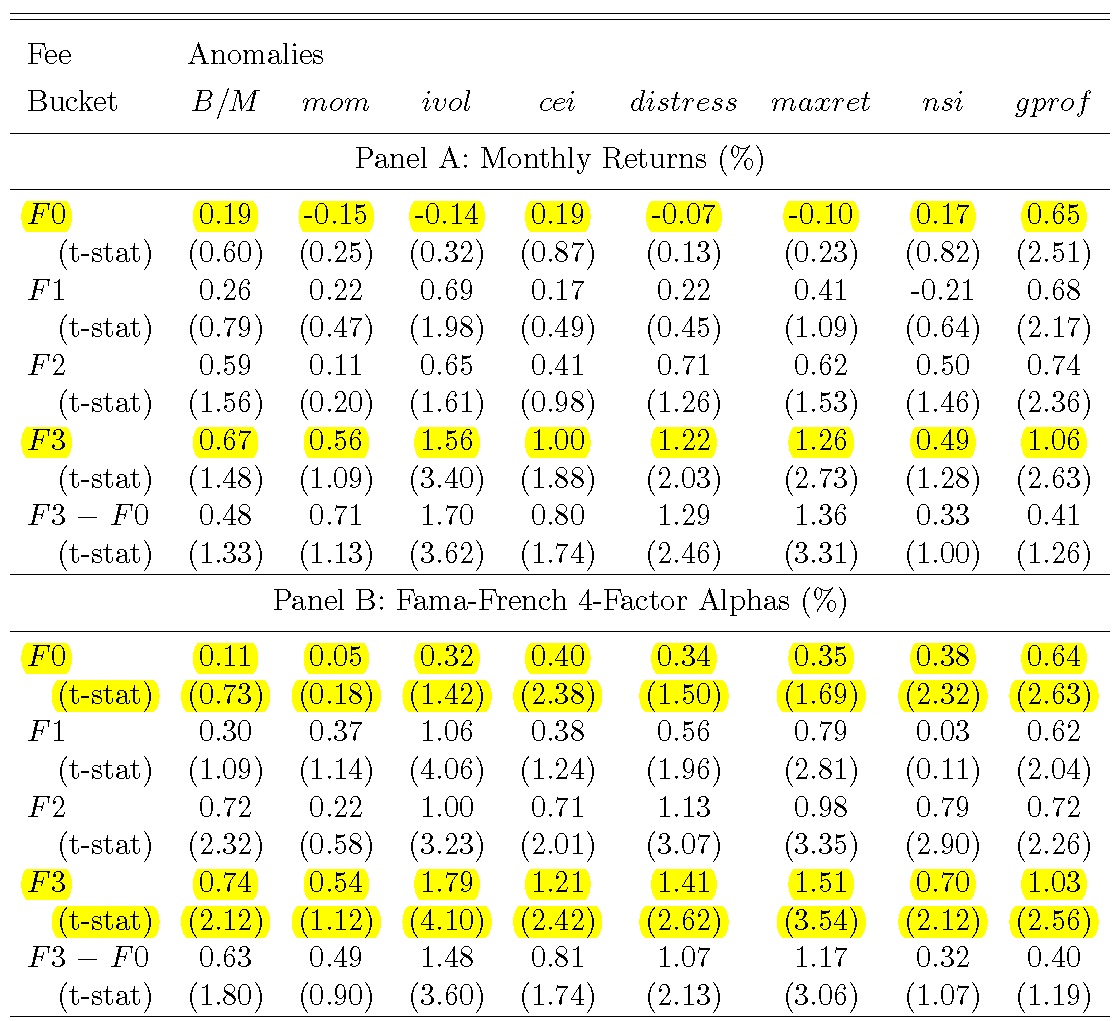

Charles uses the Fama-French (2008) variables to forecast stock returns, i. e., size, book to market, momentum, net issues, accruals, investment, and profitability. \[ Ret_{i,t+1} = \beta_0 + \beta_1 Size_{i,t} + \beta_2 BtM_{i,t} + \beta_3 Mom_{i,t} + \beta_4 zeroNS_{i,t} + \beta_5 NS_{i,t} + \beta_6 negACC_{i,t} + \] \[ + \beta_7 posACC_{i,t} + \beta_8 dAtA_{i,t} + \beta_9 posROE_{i,t} + \beta_{10} negROE_{i,t} + e_{i,t+1} \] He forms 25 portfolios based on the predicted average return from this regression, from high to low expected returns. Then, he finds the principal components of these 25 portfolio returns.

|

| Source: Charles Clarke |

And the result is... hold your breath... Level, Slope and Curvature! The picture on the left plots the weights and loadings of the first three factors. The x axis are the 25 portfolios, ranked from the one with low average returns to 25 with high average return. The graph represents the weights -- how you combine each portfolio to form each factor in turn -- and also the loadings -- how much each portfolio return moves when the corresponding factor moves by one.

No surprise, the 3 factors explain almost all the variance of the 25 portfolios returns, and the three factors provide a factor pricing model with very low alphas; the APT works.

Now, why am I so excited about this paper?

_van_het_Amsterdamse_lakenbereidersgilde_-_Google_Art_Project.jpg/1024px-Rembrandt_-_De_Staalmeesters-_het_college_van_staalmeesters_(waardijns)_van_het_Amsterdamse_lakenbereidersgilde_-_Google_Art_Project.jpg)