It starts with a blast:

"Higher capital ratios are unlikely to prevent a financial crisis."Wow! How do they reach this dramatic conclusion? The post and underlying paper are empirical, collecting a very useful dataset on bank structure across countries and a long period of time. They show, for example, that

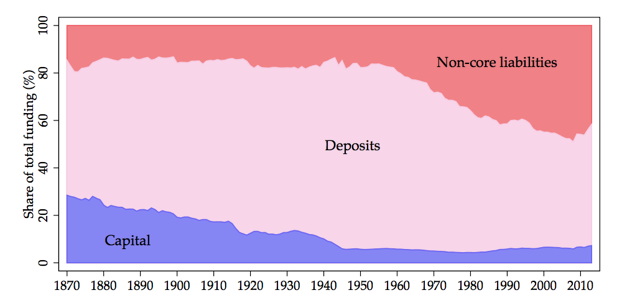

bank leverage rose dramatically between 1870 and the second half of the 20th century. In our sample, the average country’s capital ratio decreased from around 30% capital-to-assets to less than 10% in the post-WW2 period (as shown in Figure 1 below) before fluctuating in a range between 5% and 10% in the past decades.Here is the very nice Figure 1. (It shows not just how capital has declined, but how reliance on more run-prone wholesale funding has increased. The fact that capital used to be 30% is one that we need to reiterate over and over again to the crowd that says 30% capital would bring the world to an end.)

|

We find that the capital ratio provides virtually no information about the probability of a systemic financial crisis.

Whether used singly or along with credit, higher capital ratios are associated, if anything, with a higher probability of a crisis.There used to be a lot more capital, and there used to be a lot more financial crises.

Wow. Now, (this is a good quiz question for a class), before you click the "more" button: Do the facts justify the conclusion? And if not why not?

Well, obviously not, or at least not yet. Ask the standard questions of any correlation or forecast in economics: 1) Does it reflect reverse causality -- rich guys drive Mercedes, but driving a Mercedes will not make you rich? 2) What causes the movements in the right hand variable (capital)? They are not random experiments, whims of the God of financial regulation. 3) What other causes of crisis are there (the error term)? Why are they not correlated with the right hand variable (capital?).

The opportunities for reverse causality are rich -- and fully acknowledged. Continuing the above quote:

"... higher capital ratios are associated, if anything, with a higher probability of a crisis. This mechanism is consistent with banks raising capital in response to higher-risk lending choices, rather than as a buffer against a potential systemic crisis event in the economy...."The paper is even clearer:

"...Such a finding is consistent with a reverse causality mechanism: the more risks the banking sector takes, the more markets and regulators are going to demand banks to hold higher buffers."It is not surprising that more fire extinguishers predicts either nothing, or more houses burning down. People buy fire extinguishers in fire-prone areas. It is not surprising that airplanes in which pilots wear parachutes are more likely to crash than when pilots don't wear parachutes. It would be an obvious mistake to conclude that buying fire extinguishers and wearing parachutes do not increase house or pilot safety.

Similarly, it is not at all surprising that banks, their depositors, their equity holders, and their regulators all would choose more capital when the chances of a crisis are greater. It is not at all surprising that the probability of a crisis in equilibrium is independent of the amount of capital chosen -- the supply of capital just balances the dangers of crisis. All of this is not at all surprising if adding more capital at any point in time would further reduce the probability of a crisis.

Other effects are just as important. The probability of a crisis also depends on deposit insurance, topnotch risk regulators out there spotting impending crises (hmm), bailouts, and so on. We have arguably traded less capital for more of these other responses -- inefficient, in my view, full of moral hazard, but effective in putting out fires -- so no wonder less capital comes with less (before 2008) or no change in frequency of crisis.

Once again, the authors are completely upfront -- eloquent indeed -- about other effects (error terms correlated with the right hand variable)

Increasing sophistication of financial instruments allowed banks to better hedge against uncertain events. As a result, the business model of banks became safer, implying a lower need for capital buffers (Kroszner (1999), Merton (1995)). Furthermore, diversification and consolidation in banking systems may have reduced the equity buffers required to cope with risk (Saunders and Wilson (1999)).

Probably the most prominent innovation in this respect was the establishment of a public or quasi-public safety net for the financial sector. Central banks progressively took on the role of lender of last resort, allowing banks to manage short-term liquidity disruptions by borrowing from the central bank through the discount window (Calomiris et al. (2016)). The second main innovation in the 20th century regulatory landscape was the introduction of deposit insurance. Deposit insurance mitigates the risks of self-fulfilling panic-based bank runs (Diamond and Dybvig (1983)); but it may, however, also induce moral hazard if the insurance policy is not fairly priced (Merton (1974)). ...

A last and arguably more recent extension of guarantees for bank creditors relates to systemically important or “too-big-to-fail” banks. While explicit deposit insurance tends to be limited in most countries to retail deposits up to a certain threshold, large banks may enjoy an implicit guarantee by taxpayers. This implicit guarantee could also help account for the observed increase in aggregate financial sector leverage, although the subsidy is difficult to quantify.What do the authors do about this? Amazingly, nothing. The paper fully acknowledges reverse causality as a plausible, and perhaps the most plausible interpretation, it outlines a host of other effects correlated with the right hand variable -- and then goes on to do nothing about it.

Regression econometrics these days is exquisitely sensitive to these issues. Paper after paper tries to isolate a "natural experiment" -- an increase in capital unrelated to increased probability of crisis -- or adds differences in differences in differences and a plethora of fixed effects and controls to try to measure the correct cause and effect relationship. This isn't always successful, and throwing out 99% of the data variation is sometimes more confusing than revelatory, and sensitive to just which 99% one throws out, but give them credit for trying. This paper doesn't even try.

Now, perhaps I have mischaracterized the "fact," in the above graph, emphasizing the association of declining capital over time with the frequency of crises. In fact the real evidence in the paper comes from a forecasting regression across time and across countries, of crisis at time t+1 on capital and other variables at time t

So, does this capture the correlation of declining capital ratios over time with the chance of crisis? Or does it capture the correlation of different capital ratios across countries with the country's chance of crisis? (Notice here the severity of crisis is left out, that's the later fact.) Well, both since we have both i and t.

Alas, (p. 16)

"To soak up cross-country heterogeneity, we will include a country fixed effect αi for each of the 17 countries...."That means they throw out the variation, do countries which on average have higher capital standards than others, on average have fewer crises? Why in the world would one throw that out? Why are cross-country capital ratios more polluted by endogenous responses than over time capital ratios, and cross country crises more contaminated by correlation with other effects -- amount of mortgage market interference, lender of last resort effectiveness, deposit insurance, etc? If the time series variation is important and exogenous, why exclude the major source of variation, the pre vs. post WWII variation?

in sum, commandment #5 of regression running is: Think about the source of variation in your data. Don't just randomly throw in country or time fixed effects or split the sample in half.

(Yes, "Pooled models are included in the appendix as well." But that isn't much help. )

The problem is not with the paper, which is otherwise excellent. The problem is with the paper's headline conclusion -- more capital therefore does not help to reduce the chance of a crisis.

The paper does show, and correctly claims it shows, that capital ratios (in equilibrium) are not helpful in forecasting a crisis.

"our first main finding is that, perhaps counterintuitively, the capital ratio is not a good early-warning indicator, or predictor, of systemic financial crises."For example, a regulator who wants to stop crises might look at banks piling on capital as a danger signal, the way passengers in my glider are sometimes suspicious when I ask them to put on a parachute. The paper verifies that capital is useless as a forecaster. That is a good, solid point. We might have expected the opposite sign -- more capital, more crisis -- as a useful forecast. But we cannot infer that adding more capital would not reduce the chance of a future crisis.

The paper also makes a nice point about capital, which is not just nice because I agree with it but because the data more clearly support it: More capital means the crisis, when it comes, is less severe. The wearing of parachutes may not forecast safer flights, because people tend to put them on when the flight is more dangerous anyway. But when people do wear parachutes, the outcomes of midair collisions are a lot less severe.

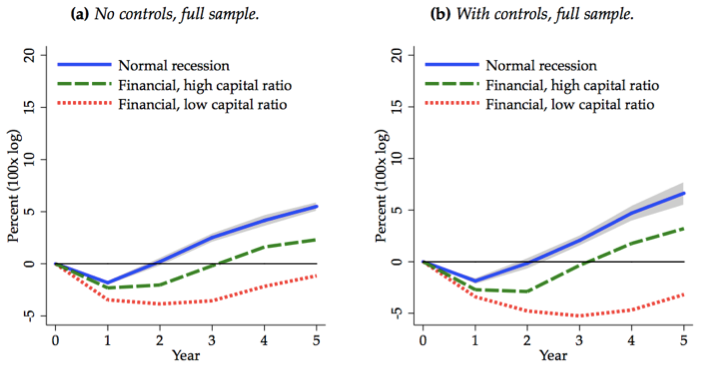

"a more highly levered financial sector at the start of a financial-crisis recession is associated with slower subsequent output growth and a significantly weaker cyclical recovery. Depending on whether bank capital is above or below its historical average, the differences in social output costs are economically sizable. Real GDP per capita five years after the start of the recession is about 5 percentage points higher when banks are well capitalised than when they are not. This difference is displayed in Figure 2."

One can complain about reverse causality here too, but the point is not to whine, the point is to see if there is a really plausible channel, and the strength of the counterargument here seems less strong to me. It does not seem likely that if people knew an unusually bad recession was ahead, or that the economy was unusually sensitive to financial shocks, they would then equilibrate to less capital.

But why did the authors take a very nice paper that shows that equilibrium (including political and economic equilibrium) doesn't forecast a crisis, and plaster on it a completely unsubstantiated conclusion that more capital would not help to reduce the probability of crisis?

At first I suspected it wasn't their fault. Oped editors frequently pick titles without the authors' knowledge. But it's in the first sentence of the paper abstract.

"Higher capital ratios are unlikely to prevent a financial crisis."The authors say it again at the end of the oped,

the main role for bank capital appears to lie not so much in eliminating the chances of systemic financial crises, but rather in mitigating their social and economic costs – a distinct but arguably more important benefit.(My emphasis.) And the paper repeats the point,

we find that macroprudential policy, in the form of higher capital ratios, can lower the costs of a financial crisis even if it cannot prevent it.

history does indeed lend support for a precautionary approach to capital regulation. Its main role appears to lie not so much in eliminating the chances of systemic financial crises, but rather in mitigating their social and economic costs...Why am I making such a fuss?

First, in the sad state of current academic-media interactions, this is sure to be picked up and quoted as "A major study shows that" more capital does not help to prevent crises. (Perhaps in a week or two I'll find time to do some google searches to verify this conjecture.) No, studies that claim a result do not always show a result! This is a classic case. Please, ask what evidence the "study" offers, and is it even vaguely logically coherent!

Second, it is a very instructive case study for students to look at -- how to ruin a great paper by trying to make sexy claims that are not supported by the logic of the paper.

Third, in that vein it allows me to reiterate some important lessons about how to run regressions, lessons that we tend to forget too often.

I don't have much to add besides saying this was a great post, thanks!

ReplyDeleteIt's regulation and supervision. Credit the FDIC, OCC and Fed. Plus, of course deposit insurance.

ReplyDeleteI was at a Bar Association Meeting in New Orleans last week. I listened to a presentation by the Loan Syndication and Trading Association.

ReplyDeleteAmong the market trends they noted was an increase in what they called "Direct Lending", which is lending without involving a bank as a lender or intermediary. They said that the direct lenders are Business Development Companies (a sub-species of regulated investment company) and private equity funds.

They identified three reasons for the shift from bank lending: 1. The banks have been hampered by the regulators seeking to stop banks from acquiring risky assets. The Inter-Agency Guidance on Leveraged Lending issued by US bank regulators in 2013 is very restrictive and has been rigorously enforced by them. 2. Investors are looking for higher yielding investments, and 3. Middle Market companies (EBITDA > $25 million <$50 million) have difficulty accessing capital markets.

The banker who made this part of the presentation was a bit miffed by the trend, particularly by the regulatory issue. When asked he said that the bank's competitive advantage over the private lenders was the bank's much lower cost of funds.

I think the policy implication here is that regulation could conceivably result in regulatory arbitrage where unregulated entities take lines of business from regulated entitles, and leave us no better off. The money market fund industry is an example of that.

Second, I think that bank capital requirements should be increased dramatically, but this must be accompanied by a reduction of asset side regulation like the above mentioned Guidance. I believe that the proposal in the House by Rep. Hensarling makes that trade off. Trump seems to still have the mentality of a real estate developer, who is always pushing for more credit on easier terms. His administration may try to ease the asset side regulatory burden.

Third. I commend the article from the Thursday, April 13, Wall Street Journal: "Curtains for Global Financial Regulation: With Trump in the White House, the G-20’s dream of world-wide bank controls is dead." by Peter J. Wallison.

https://www.wsj.com/articles/curtains-for-global-financial-regulation-1492037557

Fat Man,

DeleteYou make interesting points. But I’m not sure about your claim that “regulation could conceivably result in regulatory arbitrage where unregulated entities take lines of business from regulated entitles, and leave us no better off. The money market fund industry is an example of that.”

I suggest that actually the latter outcome DOES MAKE us better off. Reason is that that outcome is actually a move towards (or comes to the same thing as) full reserve banking and that has the following merits.

1. Entities that accept deposits (i.e. entities who claim investors’ money is totally safe) put such money only into relatively safe investments. Thus failure is unlikely or impossible (depending on exactly how safe the latter investments are.)

2. People who want to take bigger risks with a view to potentially bigger rewards are free to do that, but there is no FDIC or taxpayer back up for that activity, and quite right.

That eminently rational arrangement makes us “better off” doesn’t it?

I believe Fat Man makes a good observation about the possibility of regulatory arbitrage, although in my experience both as insolvency counsel and as an econometrician, the greatest part of direct lenders' loan portfolios consist of credits acquired from regulated lenders after the regulated lender's loan defaults. The direct lender buys the classified credit at a substantial discount, then restructures the credit.

DeleteThat said, I still encounter a very substantial amount of loans originated by direct lenders that a bank or other regulated lender would not make. In either case, the direct lender has the loan because regulations lower the value of the loan to the bank, or prevent the bank from undertaking the loan's risk.

Mr. Musgrave: During the panic of 2008, the Federal Government guaranteed all MMF holdings. I believe that the SEC has now ordered MMFs that are not limited to investing in Treasuries off limits to non-individual investors. I assume that is because they want to limit the size of the problem in any future panic.

ReplyDeleteJohn,

ReplyDeleteIMHO, a better way to look at historical data regarding bank leverage would be bank survival rate vs. leverage.

I have always had a problem with the tag "financial crisis" and they are not even indicated on your graph. It is much easier to identify individual banks / financial institutions that cease to exist vs. those that continue to exist so why not compare leverage ratios between the two?

My suspicion is that a higher leverage leads to better short term results with a higher degree of bank fragility.

John,

ReplyDeleteThe capital ratio of a bank is not the same as the leverage ratio of a bank.

https://en.wikipedia.org/wiki/Capital_requirement

Total Equity (TE) = Shareholder equity + Retained Earnings + Reserves

Tier 1 Capital Ratio (CAR) = Total Equity / Credit Risk Adjusted Value of Assets

Tier 1 Leverage Ratio (LEV) = Total Equity / Non-Risk Adjusted Value of Assets

For either ratio, the "when sold" value of share holder equity is used (not the market value).

Presumably, we should be able to tease out a debt / equity ratio this way:

Total Non-Risk Adjusted Value of Assets = Total Debt (Par Value) + Total Equity

Debt / Equity Ratio (DER) = ( 1 / LEV ) - 1

And so, if a bank has an 8% Tier 1 leverage ratio, this should correspond to a 11.5 : 1 debt to equity ratio.

Notice that capital adequacy can rise and fall independently of leverage depending on total credit risk exposure.

From the paper:

"...bank leverage rose dramatically between 1870 and the second half of the 20th century..."

The graph does not depict the leverage ratio, it depicts the capital ratio.

For all I know (just from the graph), leverage was the same between 1870 and the second half of the 20th century. The capital ratio could have risen (with stable leverage) simply because risk weightings were falling during that time period.

I don't believe that was the case, but the paper seems to use capital ratio and leverage ratio interchangeably when they are not the same thing.

Got that backwards...

DeleteFor all I know (just from the graph), leverage was the same between 1870 and the second half of the 20th century. The capital ratio could have FALLEN (with stable leverage) simply because risk weightings were RISING during that time period.

Again, I don't believe that is the case, but my point is still that capital ratio and leverage ratio are not the same thing.

According to Columbia's Charles Calomiris, there are two 800 lb gorillas in banking;

ReplyDeletehttps://papers.ssrn.com/sol3/papers.cfm?abstract_id=2909846

----------------quote---------------

The protection of bank debt and the targeting of risk-promoting

mortgage subsidies are the primary sources of systemic risk in banking systems around the world.

These two threats are related. Deposit insurance and other debt protection (without offsetting strict prudential regulation and supervision) creates rents outside the normal budgetary process that funds and encourages risk taking. Governments create rents from protection of banks not just to reward bankers, but also to target credit subsidies to preferred groups of

borrowers. The same regulatory system that devises deposit insurance and prudential regulation typically also creates a host of influences that guide credit to preferred borrowers.

Tackling these twin problems with macro-prudential regulation is difficult because the agencies charged with regulatory oversight are subject to the political influences that give rise to these gorillas in the first place. Furthermore, the incentives of economists tend to make them accomplices in the drama that underestimates the importance of the primary threats to systemic stability, while overestimated less important influences, such as network effects.

What is necessary is a fundamental restructuring of the banking system that (1) reduces government protections against loss on bank debt, (2) eliminates mortgage risk subsidization, (3) restores a robust, rules-based lender of last resort to tackle systemic risk (in place of deposit

insurance and unconditional bailouts of banks), and (4) places strict limits on the funding of real estate risk through the banking system.

--------------endquote--------------

'Why am I making such a fuss?

ReplyDeleteFirst, in the sad state of current academic-media interactions, this is sure to be picked up and quoted as "A major study shows that" more capital does not help to prevent crises.'

... already happened:

https://spontaneousfinance.com/2017/04/17/thicker-capital-buffers-do-not-prevent-banking-crises/

... I don't get why people don't seem to get this bank-capital-ratio thing. Constantly I'm told that higher-capital ratios would reduce lending (which is nonsense because how banks fund themselves is irrelevant for how much they lend out) and now I'm probably going to hear a lot of variations of "more capital does not help to prevent crises"

... For May I'm planning to publish on my blog a comprehensive post explaining with the help of simple bank balance-sheet examples the pernicious effect of the low bank capital ratios we have today. Maybe that helps.

At the same time, capital adequacy does help with lending (that seems to be the literature consensus for the crisis period). So in fact in bad times the opposite of the non-sense happens.

DeleteAt the same time, I still don't understand myself how higher capital requirement will not affect risky lending. Please elaborate if you can.

All of the talk about capital, and no talk about "money." What makes banks special is not that they issue debt; anyone can issue debt. Bank debt is special because a lot of bank liabilities are "money." Bank deposits, for sure, but also repo and commercial paper.

ReplyDeleteThe nature of money is that it is callable. If it is not callable, it cannot be liquid. And the economy needs liquidity. Information is opaque; no one has the means or incentive to examine bank assets. Banks that issue money are vulnerable to bank runs. Bank runs produce crises. That has nothing to do with capital.

A bank can have a lot of capital. It may not be "too big to fail." But if the bank's assets are long-term and illiquid, and its liabilities are liquid and short-term, it is vulnerable to a run no matter how much capital it has. The question boils down to this: are banks with higher capital ratios less likely to suffer runs?

We might note that after Lehman, the money market mutual funds suffered a run, even though the shares are mark-to-market and not fixed in principal.

Great post - where can I find the other 9 commandments of regression running?

ReplyDelete