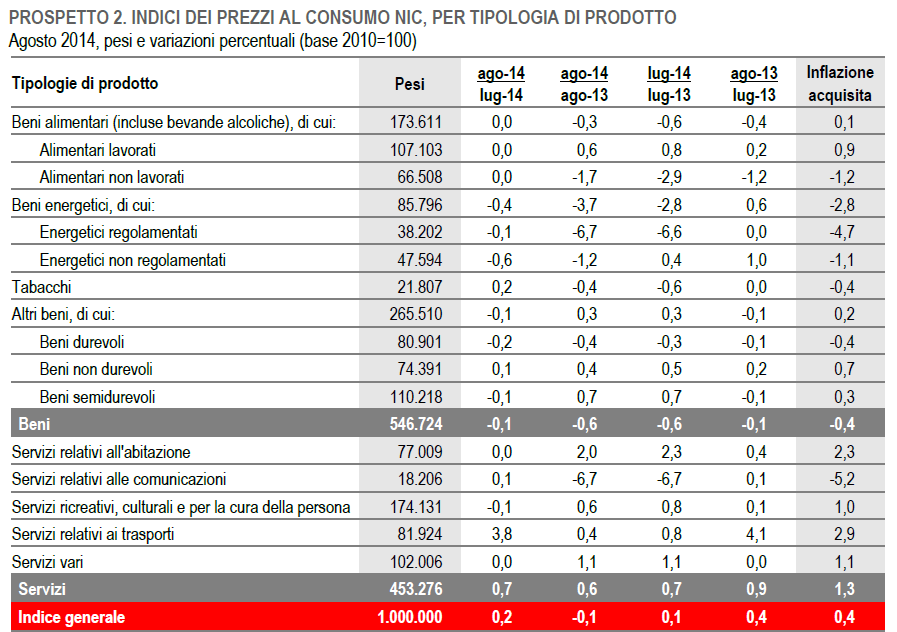

The right hand column gives inflation by category. "Beni Alimentari" are food, +0.1%, "Beni Energetici" is energy, -2.8%. "Beni Durevoli" is durable goods, -0.4% and "nondurevoli", duh, nondurable goods at +0.7%. The services are all positive, except communications services

The message, suggests Giulio, is pretty clear. What's going down? Tradeables and commodities. Oil prices and agricultural commodity prices reflect global, not Italian, supply and demand. Imported and import-competing durable prices go down. What's going up? Nontradeables and services. This looks like imported and supply deflation not lack-of-demand deflation

The subdivision goods / services is in fact for a country like Italy a good approximation of subdivision tradables ( tradables ) / non-tradable goods ( nontradables ). ... If deflation Italian was mainly due to the weakness of domestic demand, then we should observe deflation even (and especially) in the prices of services. Instead do not observe the contrary, we observe an increase of 0.6%.And prices go down when supply curves shift out,

note the strong (6.7%) reduction in the price of communications services, a reduction that is the clearest example of deflation induced by technological innovation and, probably, competition... in a rapidly expanding and highly contestable market. [Yes, even in Italy] Multiplying this price reduction by its weight in the Istat basket, (6.7% * 1.82%), it turns out this item contributes 0.12%, a bit more than the whole of deflation.The longer original is worth reading.

I guess the 16 euro gelato will still be with us for a while.

Mr. Cochrane, thanks for your post. The constant flow of "comments" on "the danger of deflation" is so disapointing, commentators and some academics seem to have forgotten that prices can go down on supply shocks, and that is good for consumers.

ReplyDeleteWhile it might be true, that deflation in italy is currently driven by supply factors, it cannot be denied that those growth factors are still much weaker now than they were until 2008. And at this time, inflation was higher than today.

ReplyDeleteSo I still think that italy's problems are mainly a demand side story, because what really counts for aggregate demand to be too weak is the deviation of total spending (per capita?) from trend. And the fact that italy now faces deflation supported by supply side factors doesn't change anything for the claim that the problem is too tight monetary policy that lets total spending deviate too much from trend.

Having said that, I agree that the media/pundits should stop talking about the problem being deflation (which *can* be harmless if not emerging as a sudden deviation from trend), but talking about deviations of total spending instead.

I am glad to learn that we are at the vanguard of tecnological innovation (and tech induced deflation), unlike for instance those Brits that have been clocking 4% inflation rates in the last few years which some people connected to this new tech thing called QE which in Italy is not licensed. Since 2008 British industrial production is back and ours is down by -27%, worse than in the 30's, our retail sales are down -9% since 2008 and in the UK are slightly up. They had deficits of 10% of GDP and we stayed at 3%. Here taxes have been raised by 70 billions in the last 3-4 years to reassure that we will pay our 85 billions euros of interest on BTP for ever. Even though Italian banks had aggregate losses below 30 billions in 2008-2009 and UK banks north of 300 billions, bringing taxes up to 48% of GDP (even allowing for a 17% black economy addition to it) collapsed sales, production and income. As a conseguence banks contracted credit of someghing around 100 billions. So, in a 1,550 billions economy (2008) we took away around 70 billions through taxes (austerity) and 100 billions of less lending from banks. And our 45 billions a year deficits go almost all to pay interest to foreign investors (yes, they are down from 45% to 30% of our gov debt, but they own the 10 years, not the one year bonds..).

ReplyDeleteBut no, money has little to do with it, because we barter here, we produce first and then exchange what we can get and this allows us to consume. No money is really involved, only being less efficient than Germans matters (something that happened in the last 10 years, since from 1950 to 1990 we grew faster...)

Do you have a model that shows what happens to a 1550 billions economy that increases taxes by 70 billions, keeps a primary surplus of 20-30 billions a year, uses its 3% deficit to pay interest abroad and contracts credit by 100 billions (? the latter due mostly to a speculative attack on its bonds because of fears of Berlusconi wanting out of the euro) ? "Ceteris paribus", without anything else happening, just those little money issues...

I am glad to learn that we are at the vanguard of tecnological innovation (and tech induced deflation), unlike for instance those Brits that have been clocking 4% inflation rates in the last few years which some people connected to this new tech thing called QE which in Italy is not licensed. Since 2008 British industrial production is back and ours is down by -27%, worse than in the 30's, our retail sales are down -9% since 2008 and in the UK are slightly up. They had deficits of 10% of GDP and we stayed at 3%. Here taxes have been raised by 70 billions in the last 3-4 years to reassure that we will pay our 85 billions euros of interest on BTP for ever. Even though Italian banks had aggregate losses below 30 billions in 2008-2009 and UK banks north of 300 billions, bringing taxes up to 48% of GDP (even allowing for a 17% black economy addition to it) collapsed sales, production and income. As a conseguence banks contracted credit of someghing around 100 billions. So, in a 1,550 billions economy (2008) we took away around 70 billions through taxes (austerity) and 100 billions of less lending from banks. And our 45 billions a year deficits go almost all to pay interest to foreign investors (yes, they are down from 45% to 30% of our gov debt, but they own the 10 years, not the one year bonds..).

ReplyDeleteBut no, money has little to do with it, because we barter here, we produce first and then exchange what we can get and this allows us to consume. No money is really involved, only being less efficient than Germans matters (something that happened in the last 10 years, since from 1950 to 1990 we grew faster...)

Do you have a model that shows what happens to a 1550 billions economy that increases taxes by 70 billions, keeps a primary surplus of 20-30 billions a year, uses its 3% deficit to pay interest abroad and contracts credit by 100 billions (? the latter due mostly to a speculative attack on its bonds because of fears of Berlusconi wanting out of the euro) ? "Ceteris paribus", without anything else happening, just those little money issues...

"I guess the 16 euro gelato will still be with us for a while. "

ReplyDeleteI understand that one of the big drivers for things like a 16 euro gelato is that Italy (and the rest of Europe) relies heavily on sales taxes and has high payroll taxes. The flip side is that Italy has low corporate income taxes.

Apparently some economists think America should reduce corporate taxes and introduce a VAT. Twenty five dollars for a Big Mac, anyone?

The way you get a 16 euro gelato in Italy is when you buy a 3 euro gelato and then sit down at a table to eat it. They charge for sitting vs standing. Sitting can double or triple the cost, and for the unwary tourist, they can really gouge you. I've heard of people being charged 15 euros for sitting.

DeleteLook for the "banco" price vs the "tavolo" price. Banco is standing at the bar, tavolo is sitting at a table. If it's not posted, ask before you sit down.

Better yet, get your gelato then head to the nearest piazza and sit on the edge of the fountain to eat it.

Just one of the many ways you can get over-charged in Italy.

Whatever the merits or demerits of the deflation story, an analysis of relative price changes, no matter how subtle, will not get us to an answer. When I was a child, a widespread story, on which undergraduates were tested, was that "quality improvements" were of such magnitude that 2% inflation was really 0% inflation. I have not kept up with this in detail, but I've always liked the story. I have no evidence that the FED thought this way when it decided that 2% was a nice inflation rate. In any case, if this story is near the truth, Italy is being subject to 1.4% deflation per annum.

ReplyDeleteI am posting this here, instead of under the next post ("Krugman on the attack")

ReplyDeleteYou wrote: "I generally don't read Paul Krugman -- bad for the blood pressure -- and I even less often respond -- don't dignify the insults or feed the trolls."

Have you been on a lot of airplanes lately?

With large national government deficits and debt, why does Japan have deflation?

ReplyDeleteEU Commission has significantly reduced maximum permissible roaming prices at 1st of July 2014 (after setting maximums at 1st of July 2012 and reducing them at 1st of July 2013). This is likely the only reason for deflation in communications sector.

ReplyDelete