The last paragraph caught my eye:

"The election should lay out each candidate's fiscal grand bargain and growth strategy. Let us compare them. They matter. This could make up the heart of a historically important presidential contest."

Yes indeed. But I don't think Austan's partisan tone is justified -- he was criticizing Republicans in Iowa. This could have been written by the Ron Paul campaign, followed quickly by acid comments that "tax the rich" is not a "fiscal grand bargain" with any hope of closing the long-run budget gap, and neither it nor more Solyndras are a "growth strategy" as economists understand long-run growth.

Here's an optimistic interpretation: Austan advises the Obama campaign. Perhaps he's dropping a hint that the campaign will unveil that grand bargain -- with a plan to get it through Congress -- and a serious growth strategy. If they do, they'll win the election and save the economy.

Austan also gets it absolutely right that

"The true fiscal challenge is 10, 20 and 30 years down the road. An aging population and rising health-care costs mean that spending will rise again and imply a larger size of government than we have ever had..."My only quibble is that this challenge may not be so far "down the road" as Austan supposes. Bond markets panic when they see danger ahead. (Lots more here.)

The more controversial question is Austan's view that our current enormous deficits are just due to the recession, not unusually profilgate spending, and the budget will quickly recover once the economy recovers.

John Taylor took Austan to task on that question, pointing out that the Administration's February budget proposal showed no reversion to normal spending even as the economy recovers. I think John's being a little harsh here. After all, the budget was quickly ignored.

But you're here for economics, not personalities. How much of our deficit is just "normal" response to an unusually deep recession? Will the deficits fade away quickly as the economy recovers? Is spending really not a problem?

Deficits do and should rise in recessions. Tax revenues fall in recessions. A family that runs in to hard times -- business doing badly, losing a job, etc. -- should dip in to savings, or even borrow to keep expenditures relatively constant, and pay that back when good times return. Governments are the same. This is uncontroversial "consumption smoothing" and has nothing to do with attempts at "stimulus." You may -- as I do -- think that government is spending grossly too much overall, but that's a different question than the timing of that spending.

But how much? Is this the story, or is our Government off on an ill-advised shopping spree during these hard times?

Austan cites "automatic stabilizers"

"Most of the increase in the deficit during a downturn doesn't come from new policies in Washington. The deficit rises because both spending and taxes automatically adjust when the economy struggles. Unemployment insurance payments rise and more people qualify for Medicaid and food stamps. Incomes fall so people pay less taxes"This, as far as I can tell, is not quite true. Here is the CBO's "cyclically adjusted deficit"

|

| Source: http://www.cbo.gov/ftpdocs/114xx/doc11471/05-27-AutomaticStabilizers.pdf |

Quoting from the CBO, "The budget balance without automatic stabilizers is an estimate of what the surplus or deficit would be if GDP was at its potential, the unemployment rate was at a corresponding level, and all other factors were unchanged." Now, one can quibble with their calculation, but the "without automatic stabilizers" deficit is not even close to a flat line!

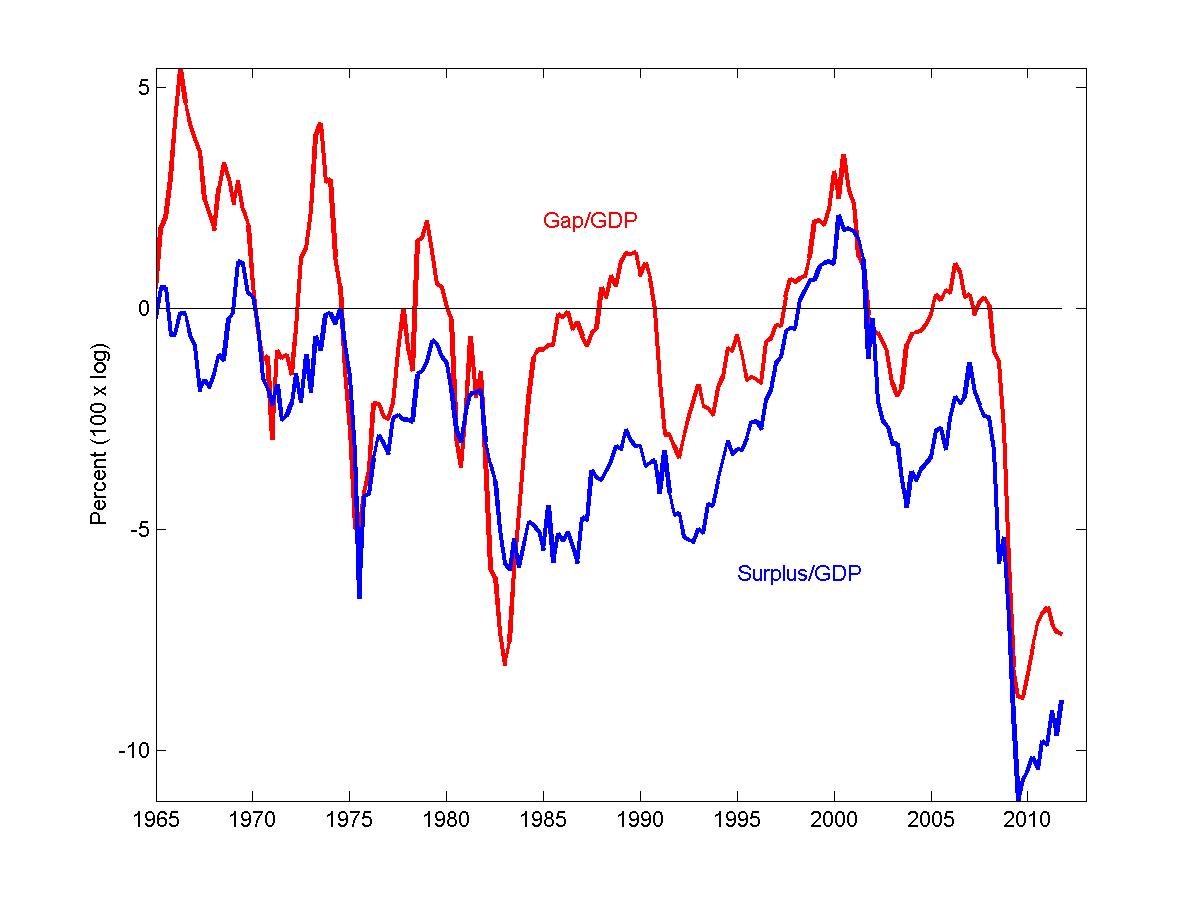

Austan is close to right however. It is true that our Government typically chooses to run larger deficits in recessions. It is also true that our current deficit choices are not out of line from the historical pattern, given the depth of the recession. Here's a graph to make that point:

|

| Surplus/deficit and output gap (GDP - potential), as percent of GDP |

The red "gap" line is the percentage difference between GDP and "potential GDP." (I don't put much stock into the "potential" concept, but it provides a nice trend line.) The blue line is the Federal surplus or deficit, also as a percent of GDP.

You can see that deficits regularly get much bigger in recessions. Roughly speaking, the deficit movement is just about equal to the GDP gap -- if GDP falls $100 billion, the deficit increases $100 billion. Our deficit, about 10% of GDP, corresponds to a 10% fall in GDP, consistent with the usual pattern.

So, Austan is saying, in the tight confines of the WSJ's word count, that when the GDP gap (red line) recovers, if the Goverment follows the same choices as in the past, the massive deficits will largely disappear (blue line).

How do I keep worrying?

First, we will still have racked up an impressive debt. Each year of deficits equal to 10% of GDP adds 10 percentage points to our debt/GDP ratio. Greece is out there not too far away. Even if the deficits pass, we still have to pay off the debt...Just as the "long term" problems settle in.

Second, look at the longer-term trends. 1969-1982 saw a steady deterioration in GDP and steady widening of the deficits. The strong growth in GDP from 1982 to 2000 corresponded with our first actual surpluses in a quarter century. But 2000 to now is starting to look suspiciously like another growth slowdown. If this is 1975 again, how long until we see 1999?

In other words, what if GDP does not quickly recover to "potential?" Here's a graph to make the issue clearer.

The green dashed line is real potential GDP. You can see that actual GDP has fell about 10% below this trendline -- and is sitting there. You can see huge increase in expenditures -- the rise in the red line by nearly 10 percentage points. Expenditures are sitting at 25% of potential GDP. The huge fall in tax receipts is also striking, and they're stuck too. (Tax receipts depend on more than GDP. In particular, you can see the effect of the two big stock market declines in 2000 and 2008.)

To get GDP back to the trend line, we need 10 percentage points of extra growth, on top of the 2.5% per year or so of trend growth. That's two years of 7.5% growth, which nobody is forecasting any time soon. This "catch-up-to-trend" growth has been the pattern of past business cycles. But what if we keep stumbling along at 2.5% - 3% growth for many years, racking up trillion dollar deficits each year we do so?

Third, to make it just a little more scary, notice the subtle flattening of the green "potential" line. Trend growth itself is slowing down. The trend grew at 4% in the 1950 and 1960s, slowed to 3% through 2000. It is 2.5% in the 2000s and the CBO's forecast is down to 2.3% for the 2010s.

Back to the family analogy: Yes, dip into savings or use the credit cards if you lost your job, but a new one is all lined up for 6 months from now. But maybe this family is facing a long and uncertain spell of unemployment, and it's going to end up working at Wal-Mart for a lot less money than before. Racking up debt with alacrity isn't such a good idea in that case.

So I think both Austan and John are right: Yes, this Administration (and Congress') spending response to the recession was not much different than previous ones. But it does not follow that long-run discretionary spending and debt accumulation are not a huge problem, even before the entitlements disaster hits. We may be looking at the long run!

Which brings us back to the beginning. "A fiscal grand bargain and growth strategy" really are important, perhaps more than Austan had in mind when he penned those poetic words! Catching up to trend, and then bending the trend upwards, will take some deep changes in how we do things.

Excellent post. My only complaint -- it didn't seem grumpy at all!

ReplyDeleteWhat do you think a fiscal grand bargain and growth strategy would look like?

ReplyDeleteIf I understood correctly, you think there is a problem in Government current deficit trend because we do not know how long this recession will endure.

ReplyDeleteWhat is not clear to me is the role you see government taking here. I mean, unemploiment at 8,5% sounds like great news when we think about Europe.

Let the economy sink? Printing money? What else?

I think you are being much too kind to Mr. Goolsbee. The CBO report you use (March 2010), combined with the OMB budget projections at the time, indicate outlays associated with automatic stabilizers in F10 through F14 account for about $200 to $250 billion of incremental Federal government spending per year. However, federal government spending increased from $3 trillion in F08, when the automatic stabilizer contribution was only $7 billion, to about $3.8 trillion in the subsequent years.

ReplyDeleteSince the increase in outlays is expected to be about $800 billion per year, and automatic stabilizers accounts for $250 billion, $550 billion, or over two-thirds of the increase in spending is not due to automatic stabilizers.

This is a far way from don't worry be happy, the deficit is only a cyclical concern.

Actually, I am here for economics AND personalities. I want to hear that Goolsbee is a twit. After all, we get that from Krugman all the time...

ReplyDeleteJohn, I am your former student, so I don't think you are a moron unlike Krugman :) However, it seems to me his criticism regarding a somewhat muddled position on stimulus is justified. For example, I am confused by the following:

ReplyDelete"

This is uncontroversial "consumption smoothing" and has nothing to do with attempts at "stimulus."

"

Isn't stimulus nothing but a form of consumption smoothing? You seem to be for it and against it simultaneously. Wouldn't be run of the mill consumption smoothing to prevent local governments from firing tons of employees via federal government deficit spending ? You don't make the distinction clear at all. Not at all like your Advanced Investments class :)

thanks.

I'm glad you allowed comments. I hope you continue to.

ReplyDeleteI think one of the big claims he is making is, the deficit was here when we got here, "The Congressional Budget Office forecast a $1.2 trillion deficit before the Obama administration even came into office." As opposed to being a result of President Obama's new era of big spending as portrayed in the Republican debate.

Maybe he wouldn't mind the Republican debates so much if the administration was being criticized for failing to deal with a large budget deficit already written into current law.

Sorry if this comment is attached to a different post than the intended one on Ricardian equivalence, but how does fractional banking (assuming a bank loan) not yield a net stimulus from a significant portion of the $100,000, given the economy is operating at less than "optimal" efficiency with banks having unused lending capacity?

ReplyDelete"But you're here for economics, not personalities.", yep! And thanks for having opened up comments!

ReplyDeleteagain on the theme of 'economics, not personalities' I have posted an idea for improving the public debate among economists:

ReplyDeletehttp://europlay.blogspot.com/2012/01/one-debate-to-rule-them-all.html