My proposal to fund the US with perpetuities comes from a paper, here. (Sorry regular readers for the repeated plug.) The rest is standard fiscal theory of the price level, spread over too many papers to give one more plug.

There are three main points. First, inflation is not about money anymore -- the choice of money vs. bonds. Money -- reserves -- pay interest, so reserves are just very short-term government bonds. Inflation is about the the overall demand for government debt. That demand comes from the likelihood of the debt being repaid, and the rate of return people require to hold debt.

Second, if we have inflation, the mechanism will be very much like a run or debt crisis. Our government rolls over very short term debt. Roughly every two years on average, the government must find new lenders to pay off the old lenders. If new lenders sniff trouble they refuse to roll over the debt and we're suddenly in big trouble. This is what happened to Greece. It's what happened to Lehman Bros. In our case, our government can redeem debt with non-interest-paying reserves, resulting in a large inflation rather than an explicit default.

2a, a run is always unpredictable. If you knew there would be a roll-over crisis next year, you would dump your government bonds this year, and the run would be on. There is a whiff of multiple equilibrium too. Our debt is nicely sustainable at 1% interest. If interest rates go up to 5%, we suddenly have north of $1 trillion additional deficits, which are not sustainable. The government is like a family who, buying a home, got the 0.1% adjustable rate mortgage rather than the 1% (government debt prices) fixed rate mortgage because it seemed cheaper. Then rates go up. A lot.

Sure demand is high for US government debt, rates are low, and there is no inflation. But don't count on trends to continue just because they are trends. How long does high demand last? Ask Greece. Ask an airline.

Third, for this reason, I argue the US should quickly move its debt to extremely long maturities. The best are perpetuities -- bonds that pay a fixed coupon forever, and have no principal payment. When the day of surpluses arrives, the government repurchases them at market prices. By replacing 300 ore more separate government bonds with three (fixed rate, floating rate, and indexed perpetuities), treasury markets would be much more liquid. Perpetuities never need to be rolled over. As you can imagine the big dealer banks hate the idea, and then wander off to reasons that make MMT sound like bells of clarity. That they would lose the opportunity to earn the bid/ask spread off the entire stock of US treasury debt as it is rolled over might just contribute.

But we don't have to wait for perpetuities. 30 year bonds would be a good start. 50 year bonds better. The treasury could tomorrow swap floating for fixed payments.

Then we would be like the family that got the 30 year fixed mortgage. Rates go up? We don't care. By funding long, the US could eliminate the possibility of a debt crisis, a rollover crisis, a sharp inflation for a generation.

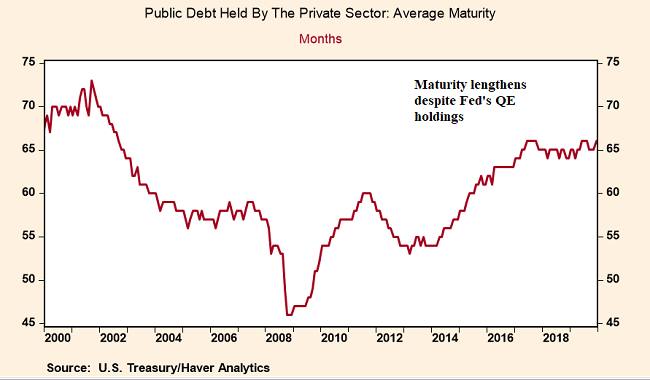

Gavin Davies shows the following graph, congratulating the Treasury for going longer after 2008.

But weighted average maturity is a terrible statistic, and substantially overstates the maturity. It weights only the maturity of the principal, ignoring the coupons. If the Treasury introduced perpetuities, the weighted average maturity would instantly be infinity, which is obvious nonsense. We know how to calculate better numbers -- start with duration, which includes the maturity of the coupons. The Treasury's antiquated accounting is an obstacle to reform.

Well, a rise in rates is hardly likely, you say. Indeed in the same volume as my perpetuities proposal, Robin Greenwood, Sam Hanson, Joshua Rudolph, and Larry Summers advocated an even shorter maturity structure. The ARM is cheaper, and they ran some situations that a rise in interest rates was unlikely given the statistical patterns of recent history.

But past history does not always continue. I buy earthquake insurance in California even though there hasn't been a really big one since 1906. The same statistical approach to risk management blows up regularly. Economists working on climate change often make the insurance argument -- sure, the conditional mean is not a catastrophic impact, but we should take out insurance that it's not much worse than we think.

A debt crisis is like the Spanish Inquisition. Nobody expects it. Alan Blinder, for example, writing in WSJ echoes this conventional wisdom,

First, at least for now, the Fed is buying as many debt securities as the Treasury is selling. On net, the investing public doesn’t have to buy any.Wait a minute, Alan, the public does have to hold the reserves, which are just another form of government debt!

Second, the U.S. borrows in its own currency. Sovereign debt crises almost never arise in such cases.True, but inflations do. Riots, civil wars, pandemics and coups "almost" never arise either, yet we are well advised to pay some attention. And the US has had one big debt crisis in 1972, though we borrow in our own currency and under Bretton Woods the dollar was the reserve currency. Foreigners distrusted the dollar and demanded payment in gold, which we ran out of. (Short version). The UK had several debt/currency/inflation crises.

Third, if the U.S. Treasury starts to supply more bonds than the world’s investors demand, the markets will warn us with higher interest rates and a sagging dollar. No such yellow lights are flashing.Did I mention that nobody expects a run? Flashing yellow lights did not warn Greece, Lehman Bros., or the US.

Here are 10 year rates and inflation through the 1970s and 1980s. 10 year rates never saw inflation ahead of time. They didn't see the decline in inflation even after it happened.

Fourth, interest rates on government debt in several advanced countries—notably but not only Japan—are superlow today even though their national debts are far higher, relative to gross domestic product, than seemed prudent a decade or two ago.So AIG was in worse shape than Lehman.

Fifth, the U.S. public debt topped 100% of GDP at the end of World War II with no adverse consequences. After that peak, we managed to whittle the debt down to only 22% of GDP over the next 28 years or so. To accomplish that feat, we didn’t need to run budget surpluses year after year. We just kept deficits small enough that the debt grew slower than GDP. Which is not that hard if the interest rate remains below the economy’s growth rate—as has been true for years.

Actually, post WWII, after a quick bout of inflation that wiped out some of the real value of debt, the US ran steady primary surpluses until 1975. And had strong supply-side growth in a much less regulated economy. Let's be nice -- "keep deficits small enough" is wisdom widely overlooked around Washington.

"if the if the interest rate remains below the economy’s growth rate—as has been true for years" sounds a lot to me like "if the stock market keeps going up at 7% per year -- as has been true for years."

Yes, I was worried in 2008, and the crisis hasn't happened yet. But the logic of it does not suggest a classic near-term forecast. It could wait 10 or 20 years. We could escape with strong supply side growth, and "deficits small enough" by sensible reforms. But if it came -- doubtless in a deep recession, social unrest, perhaps war, just the sort of times that people doubt America's ability to reform itself and pay off its debt -- it would be an immense disaster.

Locking in 1% interest rates for a generation seems like a no-brainer. While markets are willing to sell us insurance at this rate, take it.

Updates:

1) A colleague writes,

Might the short term debt issuance be a way the government is implicitly committing to not inflate the debt away. Such inflation would be much more painful than say deciding to inflate away debt with a long maturity structure?This is a good point. The short maturity structure is much harder to inflate away. The long maturity structure means in the event of inflation, default, widening credit spreads for the US, etc., the government comes out ahead, and is thus less likely to avoid the event. Seeing the US in effect take a big bet on inflation might also scare markets a bit. It's sort of like showing up at the insurance office with a can of gasoline under one arm. Like swaps, it also raises the counterparty question. If the US issues 30 year bonds, interest rates rise, the bondholders take a huge hit. Will the US really allow that to happen? If the bondholders are big banks, pension funds, and so forth?

I think Merton Miller once suggested that Hong Kong defend a currency peg by writing a huge number of options against it, which would profit if the peg did not fall apart and ruin the country if it did.

2) In my memory of history, I can think of only one and a half times that debt to GDP greater than 100% has ended well for bondholders in the last 1000 years. The UK following the napoleonic wars is the first (funded by perpetuities, by the way). The US after WWII is the half - the inflation of 1945-46, the collapse of Bretton Woods and inflation of the early 1970s also contributed a bit. The UK following WWII was not a success. The UK grew out of the debt -- it started the industrial revolution. So both US and UK successes trace to a surge of supply-side growth, with sober fiscal management -- at least primary surpluses, as above. We have neither going forward. I asked some assembled economic historians for other examples. The US after the civil war came up. That's about it. I welcome other antecedents, especially ones with sclerotic growth and ever expanding deficits.

Let's suppose the Federal government only had the power to issue fixed value floating rate debt, fixed coupon debt, and indexed perpetuities. Under your proposal, what keeps the issuer from only issuing the fixed value floating rate debt? While a type of debt default is avoided, they would fully expose themselves to interest rate risk.

ReplyDeleteFascinating post.

ReplyDeleteI do wonder about the actions of a lone central bank conducting quantitative easing, in a world of globalized asset markets and fungible money.

Global asset markets, including property bonds and equities, are about $400 trillion. The world appears to a generate additional capital every year with additional trillions looking for a home.

In this context, the actions of the Federal Reserve, with a few trillion dollars of quantitative easing, appear rather small. It does not seem "fair," but I suspect the Federal Reserve could pay off or monetize the entire US national debt without consequence.

The Swiss National Bank has acquired assets, through quantitative easing, about four times Swiss national debt.

I actually prefer a much smaller federal budget, including much smaller military and social welfare outlays, and for any stimulus to come in the form of hefty tax cuts.

But with globalized asset markets and the fungibility of money, the outlook for demand for US government debt appears very long-term. Curiously, some QE seems to make the viability of remaining outstanding US bonds to be even higher.

Add on: The Fed does not have to pay interest on excess reserves, and many say it should not. The IOER strikes me as a sop to the banking industry, the most important client of the Fed. If banks did not receive IOER, so what? Would lending become too-expansionary? Hard to imagine such a concern.

ReplyDeleteVery interesting post as always! I think a more recent example (even if not as long as the UK after Napoleonic wars) is Belgium.

ReplyDeleteThey managed twice to get their debt under 100% of GDP: from around 130% to 90% between 1984 and 2006, and then from 110% to 99% between 2014 and 2019, with low inflation.

However, it seems closer to the English case, where the EMS and then the Euro plays the role of the gold standard to anchor expectation, coupled with a sharp reduction in the fiscal deficit to make this anchor credible (seems taken from Sargent's Stopping moderate inflations: the methods of Poincaré and Thatcher)

But still interesting that this supply side growth strategy remains possible!

Nominal rates rising depends on some assumption about monetary policy though.

ReplyDeleteSay there's some big positive shock to real rates that devalues future surpluses and the Fed has credible forward guidance.

If the maturity structure is long, the Fed has to choose between keeping rates steady, allowing government liabilities to be revalued in light of higher discount rates, or it can raise rates, which will temporarily lower inflation by forcing long bond holders to take losses.

In both cases bondholders are screwed. With the first option we get the social cost of high inflation.

With the second option bondholders eat losses. But bondholders are now "systemically important", so if they eat losses, the government has to step in and guarantee all of their liabilities worsening the original problem.

The first option honestly sounds better. the government's creditors are forced to take haircuts vis a vis inflation, but they won't go bankrupt and there will be no financial disaster.

While i agree, i'm not sure this actually solves too much. If the world began to distrust the USD, it would sell it's 30y treasuries well in advance of any actual inflation. The Fed would surely be concerned by the wealth effect on spending given the size of the treasury market. It would then begin purchasing Treasuries in large quantities given the absence of current inflation. At that point you've accomplished little.

ReplyDeletePerhaps its best for all debt to be inflation-linked so inflation is off the table as a fiscal solution. Given the size of quasi-inflation-linked spending (health, military, tips, social security), inflation may already be off the table as a fiscal solution.

"In our case, our government can redeem debt with non-interest-paying reserves, resulting in a large inflation rather than an explicit default." Could you explain what mechanism creates inflation? I would be worried about spike in real rates, collapse of velocity, prolonged recession.

ReplyDeleteThe U.S. is not Greece, or Lehman Bros -- you make assumptions that are beyond reality, e.g. a run on avoiding our debt. The fact is our debt is in demand -- and that depends on our rate of productivity, and how we compare with other avenues of investment. It has been going in our favor for many decades -- and that is with rates of growth that have been increasing at decreasing rates. We need to get back to higher rates of growth.

ReplyDeleteGetting back to higher rates of growth would not only be better for our economy and our society, it would help us in pursuing our national security strategy of spreading democratic values in a world where we have adversaries, as well as a few allies, who are authoritarian in nature.

Vic, fair point but Greece is a cautionary tale. Greece's population is about 11 million. Insufficient tax revenue and low rates of productivity were a problem save for the fact that she was a Euro-zone member. She borrowed on the cheap and ran deficits till she defaulted. Bond rating services rated her debt as junk. In 2015, Greece was asking Wall street to lend money for 2 years at 20%. There were very few takers.

DeleteJohn, excellent post.

ReplyDeleteIt reminds me what we have done in Israel last weeks: https://en.globes.co.il/en/article-israeli-govt-completes-largest-ever-bonds-issue-1001324135

Best,

Jonathan

Why not zero coupon perpetuals? Otherwise known as Federal Reserve Notes. There is something like a Trillion Dollars worth of $100 bills in circulation, mostly outside of the country.

ReplyDeleteIf we really wanted to lean into the concept, the Fed could issue higher denominations. In the past it has issued notes up to $10,000. https://en.wikipedia.org/wiki/Large_denominations_of_United_States_currency.

I am sure that 1s and 10s would be extremely popular. Using 10s you could put very meaningful amounts of cash into an attache case. The busybodies in the DEA and the counter terrorism agencies would hate it. But, sometimes you just have do what you have to do.

With countries around the world increasing their debt and if most if not all go beyond 100% debt/GDP is the concern not in anyway mitigated?

ReplyDeleteI like this idea. A lot. One caveat. Current 30 year rates are like 1.50%, not 1%. And that is, IMO, influenced by the small supply (couple trillion?). If we start pushing all debt to 30 years and more (which we should), those rates will almost certainly rise. How far? I don't know.

ReplyDeleteYou might be interested in a new paper by Australian macroeconomist Tony Makin released by the Centre for Independent Studies, on "A Fiscal Vaccine for Covid-19," demolishing our government's economic response and suggesting a non-Keynesian alternative. Tony and I were amongst the few to argue against the Rudd government's disastrous response to the GFC - still impacting us adversely - before it was implemented. (Sadly, we were ignored.)

ReplyDeleteAnother way to look at perpetuities is that they are interest only (I-O) bonds that never pay back the principal.

ReplyDeleteIf we are going to issue I-Os we should issue their opposite principal only bonds (p-o). Actually, Treasury issues everything under 1 year as principal only. They do not bear a coupon. The great thing about P-Os is that the P-Os with the same maturity date are the same and should ever be "off-run"

A sufficient supply of perpetuities and P-Os should give us an excellent reading of what term rates are, should trade at minimal spreads, and should stretch out the Treasuries obligations until well in the future.

Comparing Post WWII GDP growth to current GDP growth is a classic mistake. Because of the Baby Boom and entrance of women into the workforce, the population expanded dramatically, but GDP per-capita did not increase nearly as much.

ReplyDeleteBorrowing from future generations is like a ponzi scheme. As long as the population is growing, you can borrow more than you commit.

But once the population stops growing, as it has, borrowing from future generations is just legal embezzlement of public funds, and essentially slavery, because we're making future generations work harder for the same after-tax income, in order to pay for our expenses today.

OK, "slavery" not technically, because the future generations could always renounce citizenship and leave. But there's no question than any country that takes from its future generations rather than investing in them will decline.

Money is a confidence game. If one could make general purchases using wooden nickels, wooden nickels would be money. In the 18th century, bills of exchange substituted for specie as money until governments outlawed bills of exchange for that purpose. If you could exchange bus tokens or milk tokens for a shave and a shine, bus tokens and milk tokens would be money.

ReplyDeleteReserves are not money--you can't use them to pay for taxi fare to get across town, and no one would accept them for that purpose.

Inflation is not dependent on government debt obligations. Witness the decline in purchasing power of gold during the Kingdom of Spain's heyday when it controlled the gold deposits of South America and imported gold in vast quantities into Iberia. Adam Smith remarked on it, using the "corn price of gold" to compare inflation of money (gold) in Spain to that in England--it took more gold to buy a bushel of corn in Spain than it did in England at the time. The same would be true of bus tokens--issue too many and the bus token will buy fewer real goods ("corn", for example).

Your paper discourses on perpetuities. Your blog post mentions Bank of England perpetuities, "Consuls". Consols were marketable because the purchasers were confident that the purchasing power of the annual income from holding a Consul would not diminish. A Consul is desirable because it is backed by an implicit guarantee of conversion into specie at the option of the holder. No such guarantee would implicitly back a U.S. perpetuity issue.

The only reason long bonds are marketable is the existence of long term liabilities contracted for in nominal dollars. One can construct a portfolio, in theory, in which holdings of long term treasury bonds fully offset contractual liabilities denominated in nominal dollars. A perpetuity would be unlikely to fulfill this role adequately because the future value is uncertain (V(t) = C/r(t), with r(t) stochastic, possibly with a variance directly proportional to time).

A perpetual bond with constant dollar coupon payments would approximate a Consul, if there is confidence that the government would not renege on the contract. But, as with the Bretton Woods agreement when Nixon took the USD off the gold standard by suspending convertibility, so too would a future government renege on the perpetuity contract because of increasing debt service costs expressed in then nominal (budget) dollars.

A perpetuity having an exponentially diminishing coupon rate with time would be worthless, for all practical purposes.

Issuing fifty-year maturity nominal dollar coupon bonds is not equivalent to a one-time "set-and-forget" mortgage loan for a family of five. The government that runs annual deficits needs to return to the financial markets yearly--its issued and outstanding debt rises geometrically as time runs. For the first fifty years, all is well, but in the fifty-first year the scheme collapses. It faces a continuum of balloon payments from there to infinity. Even if it does run annual surpluses it nevertheless faces a period during which its finances will shake market confidence. Do you trust your congressman not to become profligate with the public finances once she's spent time in D.C.? I certainly don't.

"Money -- reserves -- pay interest, so reserves are just very short-term government bonds". How are reserved "short term" as they never redeem for anything of intrinsic value.

ReplyDeleteThey have value only because other banks accept that they have value. Their value is due to their liquidity and a bit of interest and it's ability to redeem liabilities to the government or to banks for debts. Reserves are much like bank notes whose value is 100% based on its liquidity and it's ability to redeem liabilities to the government for tax or to banks for debts. Bank notes are clearly perpetual instruments so surely so are reserves.