Suppose that an investor you admire and trust comes to you with an investment idea. “This is a good one,” he says enthusiastically. “I’m in it, and I think you should be, too.”MBA final exam question: Explain the mistake in this paragraph.

Would your reply possibly be this? “Well, it all depends on what my tax rate will be on the gain you’re saying we’re going to make. If the taxes are too high, I would rather leave the money in my savings account, earning a quarter of 1 percent.” Only in Grover Norquist’s imagination does such a response exist.

Friday, November 30, 2012

Buffett Math

Warren Buffett, New York Times on November 25th 2012:

Thursday, November 29, 2012

Truth stranger than fiction?

From the New York Times. I checked, it really is not from the Onion.

WASHINGTON — House Republicans said on Thursday that Treasury Secretary Timothy F. Geithner presented the House speaker, John A. Boehner, a detailed proposal to avert the year-end fiscal crisis with $1.6 trillion in tax increases over 10 years, an immediate new round of stimulus spending, home mortgage refinancing and a permanent end to Congressional control over statutory borrowing limits.Meanwhile, Costco is in the news, for borrowing $3 billion dollars, and paying it out as a special dividend before dividend taxes rise. Stock rose 6%. Tax arbitrage is so cool.

...In exchange for locking in the $1.6 trillion in added revenues, President Obama embraced $400 billion in savings from Medicare and other entitlements, to be worked out next year, with no guarantees.

The upfront tax increases in the proposal go beyond what Senate Democrats were able to pass earlier this year. Tax rates would go up for higher-income earners, as in the Senate bill, but Mr. Obama wants their dividends to be taxed as ordinary income, something the Senate did not approve. He also wants the estate tax to be levied at 45 percent on inheritances over $3.5 million, a step several Democratic senators balked at. The Senate bill made no changes to the estate tax, which currently taxes inheritances over $5 million at 35 percent.

Wednesday, November 28, 2012

Experimental evidence on the effect of taxes

Much of our "fiscal cliff" debate revolves around the incentive effects of raising marginal taxes on high incomes. High tax advocates used to say that taxes won't hurt growth that much, and advocated them for other reasons. Now they are advocating that even a 91% federal income tax rate, on top of state, sales, etc, as we had in the 1950s, (not counting all the loopholes!) will actually be good for the economy and also raise lots of revenue.

This seems to me like magical thinking, and a great testament to how people can persuade themselves of anything if it suits the partisan passion of the moment. But wouldn't it be nice if someone would run an experiment for us?

Fortunately, Europe has been running a very useful set of experiments on what happens if you address yawning deficits with high income, wealth and property taxes. Which brings me to a report from the Telegraph

This seems to me like magical thinking, and a great testament to how people can persuade themselves of anything if it suits the partisan passion of the moment. But wouldn't it be nice if someone would run an experiment for us?

Fortunately, Europe has been running a very useful set of experiments on what happens if you address yawning deficits with high income, wealth and property taxes. Which brings me to a report from the Telegraph

Almost two-thirds of the country’s million-pound earners disappeared from Britain after the introduction of the 50p (percent) top rate of tax, figures have disclosed.

Sunday, November 25, 2012

Taxes and cliffs

(Update: John Batchelor show radio interview on this blog post)

The whole tax debate is supremely frustrating to anyone who survived econ 1.

The ill effects of taxation -- the "distortions" -- depend on the total, marginal rate including transfers. If I earn an extra dollar, how much more stuff do I get, or how much more of someone else's services can I receive? That calculation has to include all taxes, federal, payroll, state, local, sales, excise, etc. and phaseouts.

And, if you receive a benefit from the government that phases out with income, so every dollar of income above (say) $30,000 reduces your benefit by 50 cents, then you face a 50 percent marginal tax rate even if you pay no "taxes" at all. Taxes and benefits -- both in level and on the margin -- need to be considered together.

I've been looking for good calculations of marginal rates. The CBO has just issued a nice report titled "Effective Marginal Tax Rates for Low- and Moderate-Income Workers" that begins (begins!) to shed some light on the right question. Here's one important graph, titled "Marginal Tax Rates for a Hypothetical Single Parent with One Child, by Earnings, in 2012";

Friday, November 23, 2012

Tuesday, November 20, 2012

Health economics update

Russ Roberts did a podcast with me in his "EconTalk" series, on my "After the ACA'' article. Russ also put together a really nice list of readings with the podcast, at the same link.

I also found this very informative editorial "What the world doesn't know about health care in America" by Scott Atlas. It goes a good way to answering the persistent "What about how great health care is in Europe" comments. Some choice quotes:

I also found this very informative editorial "What the world doesn't know about health care in America" by Scott Atlas. It goes a good way to answering the persistent "What about how great health care is in Europe" comments. Some choice quotes:

Affirming 2005’s Chaoulli v. Quebec, in which [Canadian] Supreme Court justices famously concluded “access to a waiting list is not access to health care,” [my emphasis] countless studies document grave consequences from prolonged waits...I love this little quote, because the deliberate confusion of "insurance" with "access" has long bugged me about the US debate.

Friday, November 16, 2012

Debt Maturity

Another essay, a bit shorter this time, on maturity structure of US debt. I was asked to give comments on a paper by Robin Greenwood, Sam Hanson, and Jeremy Stein *

at a conference at the Treasury. It's a really nice paper, and (unusually) I didn't have much incisive to say about it, except to say it didn't go far enough. And, I only had 10 minutes. So I gave a speech instead. (The pdf version on my webpage may be better reading, and will be updated if I ever do anything with this.)

Having your cake and eating it too: The maturity structure of US debt

John H. Cochrane 1

November 15 2012

Robin Greenwood, Sam Hanson, and Jeremy Stein 2 nicely model two important considerations for the maturity structure of government debt: Long–term debt insulates government finances from interest-rate increases. Short-term debt is highly valued as a “liquid” asset, providing many “money-like” services, and potentially displacing run-prone financial intermediaries as suppliers of “liquidity.” Long-term debt also provides some liquidity and collateral services, (Krishnamurthy and Vissing-Jorgensen3 (2012)) but not as effectively as short-term debt. How do we think about this tradeoff?

Posing the question this way is already a pretty radical departure. The maturity structure of U.S. debt is traditionally perceived as a relatively technical job, to finance a given deficit stream at lowest long-run cost, as Colin Kim eloquently explained in the panel. Greenwood, Hanson and Stein, along with the other papers at this conference, are asking the Treasury’s Office of Debt Management to consider large economic issues far beyond this traditional question. For example, saying the Treasury should provide liquid debt because it helps the financial system and can substitute for banking regulation, whether or not that saves the Treasury money, asks the Treasury to think about its operations a lot more as the Fed does. Well, times have changed; the maturity structure of US debt does have important broader implications. And getting it right or wrong could make a huge difference in the difficult times ahead.

Go Long!

As I think about the choice between long and short term debt, I feel like screaming4 “Go Long. Now!” Bond markets are offering the US an incredible deal. The 30 year Treasury rate as I write is 2.77%. The government can lock in a nominal rate of 2.77% for the next 30 years, and even that can be paid back in inflated dollars! (Comments at the conference suggested that term structure models impute a negative risk premium to these low rates: They are below expected future short rates, so markets are paying us for the privilege of writing interest-rate insurance!)

Having your cake and eating it too: The maturity structure of US debt

John H. Cochrane 1

November 15 2012

Robin Greenwood, Sam Hanson, and Jeremy Stein 2 nicely model two important considerations for the maturity structure of government debt: Long–term debt insulates government finances from interest-rate increases. Short-term debt is highly valued as a “liquid” asset, providing many “money-like” services, and potentially displacing run-prone financial intermediaries as suppliers of “liquidity.” Long-term debt also provides some liquidity and collateral services, (Krishnamurthy and Vissing-Jorgensen3 (2012)) but not as effectively as short-term debt. How do we think about this tradeoff?

Posing the question this way is already a pretty radical departure. The maturity structure of U.S. debt is traditionally perceived as a relatively technical job, to finance a given deficit stream at lowest long-run cost, as Colin Kim eloquently explained in the panel. Greenwood, Hanson and Stein, along with the other papers at this conference, are asking the Treasury’s Office of Debt Management to consider large economic issues far beyond this traditional question. For example, saying the Treasury should provide liquid debt because it helps the financial system and can substitute for banking regulation, whether or not that saves the Treasury money, asks the Treasury to think about its operations a lot more as the Fed does. Well, times have changed; the maturity structure of US debt does have important broader implications. And getting it right or wrong could make a huge difference in the difficult times ahead.

Go Long!

As I think about the choice between long and short term debt, I feel like screaming4 “Go Long. Now!” Bond markets are offering the US an incredible deal. The 30 year Treasury rate as I write is 2.77%. The government can lock in a nominal rate of 2.77% for the next 30 years, and even that can be paid back in inflated dollars! (Comments at the conference suggested that term structure models impute a negative risk premium to these low rates: They are below expected future short rates, so markets are paying us for the privilege of writing interest-rate insurance!)

Tuesday, November 13, 2012

Bloomberg TV interview

A short interview with Bloomberg TV's Betty Liu on the fiscal cliff. No big news for readers of this blog, but maybe fun anyway.

We were just getting going when it ended. I was ready to say, if you didn't buy stimulus from spending increases, you shouldn't fear lack of stimulus from spending reductions; all government (federal, state, local) and all taxes matter; you need to include taxes and benefits, and then see the huge marginal taxes faced by poor people, and how cutting subsidies that go to rich people counts in the distributional calculus;the growth of regulation and tax chaos matters more than tax rates, Europe just showed us what happens when you try to balance the budget with sharp hikes in marginal rates....Next time.

We were just getting going when it ended. I was ready to say, if you didn't buy stimulus from spending increases, you shouldn't fear lack of stimulus from spending reductions; all government (federal, state, local) and all taxes matter; you need to include taxes and benefits, and then see the huge marginal taxes faced by poor people, and how cutting subsidies that go to rich people counts in the distributional calculus;the growth of regulation and tax chaos matters more than tax rates, Europe just showed us what happens when you try to balance the budget with sharp hikes in marginal rates....Next time.

Monday, November 12, 2012

Gas price contest

As all of you know, New York and New Jersey are having huge gas lines in the wake (still) of hurricane Sandy. Both are enforcing laws against "gouging," and New Jersey's attorney general, apparently having time on his hands, is going after people who listed gas for resale on Craigslist.

Let's start a little comments essay contest. If New York and New Jersey let people charge whatever they wanted for gas, and prices went up to $25 per gallon then...

Here are some ideas to get you started

Let's start a little comments essay contest. If New York and New Jersey let people charge whatever they wanted for gas, and prices went up to $25 per gallon then...

Here are some ideas to get you started

Diversity in academia

99 percent of donors from Princeton gave to Obama, reports the Daily Princetonian, 157 to 2. Princeton's one-percenters are a visiting lecturer and a custodian.

As a colleague pointed out, it may be little wonder that Republican politicians distrust academic "studies," whether about the effects of taxes on growth or carbon on the climate.

As a colleague pointed out, it may be little wonder that Republican politicians distrust academic "studies," whether about the effects of taxes on growth or carbon on the climate.

Saturday, November 10, 2012

Dodd-Frank and Stigler's Ghost

The New York Times finally published Gretchen Morgenson's article, pointing out that Dodd-Frank enshrines rather than eliminates "too big to fail," though systemic "designation" of "financial utilities" such as the exchanges has been underway since the bill's beginning. Needless to say, this has been my opinion all along.

Today let's move on. I'll label the bigger problem, "too big to fail means too big to compete." TBTF=TBTC. There, we can put that on bumper stickers.

As the Ms. Morgenson figured out, the Chicago Mercantile Exchange is now too big to fail, and will be able to borrow from the Fed and get a bailout. But that's not the big issue. The CME is now too big to compete. Who can now start a new exchange, maybe offering more protection against high frequency traders or other conveniences to customers, and threatening the CME's customer base? Not against a protected "financial utility."

George Stigler taught us that regulators are prone to "capture." Over the years, regulators start to sympathize with the industry they're regulating. Next thing you know, the regulations end up being used to protect the industry from competition. Luigi Zingales' great new book calls it "crony capitalism," emphasizing that it, not too much benevolent government or too much ufettered market competition, is the main characteristic of our society.

Today let's move on. I'll label the bigger problem, "too big to fail means too big to compete." TBTF=TBTC. There, we can put that on bumper stickers.

As the Ms. Morgenson figured out, the Chicago Mercantile Exchange is now too big to fail, and will be able to borrow from the Fed and get a bailout. But that's not the big issue. The CME is now too big to compete. Who can now start a new exchange, maybe offering more protection against high frequency traders or other conveniences to customers, and threatening the CME's customer base? Not against a protected "financial utility."

George Stigler taught us that regulators are prone to "capture." Over the years, regulators start to sympathize with the industry they're regulating. Next thing you know, the regulations end up being used to protect the industry from competition. Luigi Zingales' great new book calls it "crony capitalism," emphasizing that it, not too much benevolent government or too much ufettered market competition, is the main characteristic of our society.

Wednesday, November 7, 2012

Predictions

I did a short spot on NPR's Marketplace this morning (also here). The announced topic was what I thought would happen to economic policy after the election. Jeff Horwich, the interviewer wanted to stitch together a story about everyone is going to get together and play nice now, which seemed like a fairly pointless line to pursue. What "I would do" is now off the table, and I didn't think it worth arguing with Jared Bernstein's repetition of Obama campaign nostrums.

But it gave me a chance to put some thoughts together. I usually don't predict anything, because I (like everyone else) am usually wrong. But I'll make an exception today

Forecast in three parts: The sound and fury will be over big fights on taxes and spending. They will look like replays of the last four years and not end up accomplishing much. The big changes to our economy will be the metastatic expansion of regulation, let by ACA, Dodd-Frank, and EPA. There will be no change on our long run problems: entitlements, deficits or fundamental reform of our chaotic tax system. 4 more years, $4 trillion more debt.

But it gave me a chance to put some thoughts together. I usually don't predict anything, because I (like everyone else) am usually wrong. But I'll make an exception today

Forecast in three parts: The sound and fury will be over big fights on taxes and spending. They will look like replays of the last four years and not end up accomplishing much. The big changes to our economy will be the metastatic expansion of regulation, let by ACA, Dodd-Frank, and EPA. There will be no change on our long run problems: entitlements, deficits or fundamental reform of our chaotic tax system. 4 more years, $4 trillion more debt.

Monday, November 5, 2012

DeMuth on Obamacare

Christopher DeMuth has a nice Oped in the Wall Street Journal. Thesis: Obamacare is the big question for the election.

He makes two points that I haven't seen expressed this well before, including by me despite 25 pages of trying:

He makes two points that I haven't seen expressed this well before, including by me despite 25 pages of trying:

Sunday, November 4, 2012

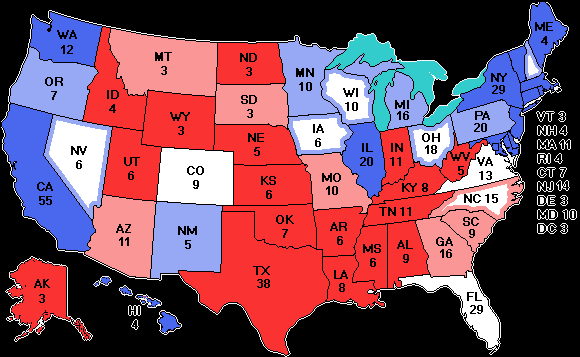

Why the electoral college is a great idea

Here's why I think the electoral college -- with (crucially) winner-take-all selection in the states, which is under attack -- is a great idea. (Even though I live in Illinois.) Look at the map. (Source here, I found it just by google searching, so no endorsement.)

With the electoral college, Governor Romney and President Obama have to get 51% majorities in enough states to get 270 votes, to win the white house.

Suppose we had a popular vote instead. Now, instead of fighting for 51% of Ohio, President Obama could instead try to raise his 60% of New York and Illinois to 70%, even if it meant 45% of Ohio. Or he could try to raise his 80% of New York city and Chicago to 90%, (made up number). He doesn't need to persuade people, really, he just needs to encourage more New Yorkers and Chicagoans to turn out.

Thursday, November 1, 2012

Debate with Goolsbee

Last Tuesday, Glen Weyl asked me to debate economic policy issues in the current election with Austan Goolsbee, in the famous "rational choice" workshop. Here's my 10-minute opening statement. Austan did a great job in a tough audience.

Economic Policy and the Election:

Growth is our number one economic challenge. Here’s how recoveries are supposed to look. We get a period of very strong growth rates, until the economy recovers to “trend,” or potential.”

Here we are. Not only have we failed to bounce back, growth is slowing down. We seem headed for a permanent loss of about 8% and sclerotic 1-2% growth.

Here we are. Not only have we failed to bounce back, growth is slowing down. We seem headed for a permanent loss of about 8% and sclerotic 1-2% growth.

Economic Policy and the Election:

Growth is our number one economic challenge. Here’s how recoveries are supposed to look. We get a period of very strong growth rates, until the economy recovers to “trend,” or potential.”

{kind=link}

Subscribe to:

Posts (Atom)