Argentina is going through some fun times (for macroeconomists)... After a two day holiday markets opened yesterday and the peso kept falling (-3%) despite the rate hike (300bps) on friday and the continued drain of reserves. We are trapped with Bill Murray in Groundhog Day. Same thing today... markets open with pressure on the peso. The central bank sold 300 millon of reserves in less than 10 minutes early in the morning when liquidity is at its lowest and it couldn´t sopt the run. Soon after it announced another rate hike of 300bps. Short term debt that expires on may 16 has a yield of 38.7% APR and there are 680 billon pesos of it waiting to mature in less than two weeks. Still the market did not respond and the peso kept falling, more than 8% with respect to yesterday´s close....Naturally my interest is particularly peaked by a country whose central bank seems powerless to stop inflation and devaluation in a time of fiscal stress. In fact, there are indications that raising interest rates, by making interest costs larger, make the fiscal problem worse and make devaluation worse, not better.

I asked Alejandro for a bit more to share with blog readers since we hear so little about this in the US. Here is his longer story backward:

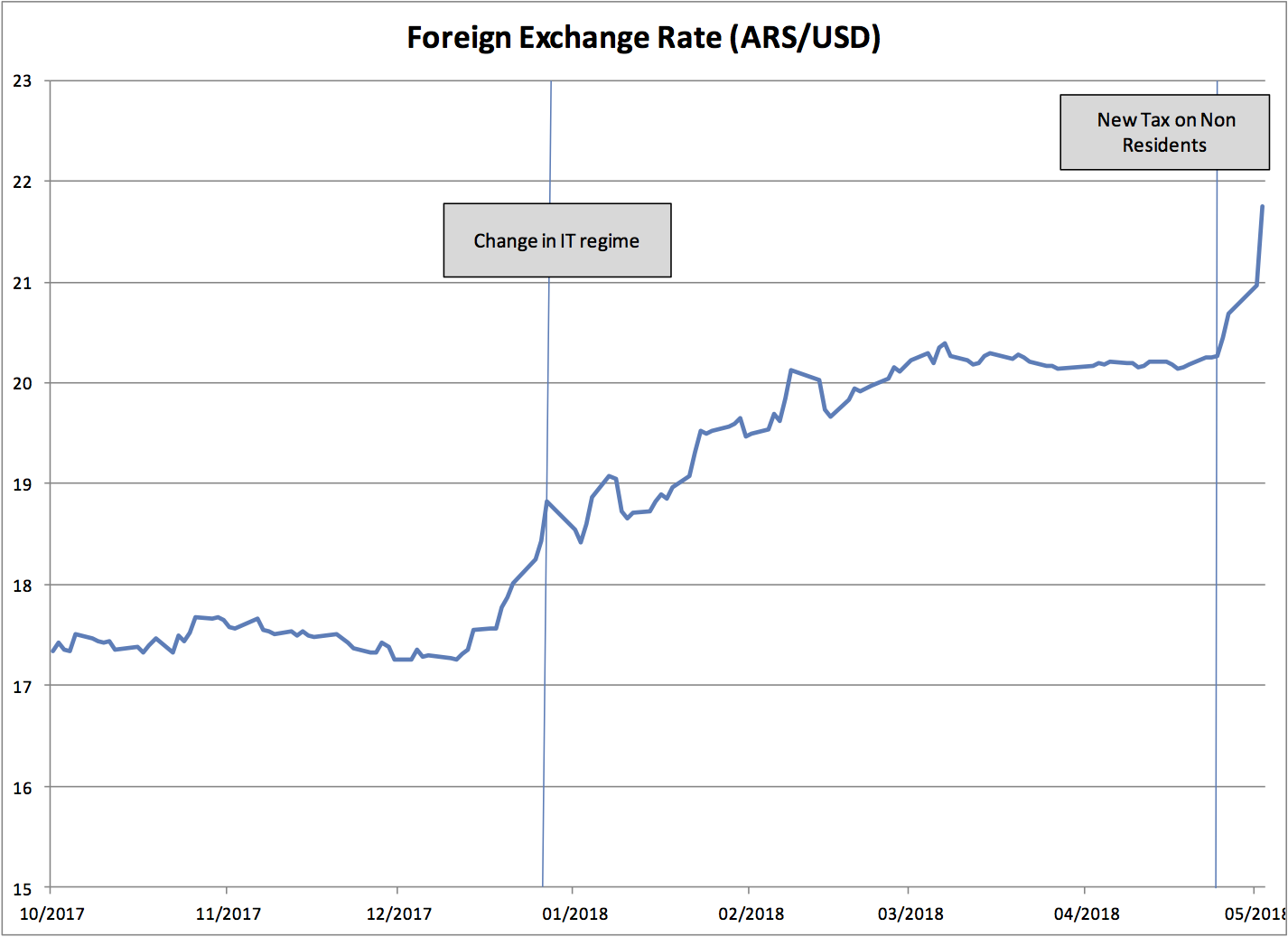

Groundhog Day: ...Like Phil Connors (Bill Murray) we got trapped in Punxsutawney by the perfect storm. Last year Congress passed a law changing the tax code which included a new tax on Central Bank debt held by non residents. The new tax became effective on April 25th. The new tax initiated a sell off by non residents which was absorbed by the CB which sold USD 2.1 billon between April 23rd and 25th without the dollar moving one cent (20.25 ARS/USD). The new tax coincided with the increase of the 10 year US treasuries yield and the strengthening of the dollar. The CB thought this was an external shock and that no further actions were going to be needed.

They were wrong. Pressure on the dollar continued on Thursday 26th. The CB sold USD 850 million but eventually had to let it go and the peso fell 1% despite their best efforts. Friday was the same thing all over again. Like Phil Connors, the CB started selling reserves as the previous days. But no matter what was offered nothing seemed to be enough so they decided to increase rates by 300 bps. The peso fell another 3% and USD 1.4 billion of reserves sold.

May started a little late in Argentina as markets were closed on Monday and Tuesday because of a National holiday but Wednesday 2nd was Groundhog Day all over again. Thursday 3rd was not any different. The peso started falling early on and the CB stepped in with an offer to sell USD 300 million which were sucked by the market like empty space. Immediately the CB raised rates by another 300 bps hoping to end the run with no luck. Without the CB in the market, bid/ask spreads rose and the market had trouble finding an equilibrium price, a last minute operation increased the closing price from 22.40 ARS/USD to 23.00 ARS/USD. Short term letters issued by the CB that mature in 13 days yielded 40% APR. Reserves fell to USD 56.1 billon from USD 62.6 billon in March.

Today (May 4th), the CB went for another rate hike. REPO rates are now at 48% and the dollar fell to 21.50 ARS/USD. To be continued…May 4 update:

Early in the morning before markets opened the Government made a coordinated series of announcements:

The Central Bank announced another rate hike of 675 bps bringing seven day REPO rates to 33% (passive) and 47% (active). One day REPO rates rose to 28% (passive) and 57% (active). It also announced that it lowered the upper limit on foreign assets that banks can hold (forcing them to sell dollars or limiting their future demand) and that it would continue operating on the foreign exchange (spot and futures) if needed.

The Secretary of the Treasury (Ministro de Hacienda) announced that it lowered the primary fiscal deficit target for 2018 from 3.2% of GDP to 2.7% of GDP. Spending cuts on public investment were announced.

The peso appreciated and the exchange rate decreased from 23.00 ARS/USD to 21.75 ARS/USD.May 8 Update:

Yesterday the peso kept falling and same thing today. FX is at a record high of $23.10 ARS/USD (5.5% up since yesterday). Central Bank absent from fx markets. President Macri will address the Nation in 15 minutes. CB short term debt yields

Days YTMWell so much for high interest rates raising the exchange rate.

8 42,8%

44 42,0%

71 41,0%

99 40,0%

134 40,0%

How did Argentina get to this place? Alejandro provided a lot of background which is useful to understanding this latest event.

...2015. The peso was appreciated in real terms and kept in place with capital controls, twin deficits were financed with money printing and loss of international reserves. The economy had been stagnant since 2011, inflation averaged 25% and markets were distorted everywhere.

But then there was light at the end of tunnel, Mauricio Macri with a center left to center right coalition won the presidential elections.

Macri and his team faced very difficult challenges. They successfully lifted capital controls; gained back access to international capital markets that were closed to Argentina due to the legal battle in NY over the 2001 default and started to bring relative prices back to order (some utilities were held constant in pesos at the same level they were in the 90´s).

The initial shock on the exchange rate (the peso depreciated by one third with respect to the dollar) and the increase in utilities put pressure on the CPI inflation which Macri had promised to control. The Central Bank (CB) increased rates to 38% trying to control inflation expectations and the dollar exchange rate. Like the previous government, they kept using very short term nominal debt issued by the CB to try to control the money supply (the ratio of debt to monetary base in November 2015 was 0.74).

The first year was bad as expected, but people were optimistic. GDP fell 1.8%, inflation reached 40%, and debt started to accumulate at a rate of 5% of GDP per year give or take. The initial forecasts made by the government placed inflation around 25% (same as the previous year) and growth around 2.5% (fueled by FDI which never came).

The fiscal deficit remained high and was financed foreign debt. This resulted in a huge capital inflow which was absorbed by the CB accumulating reserves and sterilizing the equivalent amount of pesos issuing more short term nominal debt.Are you with me? Opening up means a jump in the reported exchange rate, and thus the price level. The central bank responds by raising interest rates, and fiscal deficits start to pile up. Is inflation always and everywhere a fiscal problem? The next step has the central bank still fighting inflation in the face of the exchange rate and fiscal problems.

In 2017 the CB officially announced that it started implementing an Inflation Targeting (IT) regime. The goal for the year was 12%-17% inflation, 8%-12% in 2018 and 5% in 2019. The treasury also announced a primary fiscal deficit target for the following years: 4.2% of GDP in 2017 and 3.2% of GDP in 2018 (these figures do not include interest payments of over 2% of GDP and deficit incurred by the provinces and municipalities).

Soon after the implementation of IT the CB faced it first real test. As the midterm elections approached, and former president Cristina Fernandez de Kirchner was perceived as a real threat, the peso started falling. This coincided with higher inflation numbers than expected which drifted away from the 17% upper bound. The CB responded by raising rates slightly and eventually selling reserves. People though the CB won the round and Cambiemos (Macri´s ruling coalition) won the midterm elections.

With renewed confidence and little time to go the CB decided to bring down inflation in line with the target as market expectations drifted even further. Some economists noted that even all the efforts done by the CB inflation was still at the pre Macri times (around 25%) and that the inflation dynamics were no different than the one observed after the January 2014 devaluation of the peso, with monetary aggregates growing at 30% per year on average, just like before, and a ratio of CB nominal debt to monetary base of 1.4 (double the amount from 2015).

Then came December 2017. Inflation reached 3.2% that month (although the final number was not known at the time, high frequency and other private estimates were showing that inflation was rising rapidly) for a final number of 25% over the year. This represented a 10% deviation from the center of the IT goal. The government got scared that the high rates would hurt economic activity in the future (GDP grew 2.9% in 2017) and that they were not enough to bring inflation down to the target so they decided to change the target for 2018 and 2019. The new targets were 15% and 10% respectively.

The announcement was done on December 28th, the equivalent of April´s Fool in the US, in a joint conference held by the President´s Chief of Staff, the Secretary of the Treasury, the Secretary of Finance and, a grumpy faced, President of the CB. Many viewed the change in the target and the way it was announced as a lack of independence of the CB, especially since the monetary authority had publicly stated that “changing the target was like having no target”.Older history. Argentina in the 1990s is a lovely (sad) test case, as even 100% backing of the currency is not enough to peg an exchange rate, because the government does not back the debt. If it could back the debt, it wouldn't have to borrow! So even a currency board is not immune from the inflationary effects of fiscal problems.

The peso had started to fall before the change in the IT regime (anticipated shock or inside trading?) but the rally on the dollar kept going as the CB lowered rates and peso denominated assets became less attractive to investors. To make matters worse, inflation expectations kept raising as the credibility of the IT regime plummeted and the inflation numbers for January and February turned out to be higher than expected. The CB responded with announcements stating that the increase inflation was temporary due in part to the recent jump in the value of the dollar and that they were ready to raise rates if inflation did not decrease. The CB also started selling reserve in early March to calm down the dollar. Interventions were relatively small, between USD 30 million and USD 400 million in a market that operates an average daily volume of USD 600-800 million, and they continued until early April when things appeared to calm down.

In the early 90, after two hyperinflations, Argentina adopted the Convertibility, i.e. a fixed the exchange rate (1 ARS/USD). The experiment lasted ten year until a global strengthening of the dollar coupled with other external shocks (and homemade mistakes) spooked away the capital inflows that were needed the finance Argentina´s fiscal deficit and ballooning debt.

In December 2001 President de la Rua resigned, debt was defaulted and the economy collapsed even further. The Convertibility ended and the peso started to float (with interventions) after an abrupt devaluation (after a short overshooting the dollar stabilized around (3 ARS/USD). The depreciated real exchange and booming commodity prices acted like an adrenaline boost on the real economy which started to grow.

Then Populism happened.

Argentina's inflation problem begins and ends with money printing. The monetary base has been growing about 30% per year for the past 8-9 years, because the central bank has been financing the government's deficit. The government hasn't been able to reduce the deficit, and they have apparently not tried or have been unable to finance the deficit with legitimate debt.

ReplyDeleteSelling reserves to stem the decline in the peso is futile if the reduction in reserves does not result in a reduction in the money supply. Imposing a tax on foreign holders of central bank debt is a terrible idea, since that only weakens demand for pesos at a time when their supply is super-abundant. It's time for some supply-side thinking in Argentina, coupled with some good, old-fashioned fiscal discipline of the spending-cut variety.

It is always the fiscal problem and political weakness.

Delete'Caputo respondio "Es un movimiento que podía venir, que no nos agarró por sorpresa y estamos perfectamente preparados para resolverlo sin inconvenientes"

DeleteFinance Minister Caputo answered that (the financial chaos) was "a movement that could happen anytime, it did not take us by surprise, and we are perfectly prepared to solve it without any trouble".

It is not political weakness, Luis, it is moral weakness. How can Argentina be taken seriously when they are lying all the time?

They are not taken seriously and probably never will

DeleteWhat's interesting is this:

ReplyDeletehttps://tradingeconomics.com/argentina/gdp

Look at the GDP spike right around the time after the financial crisis in 2008. 2009-2011. Wow.

Also breaks out GDP by industry and has a lot of other interesting breakouts, similar to FRED. What's curious is you look at the graph of the inflation rate in Argentina from 2013 on with an oscillation in GDP from 2013 to 2016 - dip, rise, dip. Curious indeed. GDP is only part of the story, of course.

John,

ReplyDeleteThank yo very much for the opportunity to comment on what is going on in Argentina. Here is a short update on what happened on Friday. Regards,

Alejandro

Update on May 4th announcements:

Early in the morning before markets opened the Government made a coordinated series of announcements:

The Central Bank announced another rate hike of 675 bps bringing seven day

REPO rates to 33% (passive) and 47% (active). One day REPO rates rose to 28% (passive) and 57% (active). It also announced that it lowered the upper

limit on foreign assets that banks can hold (forcing them to sell dollars or limiting their future demand) and that it would continue operating on the foreign exchange (spot and futures) if needed.

The Secretary of the Treasury (Ministro de Hacienda) announced that they

lowered the primary fiscal deficit target for 2018 from 3.2% of GDP to 2.7%

of GDP. Spending cuts on public investment were announced.

The peso appreciated and the exchange rate decreased from 23.00 ARS/USD to

21.75 ARS/USD.

... my interest is particularly *piqued* ...

ReplyDeleteThank you for this useful detail from a knowledgeable local observer. Regarding your own comments, I am aware that neither Argentina nor monetary economics are your fields of expertise, but you should be aware that Argentina's "convertibility" system of the 1990s was far from the textbook currency board that many accounts have painted it as. For the short version of why not, see article:

ReplyDeletehttps://object.cato.org/sites/cato.org/files/articles/hanke_feb2008_argentina_currencyboard.pdf

If you want the long version, see this article that I wrote:

https://econjwatch.org/articles/ignorance-and-influence-us-economists-on-argentina-s-depression-of-1998-2002

Interesting post.

ReplyDeleteSo, given that the GOP says "deficits don't matter," and the Donks may be worse, what is the upshot?

My guess is that more taxes on productive behavior is not the answer; that is no more income or payroll taxes.

That leaves property, fuels, sales, pollution, import and Pigou taxes. I see no action to move to those better forms of taxes on the federal level. Income taxes are becoming more easily evaded every year, btw.

Cutting outlays?

We could eliminate the USDA, Commerce Dept, HUD, Education and VA---but where is the political will to do so?

The US runs a global guard service for multi-nationals (but paid for by domestic taxpayers). Is this consistent with bona fide US defense needs?

Russia just cut its military spending by 20%.

https://www.rferl.org/a/russia-despite-ventures-syria-ukraine-cut-military-spending-last-year-most-since-1998-economic-collapse-western-sanctions-recession/29203634.html

The US cannot do the same?

If national debt is the problem that Cochrane has been suggesting, it may be time to move assets out of the US into other currencies or geographies.

Does Cochrane have any suggestions, based on his perspectives?

Government has to have generally accepted utility if central banking is to work. CB money is backed by the delivery of government goods. It is reasonable, and likely, that we elect parties everywhere that don't want to buy the stuff,then your central bank standard goes haywire. A dangerous game given that the internet increasingly offers alternative money standards.

ReplyDeleteRE: "... The fiscal deficit remained high and was financed foreign debt. ... ..."

ReplyDelete• Here is the key line. The essense of the problem. Coupled with the oil price collapse.

The truth is:

• A sovereign (Treasury combined with the Federal Reserve Bank), like the US, that:

a. issues,

b. borrows in, and

c. floats

its own currency, can NEVER run out of cash.

• The sovereign, like the US, can:

a. issue currency to spend and buy anything the economy produces,

b. up to the productive capacity of the economy (adjusted for turnover/velocity),

c. without creating inflation.

I'm with Benjamin Cole. Get your assets out of the US.

ReplyDeleteYesterday a posted a short piece on Argentina on my blog with several charts that may be of interest. http://scottgrannis.blogspot.com/2018/05/argentina-just-got-5-billion-lesson-in.html

ReplyDeleteToday the big news is that Argentina has (surprisingly, given prior statements to the contrary) already begun negotiating a $30 billion credit line with the IMF. The IMF is a four-letter word in Argentina, having dispensed lots of terrible advice over the years, so Macri is either desperate for help or else willing to take big risks to succeed. The stock market has rebounded from its lows, but the peso is approaching 23.

I'm amazed that no one is talking about all the money printing.

These events look particularly funny when viewed through a fiscal theory lens.

ReplyDeleteFirst, the sovereign acts in a way which reduces the expected present value of future primary surpluses; this leads to a temporary increase in inflation which is realized over time due to price stickiness. Then, alarmed by this disturbing development, the central bank raises its policy rate, which ends up making the state of high inflation permanent and at best (with a substantial amount of long term debt) mitigates the initial fiscal shock by a small amount.

There's nothing the central bank can do if everyone believes that the central bank will bail out bondholders whenever the fiscal authority gets into trouble; no amount of playing with nominal interest rates can stop a fiscal devaluation. (Even if the central bank did not commit to this, without monetary frictions to back them up, they still have no ability to stop a fiscal devaluation.) If they just acknowledged this and kept nominal policy rates at a low level, the temporary inflation would disappear and they would be back to hitting their target. Instead, they choose to raise policy rates, almost as if they are trying to perpetuate the inflation they say they want to stop.

A note on foreign exchange reserves: when a central bank holds foreign government bonds, it's effectively the same thing as the government issuing domestic government bonds to buy foreign government bonds. If a company not restricted by financial regulation did this in substantial amounts, their shareholders would ask "can't you find something to do with your money which returns more than ~ %0.5 annually?". When a poor country's central bank hoards US government bonds, it's effectively saying that there's no better public investment opportunity within the country than putting all of this money into US treasuries yielding ~ %0.5 in real terms. The currency is supported by the ability of the government to obtain real revenue, so I can only conclude that foregin exchange reserves are a waste of resources in an emerging market economy with remotely profitable public investment opportunities.

The money printing is a consequence of the interest rate policy - nominal government liabilities have to grow if monetary policy is going to support a high nominal interest rate without help from the fiscal authority, so that's what happens when you try to implement a high interest rate policy. It's not that the central bank is trying to print money, it's that they are being forced to do it because they are trying to keep their policy rate within a high target range.

Is there even any example of a "high interest rate policy" successfully reducing inflation other than the usual one of Volcker? I don't recall hearing any such examples.

IMF to the rescue

ReplyDeleteThe key to the effectiveness of monetary policy is the credibility of the central bank and of the government. Macri started with some credibility but markets were weary of the heavy economic legacy that Cristina Kirchner gave to him -full of time bombs.

ReplyDeleteMacri did not want to call the IMF nor do 'shock therapy' for political reasons: He did not want to appear as the harbinger of hated 'austerity' or give ammunition to the peronist-controlled unions for heavy strikes. So he opted for politically soft gradualism, trusting that his credibility and foreign investment would be enough.

Now it's clear that he overestimated his credibility, particularly as foreign support was mainly political, but not backed by effective infusions of financial flows.

It is not enough to be pro-market in your ideas. If the credibility of your nation is low due to its track record of populism and debt restructuring, and you opt to keep on financing your budget deficit through overt money printing, just a little bit less than the previous government, you are taking big risks.