other reasons, because we're not quite sure how long it takes the real rate to settle down, and there is some fear that real rate movements induce a temporarily opposite move in inflation.

So why not target the spread? The Fed or Treasury could easily say that the yield difference between TIPS and Treasuries shall be 2%. (I prefer 0, but the level of the target is not the point.) Bring us your Treasuries, say, and we will give you back 1.02 equivalent TIPS. Give us your TIPS, and we will give you back 0.98 Treasuries. (I'm simplifying, but you get the idea.) They could equivalently simply intervene in each market until market prices go where they want. Or offer nominal-for-indexed swaps at a fixed rate.

Now, I think, the Neo-Fisherian logic is even tighter. If the government targets the difference \( i_t - r_t \), in a firmly committed way, \( E_t \left[ \pi_{t+1} \right] \) is going to have to adjust. I plotted 5 years, because I'm attracted to the idea of nailing down 5 year inflation expectations, but the general idea works across the maturity spectrum.

Sequester, growth, and the deflation that did not bark.

|

| Multiplier? What multiplier? |

The economy expanded at its fastest pace in more than a decade during the spring and summer,... Gross domestic product...grew at a seasonally adjusted annual rate of 3.9% in the third quarter... combined growth rate in the second and third quarters at 4.25%, affirming the best six-month pace since the second half of 2003."

The upward revision to overall growth, driven by [sic] stronger consumer and business spending and a smaller drag from inventory investment, surprised economists...Paul Krugman, February 22 2013, "Sequester of Fools"

The sequester, by contrast, will probably cost “only” around 700,000 jobs.New York Times, Februrary 21 2013, "Why Taxes Have to Go Up"

Democrats and Republicans remain at odds on how to avoid a round of budget cuts so deep and arbitrary that to allow them now could push the economy back into recession. The cuts, known as a sequester, will kick in March 1 [my emphasis]

Sunday, November 23, 2014

Behavioral Political Economy

I was interested to read "Behavioral Political Economy: A Survey" by Jan Schnellenbach and Christian Schubert. (HT marginal revolution's irresistible links.)

Context: I have long been puzzled at the high correlation between behavioral economics and interventionism.

People do dumb things, in somewhat predictable ways. It follows that super-rational aliens or divine guidance could make better choices for people than they often make for themselves. But how does it follow that the bureaucracy of the United States Federal Government can coerce better choices for people than they can make for themselves?

For if psychology teaches us anything, it is that people in groups do even dumber things than people do as individuals -- groupthink, social pressure, politics, and so on -- and that people do even dumber things when they are insulated from competition than when their decisions are subject to ruthless competition.

So on logical grounds, I would have thought that behavioral economists would be libertarians. Where are the behavioral Stigler, Buchanan, Tullock, etc.? The case for free markets never was that markets are perfect. It has always been that government meddling is worse. And behavioral economics -- the application of psychology to economics -- seems like a great tool for understanding why governments do so badly. It might also inform us how they might work better; why some branches of government and some governments work better than others.

This nice paper got my attention, since the paper says that's starting to happen.

Context: I have long been puzzled at the high correlation between behavioral economics and interventionism.

People do dumb things, in somewhat predictable ways. It follows that super-rational aliens or divine guidance could make better choices for people than they often make for themselves. But how does it follow that the bureaucracy of the United States Federal Government can coerce better choices for people than they can make for themselves?

For if psychology teaches us anything, it is that people in groups do even dumber things than people do as individuals -- groupthink, social pressure, politics, and so on -- and that people do even dumber things when they are insulated from competition than when their decisions are subject to ruthless competition.

So on logical grounds, I would have thought that behavioral economists would be libertarians. Where are the behavioral Stigler, Buchanan, Tullock, etc.? The case for free markets never was that markets are perfect. It has always been that government meddling is worse. And behavioral economics -- the application of psychology to economics -- seems like a great tool for understanding why governments do so badly. It might also inform us how they might work better; why some branches of government and some governments work better than others.

This nice paper got my attention, since the paper says that's starting to happen.

...Assuming cognitive biases to be present in the market, but not in politics, behavioral economists often call for government to intervene in a “benevolent” way. Recently, however, political economists have started to apply behavioral economics insights to the study of political processes, thereby re-establishing a unified methodology. This paper surveys the current state of the emerging field of “Behavioral Political Economy”I came away horribly disappointed. Not with the paper, but with the state of the literature that the authors ably summarize.

Saturday, November 22, 2014

Writing compactly

A correspondent sends a suggested edit of a part of my writing tips for PhD students

With markup

Keep the paper as short as

possible.

Be concise. Every word must count.

As you edit the paper ask yourself constantly, “can I make the

same my point in less space?”

and “Do Must I really have

to say this?” Final papers should be no more than under 40

pages, drafts should be

shorter. (Do as I say, not as I do!) Shorter is better.

With markup

Keep it short

Clean:

Keep it short

Be

concise. Every word must count. As you edit, ask yourself, “can I make my point

in less space?” and “must say this?” Final papers should be under 40 pages,

drafts shorter. Shorter is better.

Well, I did say "do as I say, don't do as I do!"

Friday, November 21, 2014

Segregated Cash Accounts

An important little item from the just released minutes of the October Federal Open Market Committee meeting will be interesting to people who follow monetary policy and financial reform issues.

The simple version, as I understand it, seems like great news. Basically, a company can deposit money at a bank, and the bank turns around and invests that money in interest-paying reserves at the Fed. Unlike regular deposits, which you lose if the bank goes under, (these deposits are much bigger than the insured limit) the depositor has a collateral claim to the reserves at the Fed.

This is then exactly 100% reserve, bankruptcy-remote, "narrow banking" deposits. I argued for these in "toward a run-free financial system" as a substitute for all the run-prone shadow-banking that fell apart in the financial crisis. (No, this isn't going to siphon money away from bank lending, as the Fed buys Treasuries to issue reserves. The volume of bank lending stays the same.)

Finally, the manager reported on potential arrangements that would allow depository institutions to pledge funds held in a segregated account at the Federal Reserve as collateral in borrowing transactions with private creditors and would provide an additional supplementary tool during policy normalization; the manager noted possible next steps that the staff could potentially undertake to investigate the issues related to such arrangements.A slide presentation by the New York Fed's Jamie McAndrews explains it.

The simple version, as I understand it, seems like great news. Basically, a company can deposit money at a bank, and the bank turns around and invests that money in interest-paying reserves at the Fed. Unlike regular deposits, which you lose if the bank goes under, (these deposits are much bigger than the insured limit) the depositor has a collateral claim to the reserves at the Fed.

This is then exactly 100% reserve, bankruptcy-remote, "narrow banking" deposits. I argued for these in "toward a run-free financial system" as a substitute for all the run-prone shadow-banking that fell apart in the financial crisis. (No, this isn't going to siphon money away from bank lending, as the Fed buys Treasuries to issue reserves. The volume of bank lending stays the same.)

Dusty corners of the market

Thursday and Friday I attended the NBER Asset Pricing conference. As usual it was full of interesting papers and sharp discussion. Program here.

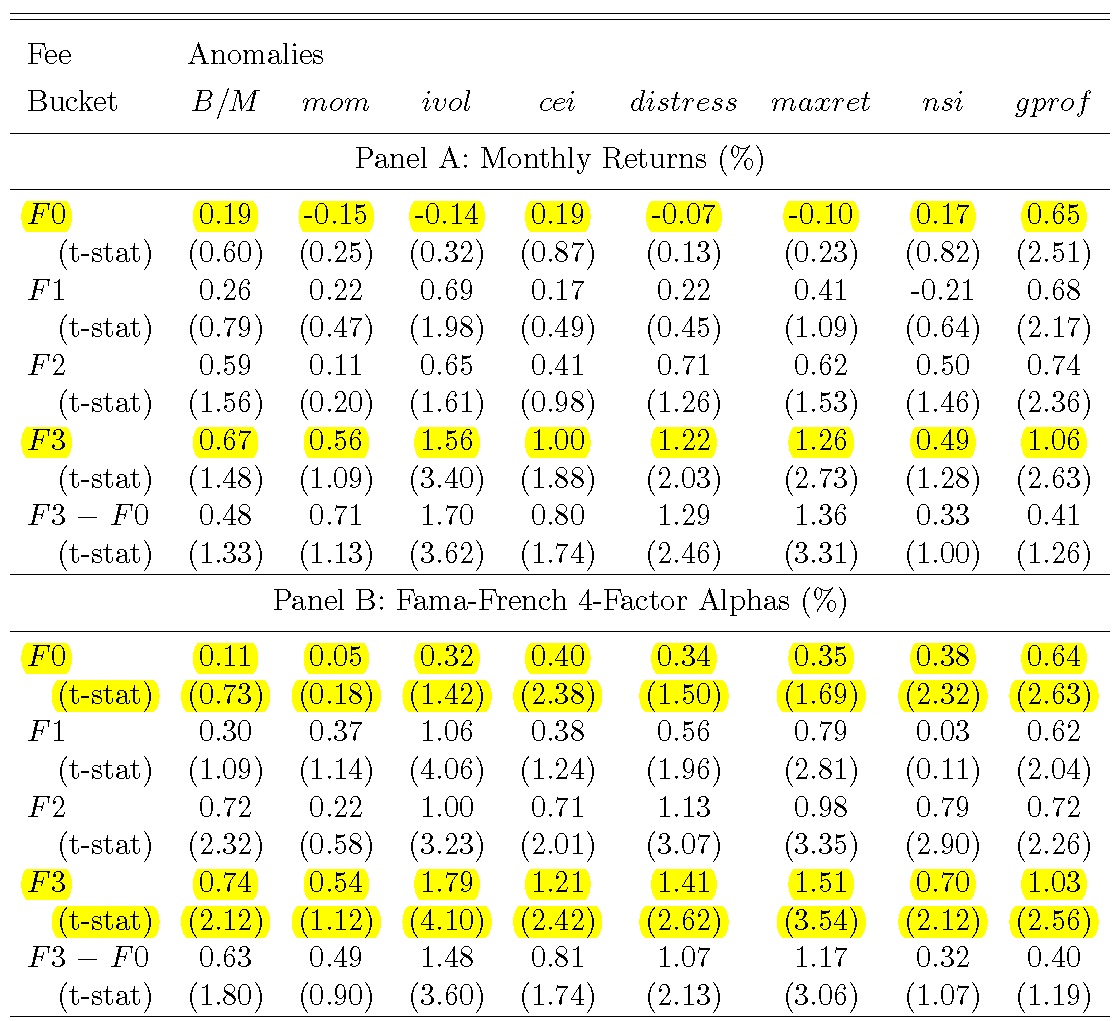

A bloggable insight: Itamar Drechsler, and Qingyi F. Drechsler "The Shorting Premium and Asset Pricing Anomalies." They carefully found the cost to short-sell stocks.

Here's their Table 5. F0 are all the easy to short stocks. F3 are the hardest to short stocks. They construct long-short anomaly portfolios in each group. "F 0 Mom" for example is the average monthly return of past winners minus that of past losers, among the easy to short stocks. Now compare the F0 row to the F3 row. The anomaly returns only work in the hard-to-short portfolios.

The second panel shows Fama-French alphas, which are better measured. The sample is alas small. But the result is cool.

The implication is that a lot of anomalies exist only in hard to trade stocks. There is a lot more in the paper, of course.

Table 5: Anomaly Returns Conditional on Shorting Fees

We divide the short-fee deciles from Table 2 into four buckets. Deciles 1-8, the low-fee stocks, are placed into the F0 bucket. Deciles 9 and 10, the intermediate- and high-fee stocks, are divided into three equal-sized buckets, F1 to F3, based on shorting fee, with F3 containing the highest fee stocks. We then sort the stocks within each bucket into portfolios based on the anomaly characteristic and let the bucket's long-short anomaly return be given by the di erence between the returns of the extreme portfolios. Due to the larger number of stocks in the F0 bucket, we sort it into deciles based on the anomaly characteristic, while F1 to F3 are sorted into terciles. Panel A reports the monthly anomaly long-short returns for each anomaly and bucket. Panel B reports the corresponding FF4 alphas. Panel C reports the FF4 + CME alphas. The sample period is January 2004 to December 2013.

(From Table 4 caption) The anomalies are: value-growth (B=M), momentum (mom), idiosyncratic volatility (ivol), composite equity issuance (cei), nancial distress (distress), max return (maxret), net share issuance (nsi), and gross pro tability (gprof). The sample is January 2004 to December 2013.

A bloggable insight: Itamar Drechsler, and Qingyi F. Drechsler "The Shorting Premium and Asset Pricing Anomalies." They carefully found the cost to short-sell stocks.

Here's their Table 5. F0 are all the easy to short stocks. F3 are the hardest to short stocks. They construct long-short anomaly portfolios in each group. "F 0 Mom" for example is the average monthly return of past winners minus that of past losers, among the easy to short stocks. Now compare the F0 row to the F3 row. The anomaly returns only work in the hard-to-short portfolios.

The second panel shows Fama-French alphas, which are better measured. The sample is alas small. But the result is cool.

The implication is that a lot of anomalies exist only in hard to trade stocks. There is a lot more in the paper, of course.

Table 5: Anomaly Returns Conditional on Shorting Fees

We divide the short-fee deciles from Table 2 into four buckets. Deciles 1-8, the low-fee stocks, are placed into the F0 bucket. Deciles 9 and 10, the intermediate- and high-fee stocks, are divided into three equal-sized buckets, F1 to F3, based on shorting fee, with F3 containing the highest fee stocks. We then sort the stocks within each bucket into portfolios based on the anomaly characteristic and let the bucket's long-short anomaly return be given by the di erence between the returns of the extreme portfolios. Due to the larger number of stocks in the F0 bucket, we sort it into deciles based on the anomaly characteristic, while F1 to F3 are sorted into terciles. Panel A reports the monthly anomaly long-short returns for each anomaly and bucket. Panel B reports the corresponding FF4 alphas. Panel C reports the FF4 + CME alphas. The sample period is January 2004 to December 2013.

(From Table 4 caption) The anomalies are: value-growth (B=M), momentum (mom), idiosyncratic volatility (ivol), composite equity issuance (cei), nancial distress (distress), max return (maxret), net share issuance (nsi), and gross pro tability (gprof). The sample is January 2004 to December 2013.

Thursday, November 20, 2014

Inequality at WSJ

"What the Inequality Warriors Really Want" a Wall Street Journal oped on inequality. It's a much edited version of my evolving "Why and How we Care About Inequality" essay. Any writers will appreciate the pain that cutting so much caused.

As usual I can't post the whole thing for 30 days, but you might find the WSJ short version interesting, especially if you couldn't slog through the whole thing. Their comments might be fun too.

As usual I can't post the whole thing for 30 days, but you might find the WSJ short version interesting, especially if you couldn't slog through the whole thing. Their comments might be fun too.

Monday, November 17, 2014

Guilds

_van_het_Amsterdamse_lakenbereidersgilde_-_Google_Art_Project.jpg/1024px-Rembrandt_-_De_Staalmeesters-_het_college_van_staalmeesters_(waardijns)_van_het_Amsterdamse_lakenbereidersgilde_-_Google_Art_Project.jpg) |

| The Syndics of the Drapers' Guild by Rembrandt, 1662. |

..the behavior of guilds can best be understood as being aimed at securing rents for guild members; guilds then transferred a share of these rents to political elites in return for granting and enforcing the legal privileges that enabled guilds to engage in rent extraction.The paper nicely works through all the standard pro-guild and pro-regulation arguments. If you just replace "Guild" with "regulatory agency" it sounds pretty fresh.

Did guilds provide contract enforcement, security in weak states, property right protections not otherwise available? No.

Thursday, November 13, 2014

Who is afraid of a little deflation?

Fears of "tipping" into deflation are overblown. I poke a little fun at sticky wages, Fed headroom, deflation-induced defaults and the long-predicted Keynesian deflationary spiral that never seems to happen, and the doom and gloom language from the ECB, IMF and other worriers who just happen to (of course) want to spend trillions to fix this latest "biggest economic problem."

One point that went by a little too quickly in the interest of space: Deflation can be a symptom of bad things. The issue is whether deflation is by itself a bad thing, and causes further damage.

Also, I should have been clearer on a big bottom line: we don't need huge "infrastructure" projects just to save us from deflation.

They ask me not to post the whole thing for 30 days, so those of you without WSJ access will just have to google or wait breathlessly.

Update: Ed Leamer wrote a great similar piece for Economists' Voice a while back "Deflation Dread Disorder; 'The CPI is Falling!'" In addition to a better title, he's got a cool Godzilla reference and picture.

Reason for big Government: The Firm

I enjoyed John Goodman's essay at Forbes.com, "Reason for big Government: The Firm"

California has a new law that requires all eggs sold in the state to come from chickens that are housed in roomier cages. Specifically, the hens “must be able to lie down, stand up and fully spread their wings.”

So how many Californians have been arrested for eating the wrong kind of egg? Zero. Not even one? Not one. Actually, the law doesn’t take effect until January, but even then egg eaters will have nothing to fear. The reason: the law doesn’t apply to people who eat eggs. It only applies to people who sell eggs.

Thursday, November 6, 2014

The Neo-Fisherian Question

On the "Neo-Fisherian" idea that maybe raising interest rates raises inflation,

Nick Rowe asks an important question. What about the impression, most recently in a host of countries that seemed to raise rates "too early" and then backed off, that raising interest rates lowers inflation? (And thanks to commenter Edward for the pointer.)

Partly in answer, and partly just in mulling it over, I think I can boil down the issue to this question:

If the central bank pegs the nominal rate at a fixed value, is the economy eventually stable, converging to the interest rate peg minus the real rate? Or is it unstable, careening off to hyperinflation or deflationary spiral?

Here are some possibilities to consider. At left is what we might call the pure neo-Fisherian view. Raise interest rates, and inflation will come.

Here are some possibilities to consider. At left is what we might call the pure neo-Fisherian view. Raise interest rates, and inflation will come.

I guess there is a super-pure view which would say that expected inflation rises right away. But that's not necessary. The plot in Monetary Policy with Interest on Reserves worked out a simple sticky price model. In that model, dynamics were pretty much as I have graphed to the left: real rates rise for the period of price stickiness, then inflation sets in.

Now, here is a possibility that I think might satisfy Neo-Fisherism, Nick, and a lot of people's intuition:

In response to the interest rate rise, indeed in the short run inflation declines. But if the central bank were to persist, and just leave the target alone, the economy really is stable, and eventually inflation would give up and return to the Fisher relation fold. (I was trying to get the model of "Interest on Reserves" to produce this result, but couldn't do it. Maybe fancier price stickiness, habits, adjustment costs...?)

This view would account for the Swedish and other experience.

We don't see the Fisher prediction because central banks never leave interest rates resolutely pegged. Instead, they pursue short-run pushing inflation around.

Partly in answer, and partly just in mulling it over, I think I can boil down the issue to this question:

If the central bank pegs the nominal rate at a fixed value, is the economy eventually stable, converging to the interest rate peg minus the real rate? Or is it unstable, careening off to hyperinflation or deflationary spiral?

I guess there is a super-pure view which would say that expected inflation rises right away. But that's not necessary. The plot in Monetary Policy with Interest on Reserves worked out a simple sticky price model. In that model, dynamics were pretty much as I have graphed to the left: real rates rise for the period of price stickiness, then inflation sets in.

Now, here is a possibility that I think might satisfy Neo-Fisherism, Nick, and a lot of people's intuition:

In response to the interest rate rise, indeed in the short run inflation declines. But if the central bank were to persist, and just leave the target alone, the economy really is stable, and eventually inflation would give up and return to the Fisher relation fold. (I was trying to get the model of "Interest on Reserves" to produce this result, but couldn't do it. Maybe fancier price stickiness, habits, adjustment costs...?)

This view would account for the Swedish and other experience.

We don't see the Fisher prediction because central banks never leave interest rates resolutely pegged. Instead, they pursue short-run pushing inflation around.

Tuesday, November 4, 2014

Across the Great Divide

There will be a webcast book event on Wed Nov 5, from the Hoover Institution's Washington D. C. offices, also available after the fact at that link.

My "Toward a Run-Free Financial System" is in it, in published form, also available on my webpage.

Larry Summers' Low Equilibrium Real Rates, Financial Crisis, and Secular Stagnation is an interesting read in his evolving case for "secular stagnation," which I'm sure will get a lot of attention.

But lots of the other papers are really interesting as well.

The rest of the table of contents:

Introduction

By Martin Neil Baily and John B. Taylor

Thursday, October 16, 2014

Monetary Policy with Interest On Reserves

Or, Heretics Part II

I just finished a big update of a working paper, "Monetary Policy with Interest on Reserves." It also sheds light on the question, what is the sign of monetary policy? (Previous posts here, here and here).

Again, the big issue is whether the "Fisherian" (Shall we call it "Neo-Fisherian?") possibility works. The Fisher equation says nominal interest rate = real interest rate plus expected inflation. So by raising nominal interest rates, maybe expected inflation rises?

The usual answer is "no, because prices are sticky." So, I worked out a very simple new-Keynesian sticky price model in which prices are set 4 periods in advance.

The top left panel of the graph shows the heretical result. I suppose the Fed raises interest rates by 1 percentage point for two periods, then brings interest rates back down (blue line). Prices are stuck for 4 periods (red line) so don't move. After 4 periods prices fully absorb the repressed inflation -- the Fisher equation works great, only waiting for prices to be able to move.

The top left panel of the graph shows the heretical result. I suppose the Fed raises interest rates by 1 percentage point for two periods, then brings interest rates back down (blue line). Prices are stuck for 4 periods (red line) so don't move. After 4 periods prices fully absorb the repressed inflation -- the Fisher equation works great, only waiting for prices to be able to move.

In the meantime the higher real interest rates (green) induce a little boom in consumption. So, raising rates not only raises inflation, it gives you a little output boost along the way! Raising rates forever does the same thing, but sets off a permanent inflation once price stickiness ends.

Why do conventional models give a different result?

I just finished a big update of a working paper, "Monetary Policy with Interest on Reserves." It also sheds light on the question, what is the sign of monetary policy? (Previous posts here, here and here).

Again, the big issue is whether the "Fisherian" (Shall we call it "Neo-Fisherian?") possibility works. The Fisher equation says nominal interest rate = real interest rate plus expected inflation. So by raising nominal interest rates, maybe expected inflation rises?

The usual answer is "no, because prices are sticky." So, I worked out a very simple new-Keynesian sticky price model in which prices are set 4 periods in advance.

In the meantime the higher real interest rates (green) induce a little boom in consumption. So, raising rates not only raises inflation, it gives you a little output boost along the way! Raising rates forever does the same thing, but sets off a permanent inflation once price stickiness ends.

Why do conventional models give a different result?

Heretics

Low inflation is back in the news. The Wall Street Journal covers the latest decline in European inflation. Peter Schiff has a nice article explaining that inflation is not such a great thing, unless of course you're a government that wants to pay back debt with cheap money. I dipped into this heresy in an earlier post, explaining that maybe zero rates and slight deflation just represent the arrival of Milton Friedman's optimal quantity of money.

But this news also brings to mind some thoughts on the second heresy -- maybe we have the sign wrong, and we're getting low inflation or deflation because interest rates are pegged at zero, and maybe the way to raise inflation (if you want to) is for the Fed to raise interest rates, and leave them there. (Earlier posts on this question here and here)

Back in 2010, Narayana Kocherlakota explained the basic idea

But this news also brings to mind some thoughts on the second heresy -- maybe we have the sign wrong, and we're getting low inflation or deflation because interest rates are pegged at zero, and maybe the way to raise inflation (if you want to) is for the Fed to raise interest rates, and leave them there. (Earlier posts on this question here and here)

Back in 2010, Narayana Kocherlakota explained the basic idea

Long-run monetary neutrality is an uncontroversial, simple, but nonetheless profound proposition. In particular, it implies that if the FOMC maintains the fed funds rate at its current level of 0-25 basis points for too long, both anticipated and actual inflation have to become negative. Why? It’s simple arithmetic. Let’s say that the real rate of return on safe investments is 1 percent and we need to add an amount of anticipated inflation that will result in a fed funds rate of 0.25 percent. The only way to get that is to add a negative number—in this case, –0.75 percent.

To sum up, over the long run, a low fed funds rate must lead to consistent, but low, levels of deflation.”It's really simple. One of the most fundamental relations in economics is the Fisher equation, nominal interest rate = real interest rate plus expected inflation. Real interest rates can be affected by monetary policy in the short run. But not forever. So if the Fed raises the nominal interest rate and leaves it there, expected inflation should eventually rise to meed that nominal rate.

Monday, October 6, 2014

Chicken and Egg Inequality

The FT's Martin Wolf weighs in on "Why inequality is such a drag on economies"

This is the question that was bugging me last week. Why is inequality a problem in and of itself, rather representing a symptom of problems that should be fixed for their own sake?

Since last week's review of these ideas was rather scathing, I hoped Wolf would offer some new, and better tested ideas.

Alas, and interestingly, no.

This is the question that was bugging me last week. Why is inequality a problem in and of itself, rather representing a symptom of problems that should be fixed for their own sake?

Since last week's review of these ideas was rather scathing, I hoped Wolf would offer some new, and better tested ideas.

Alas, and interestingly, no.

Wednesday, October 1, 2014

Envy and excess

In the inequality post, I puzzled over the following conundrum:

There is a view motivating the left that inequality is just unjust so we - the federal government is always "we" -- have to stop it. If they'd say that, fine, we could have productive discussion.

But they say, and I was going after in the post, all sorts of other things. That inequality will cause poor people to spend too much, that it will cause them to rise in political rebellion, for example. For that to happen, for the presence of the rich to affect their behavior in any way, they have to know about how the exploding 1/10 of 1% live, and how many of them there are. Which just doesn't make any sense.

Paul Krugman had a few revealing columns over the weekend. (No, not the endlessly repeated Say's Law calumny. I trust you all understand how empty that is.)

Why does it matter at all to a vegetable picker in Fresno, or an unemployed teenager on the south side of Chicago, whether 10 or 100 hedge fund managers in Greenwich have private jets? How do they even know how many hedge fund managers fly private? They have hard lives, and a lot of problems. But just what problem does top 1% inequality really represent to them?I emphasized the quantity issue here. His grandfather in the 1930s watched movies and saw glamorous lifestyles way beyond what he could achieve. Increasing inequality is about larger numbers who live a lavish lifestyle. And the claim is that increasing inequality is changing behavior.

There is a view motivating the left that inequality is just unjust so we - the federal government is always "we" -- have to stop it. If they'd say that, fine, we could have productive discussion.

But they say, and I was going after in the post, all sorts of other things. That inequality will cause poor people to spend too much, that it will cause them to rise in political rebellion, for example. For that to happen, for the presence of the rich to affect their behavior in any way, they have to know about how the exploding 1/10 of 1% live, and how many of them there are. Which just doesn't make any sense.

Paul Krugman had a few revealing columns over the weekend. (No, not the endlessly repeated Say's Law calumny. I trust you all understand how empty that is.)

Returns to unwanted education

In my inequality post, I wrote, somewhat speculatively,

The returns to education chosen and worked hard for are not necessarily replicated in education subsidized or forced.Marginal Revolution points to a nice new paper by Pierre Mouganie making this point. From the abstract:

In 1997, the French government put into effect a law that permanently exempted young French male citizens born after Jan 1, 1979 from mandatory military service while still requiring those born before that cutoff date to serve. ... conscription eligibility induces a significant increase in years of education, which is consistent with conscription avoidance behavior. However, this increased education does not result in either an increase in graduation rates, or in employment and wages. Additional evidence shows conscription has no direct effect on earnings, suggesting that the returns to education induced by this policy was zero.

Monday, September 29, 2014

Why and how we care about inequality

Note: These are remarks I gave in a concluding panel at the Conference on Inequality in Memory of Gary Becker, Hoover Institution, September 26 2014. The conference program here, and John Taylor's summary here, where you can see the great papers I allude to. I'll probably rework this to a more general essay, so I reserve the right to recycle some points later.

Why and How We Care About Inequality

Wrapping up a wonderful conference about facts, our panel is supposed to talk about “solutions” to the “problem” of inequality.

We have before us one “solution,” the demand from the left for confiscatory income and wealth taxation, and a substantial enlargement of the control of economic activity by the State.

Note I don’t say “redistribution” though some academics dream about it. We all know there isn’t enough money, especially to address real global poverty, and the sad fact is that government checks don’t cure poverty. President Obama was refreshingly clear, calling for confiscatory taxation even if it raised no income. “Off with their heads” solves inequality, in a French-Revolution sort of way, and not by using the hair to make wigs for the poor. The agenda includes a big expansion of spending on government programs, minimum wages, “living wages,” government control of wages, especially by minutely divided groups, CEO pay regulation, unions, “regulation” of banks, central direction of all finance, and so on. The logic is inescapable. To “solve inequality,” don’t just take money from the rich. Stop people, and especially the “wrong” people, from getting rich in the first place.

In this context, I think it is a mistake to accept the premise that inequality, per se, is a “problem” needing to be “solved,” and to craft “alternative solutions.”

Just why is inequality, per se, a problem?

Suppose a sack of money blows in the room. Some of you get $100, some get $10. Are we collectively better off? If you think “inequality” is a problem, no. We should decline the gift. We should, in fact, take something from people who got nothing, to keep the lucky ones from their $100. This is a hard case to make.

One sensible response is to acknowledge that inequality, by itself, is not a problem. Inequality is a symptom of other problems. I think this is exactly the constructive tone that this conference has taken.

But there are lots of different kinds of inequality, and an enormous variety of different mechanisms at work. Lumping them all together, and attacking the symptom, “inequality,” without attacking the problems is a mistake. It’s like saying “fever is a problem. So medicine shall consist of reducing fevers.”

Why and How We Care About Inequality

Wrapping up a wonderful conference about facts, our panel is supposed to talk about “solutions” to the “problem” of inequality.

We have before us one “solution,” the demand from the left for confiscatory income and wealth taxation, and a substantial enlargement of the control of economic activity by the State.

Note I don’t say “redistribution” though some academics dream about it. We all know there isn’t enough money, especially to address real global poverty, and the sad fact is that government checks don’t cure poverty. President Obama was refreshingly clear, calling for confiscatory taxation even if it raised no income. “Off with their heads” solves inequality, in a French-Revolution sort of way, and not by using the hair to make wigs for the poor. The agenda includes a big expansion of spending on government programs, minimum wages, “living wages,” government control of wages, especially by minutely divided groups, CEO pay regulation, unions, “regulation” of banks, central direction of all finance, and so on. The logic is inescapable. To “solve inequality,” don’t just take money from the rich. Stop people, and especially the “wrong” people, from getting rich in the first place.

In this context, I think it is a mistake to accept the premise that inequality, per se, is a “problem” needing to be “solved,” and to craft “alternative solutions.”

Just why is inequality, per se, a problem?

Suppose a sack of money blows in the room. Some of you get $100, some get $10. Are we collectively better off? If you think “inequality” is a problem, no. We should decline the gift. We should, in fact, take something from people who got nothing, to keep the lucky ones from their $100. This is a hard case to make.

One sensible response is to acknowledge that inequality, by itself, is not a problem. Inequality is a symptom of other problems. I think this is exactly the constructive tone that this conference has taken.

But there are lots of different kinds of inequality, and an enormous variety of different mechanisms at work. Lumping them all together, and attacking the symptom, “inequality,” without attacking the problems is a mistake. It’s like saying “fever is a problem. So medicine shall consist of reducing fevers.”

Monday, September 22, 2014

A few things the Fed has done right -- the oped

Now that 30 days have passed, I can post the whole oped from the Wall Street Journal. See previous post for additional commentary

A Few Things the Fed Has Done Right

The Fed's plan to maintain a large balance sheet and pay interest on bank reserves is good for financial stability.

As Federal Reserve officials lay the groundwork for raising interest rates, they are doing a few things right. They need a little cheering, and a bit more courage of their convictions.

The Fed now has a huge balance sheet. It owns about $4 trillion of Treasury bonds and mortgage-backed securities. It owes about $2.7 trillion of reserves (accounts banks have at the Fed), and $1.3 trillion of currency. When it is time to raise interest rates, the Fed will simply raise the interest it pays on reserves. It does not need to soak up those trillions of dollars of reserves by selling trillions of dollars of assets.

The Fed's plan to maintain a large balance sheet and pay interest on bank reserves, begun under former Chairman Ben Bernanke and continued under current Chair Janet Yellen, is highly desirable for a number of reasons—the most important of which is financial stability. Short version: Banks holding lots of reserves don't go under.

This policy is new and controversial. However, many arguments against it are based on fallacies.

A Few Things the Fed Has Done Right

The Fed's plan to maintain a large balance sheet and pay interest on bank reserves is good for financial stability.

As Federal Reserve officials lay the groundwork for raising interest rates, they are doing a few things right. They need a little cheering, and a bit more courage of their convictions.

The Fed now has a huge balance sheet. It owns about $4 trillion of Treasury bonds and mortgage-backed securities. It owes about $2.7 trillion of reserves (accounts banks have at the Fed), and $1.3 trillion of currency. When it is time to raise interest rates, the Fed will simply raise the interest it pays on reserves. It does not need to soak up those trillions of dollars of reserves by selling trillions of dollars of assets.

The Fed's plan to maintain a large balance sheet and pay interest on bank reserves, begun under former Chairman Ben Bernanke and continued under current Chair Janet Yellen, is highly desirable for a number of reasons—the most important of which is financial stability. Short version: Banks holding lots of reserves don't go under.

This policy is new and controversial. However, many arguments against it are based on fallacies.

Saturday, September 20, 2014

Yellen on the poverty of the poor.

I ran across this interesting speech by Fed Chair Janet Yellen, "The importance of asset building for low and middle income households."

This all brings to mind several thoughts.

The median net worth reported by the bottom fifth of households by income was only $6,400 in 2013. Among this group, representing about 25 million American households, many families had no wealth or had negative net worth. The next fifth of households by income had median net worth of just $27,900.But even these numbers are in a sense overstated, since much of the "net worth" is in home equity, thus not easily available

Home equity accounts for the lion's share of wealth... for lower and middle income families, financial assets, including 401 (k) plans and pensions, are still a very small share of their assets.This matters because,

for many lower-income families without assets, the definition of a financial crisis is a month or two without a paycheck, or the advent of a sudden illness or some other unexpected expense. .... According to the Board's recent Survey of Household Economics and Decisionmaking, an unexpected expense of just $400 would prompt the majority [!] of households to borrow money, sell something, or simply not pay at all.["Majority" meaning 51% of all households seems like a lot, if the bottom 2/5 has $27,500. But I didn't look it up.]

This all brings to mind several thoughts.

Friday, September 19, 2014

Capital Language

Sometimes the press deserves a little applause. Peter Coy at Business Week and Pat Regnier at Time both wrote articles very nicely explaining bank capital and many fallacies around it.

Both articles also have nice graphics, but I give Coy and BusinessWeek the A+, because it also explains that banks can build capital without cutting lending.

A few select quotes. From Coy at Business Week, two fallacies skewered:

HT to Anat Admati who sent me the links.

Both articles also have nice graphics, but I give Coy and BusinessWeek the A+, because it also explains that banks can build capital without cutting lending.

A few select quotes. From Coy at Business Week, two fallacies skewered:

So what exactly is capital? Sometimes it’s described as a rainy-day fund, which is wrong. More often it’s characterized as something banks “hold,” which can make it sound like a pile of money that has to be set aside so it can’t be lent out for a profit. That’s not right either.

The American Bankers Association says that higher capital requirements for big banks “reduce economic and job growth.” But banks can meet capital requirements without cutting back lending. They just have to sell more shares (cutting down on buybacks also works) or reduce cash-draining dividends (refraining from raising them also helps).Regnier at Time too, and passes on the useful housing analogy.

...As Admati frequently points out, banks have benefited from the misconception that higher capital requirements means banks would have to keep 20% or 30% of their money locked up in a vault, instead of lending it out to businesses or homeowners.

In fact, making banks “hold more capital” actually means they have to borrow less. In their book, Admati and Hellwig show that this is almost exactly like a homeowner making sure to build up equity in her house.

To raise more capital, banks wouldn’t hold back lending. Rather, they’d tap their shareholders, either by issuing new stock or just by cutting the dividends they pay out of earnings, letting profits build up on the balance sheet.It's refreshing when professional writers explain things a lot more clearly and succinctly than us academics seem to do, and get the economics spot on. Yes, words, stories, and ideas do matter, and the change in attitude about bank capital is a great example.

HT to Anat Admati who sent me the links.

Thursday, September 18, 2014

The case for open borders

Alex Tabarrok has a splendid post "the case for open borders" on Marginal Revolution.

Along the way he points to "Economics and Immigration: Trillion Dollar Bills on the Sidewalk?" by Michael Clemens and forthcoming Journal of Economic Perspectives, "The Domestic Economic Impacts of Immigration" by David Roodman and "The case for Open Borders" by Dylan Matthews, a Bryan Caplan interview and story on vox. All are worth reading.

1) Women

1) Women

Anecdotes and analogies are important for how we understand events, beyond equations and tables. Bryan makes this point, with a lovely "elevator pitch" metaphor. Bryan comes up with a good story as well, that I hadn't thought of:

How much has the entry of women to the labor force lowered men's jobs and wages? (I was tempted to write "access to jobs," but someone might take it seriously!) Should the US government have prohibited women from entering the labor force, in order to shore up the wages of men?

The increase in women's labor force participation was huge -- from 32% to 60%, resulting in an increase in overall labor force participation from 59% to 67% of the population from 1960 to 2000. 8% of 320 million is 26 million, so we're talking about a lot of extra people working.

The answer to the first question is surely yes, but not a lot. 26 million men did not lose their jobs so women could work. And the answer to the second question is surely no.

Along the way he points to "Economics and Immigration: Trillion Dollar Bills on the Sidewalk?" by Michael Clemens and forthcoming Journal of Economic Perspectives, "The Domestic Economic Impacts of Immigration" by David Roodman and "The case for Open Borders" by Dylan Matthews, a Bryan Caplan interview and story on vox. All are worth reading.

Anecdotes and analogies are important for how we understand events, beyond equations and tables. Bryan makes this point, with a lovely "elevator pitch" metaphor. Bryan comes up with a good story as well, that I hadn't thought of:

How much has the entry of women to the labor force lowered men's jobs and wages? (I was tempted to write "access to jobs," but someone might take it seriously!) Should the US government have prohibited women from entering the labor force, in order to shore up the wages of men?