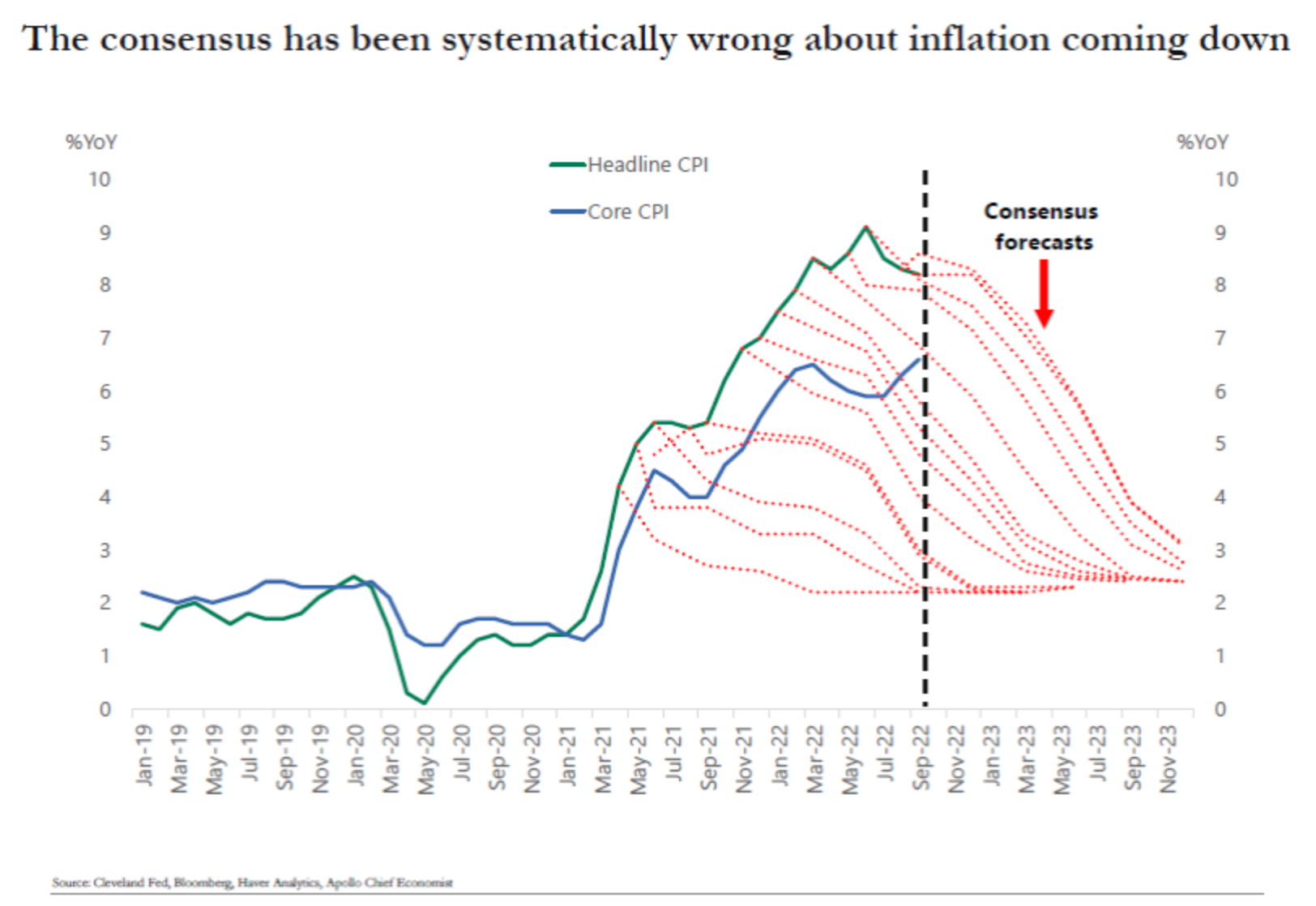

Inflation will be coming down over the coming quarters. This is what the Fed is predicting, that is what the consensus is expecting, and that is what we are predicting. The problem is that this has been the forecast ever since inflation started going up in April 2021, see chart below. Given how systematically wrong inflation forecasts have been over the past 18 months, there are good reasons to be cautious about the current forecast.

It is also how market expectations have evolved. Is inflation inherently unpredictable? Are we collectively in thrall of the same wrong model? Does "expectation" mean the same thing in models and surveys? Are market risk premiums really important?

Apparently inflation rates are unpredictable and may follow a random walk. Maybe existing models fail to explain inflation and market risk premiums. We may need to find the models that have better predictive power

ReplyDeleteIs there a way to check whether consumers have had more accurate inflationary expectations than "experts" this past year? I bet they have. The experts are too partisan.

ReplyDeletehttps://data.sca.isr.umich.edu/fetchdoc.php?docid=70947

DeleteI should add that expert partisanship is "sincere" partisanship. That would explain why Wall Street investors have blown it so badly: they just didn't want to believe Biden's spending would cause inflation.

ReplyDeleteThis is one case where it might be necessary to consider two items that are left out of the inflation debate: 1) money supply and 2) levels vs. growth rates. The level of the money supply rose about 30% in one year (Divisia M4 growth was most recently at 2.5% growth). The price level should jump by a proportional amount but it takes time for the price level to catch up.

ReplyDeleteWhat, pray tell, is the, or even a, model?

ReplyDeleteThe Wall Street Journal Economic Forecasting Survey of 66 economists between October 7th to 11th, 2022 provided an average (sample mean) for the year-over-year change in CPI over the next three years, as follows:

ReplyDeleteDec/'22, Jun/'23, Dec/'23, Jun/'24, Dec/'24, Jun/'25, Dec/'25

7.18%, 4.12%, 3.25%, 2.71%, 2.42%, 2.33%, 2.25%

Closing Yield, 10-Year Treasury notes (sample mean) on:

12/31/'22 6/30/'23 12/31/'23 6/30/'24 12/31/'24 6/30/'25 12/31/'25

3.84% 3.68% 3.45% 3.31% 3.19% 3.21% 3.20%

Midpoint of the range (sample mean) for the Federal Funds Rate on:

12/31/'22 6/30/'23 12/31/'23 6/30/'24 12/31/'24 6/30/'25 12/31/'25

4.267%, 4.551%, 4.228%, 3.645%, 3.102%, 2.940%, 2.828%

These forecasts may be internally consistent (in the mean sample), but inaccurate in fact. It is noteworthy that the sample means indicate that the yield curve will have inverted by the end of 2022. And, furthermore, that the yield curve inversion will continue through to at least June of 2024, by which time the mean estimate of the CPI year/year change will have declined to 2.71% (annual rate). This is likely to be optimistic. Inflation will be more persistent (stickier) than the forecasters (on average) predict. The Fed Funds Rate will rise higher than sample mean prediction.

The blog post asks four questions:

ReplyDelete(a) Is inflation inherently unpredictable?

(b) Are we collectively in thrall of the same wrong model?

(c) Does "expectation" mean the same thing in models and surveys?

(d) Are market risk premiums really important?

I offer the following thoughts in response:

If the answer to question (a) is 'yes', i.e., inflation is inherently unpredictable, then the answer to question (b) is 'probably yes'--we are in thrall to the wrong model.

The answer to the third question, question (c), is 'negative', i.e., "expectation" in theory differs from "expectation" in forecasts and the term is used differently in different contexts. In theoretical models, "expectation" means mathematical expectation. In forecasting, especially in predictive forecasting, "expectation" means a point forecast, e.g., "consensus estimate" of CPI change yr/yr for December 2024 is 2.42% (sample mean of 66 economists' forecasts polled from October 7th - 11th of 2022). The respective "expectations" are used for different purposes.

The fourth question, question (d), appears to be straight from out of left-field. Risk premiums are idiosyncratic, i.e., it will depend on the specifics of the risk or hazard under consideration. A risk premium is a price-adder placed on a contract or security by the underwriter or counter-party. Except to the extent that the contract is not priced in the nominal currency value (or numeraire), inflation may be taken into the determination of the price independently of the risk premium quanta.

"Inherently unpredictable", some notable uses of the term.

DeleteClimate Change:

"Climate models might be improving but they will never be able to tell us exactly what to expect. That's the conclusion of experts from the University of Washington, Seattle, who have set out to prove that predicting the exact level of climate change is by its very nature an uncertain science." -- Hopkin, M., "Climate sensitivity 'inherently unpredictable'". Nature (2007). https://doi.org/10.1038/news.2007.198

https://www.nature.com/articles/news.2007.198

Predicting the unpredictable:

"Time series forecasting is of fundamental importance for a variety of domains including the prediction of earthquakes, financial market prediction and the prediction of epileptic seizures. We present an original approach that brings a novel perspective to the field of long-term time series forecasting. Nonlinear properties of a time series are evaluated and used for long-term predictions. We used financial time series, medical time series and climate time series to evaluate our method. The results we obtained show that the long-term prediction of complex nonlinear time series is no longer unrealistic. "

Golestani, A., Gras, R. Can we predict the unpredictable?. Sci Rep 4, 6834 (2014). https://doi.org/10.1038/srep06834

https://www.nature.com/articles/srep06834

The authors, from the Univ. of Waterloo, Waterloo, Ontario, describe an extrapolation method for predicting future values of a time series. The method is not so much a prediction machine as a modelling algorithm. On predicting DJIA index values, the method outperforms ARIMA, GARCH, and VAR methods. But the 'predictions' are neither right-on-the-money, nor capable of predicting a change in underlying factors that determine the time series values, as shown in charts of the DJIA with the prediction values superimposed over the actual index values as time goes along.

"Inherently unpredictable" is a measure of the complexity of a physical phenomenon. The exact number of alpha particles leaving a radioactive source of alpha particles is "inherently unpredictable" in any time interval of any finite length, but on average we may say that the number will lie between N.min and N.max, P percent of the time, with a confidence level of L. Likewise, in engineering reliability studies, we can say that the number of failures of a machine component (say a rocket motor) is between M.min and M.max, R percent of the trials, with confidence level H. We cannot predict the future event count with exactitude, but we can predict a range of outcomes based on our understanding of the underlying phenomenon based on experience and theory.

Economics is concerned with social phenomenon. It is an inherently inexact 'science', largely because of the complexity of the phenomenon and the scope of variation in the interactions of different objects that comprise the system covered by the practitioners.

Is inflation "inherently unpredictable"? The answer is "affirmative, almost surely", given the complexity of the phenomena that influence and determine the level of a price index. Is "inherently unpredictable" fatal to the work of the economist? I would venture the answer is "no, it isn't", for the same reason that for physicists and engineers the underlying complexity of the phenomena of radioisotope decay and rocket motor failure do not deter the physicist or the engineer from designing systems that are practicable in managing systems subject to those phenomena. Venture on!

I’m not an economist, but I’m interested. A while back I looked for papers on the accuracy of economic forecasts and found a few. The graphs all looked suspiciously like the one in this article.

ReplyDelete"Excess Savings during the COVID-19 Pandemic", Aditya Aladangady, David Cho, Laura Feiveson, and Eugenio Pinto, FEDS Notes, Oct. 21, 2022.

ReplyDeleteAccessible URL:

https://www.federalreserve.gov/econres/notes/feds-notes/excess-savings-during-the-covid-19-pandemic-20221021.html?mod=djemRTE_h

The authors estimate household savings relative to a baseline trend, and determine the "excess savings" over the baseline trend for U.S. households by population quartile. The authors note that retirees on Social Security make up 1/3 of the households within the lowest quartile, and that the non-retiree 2/3rds fraction of that quartile likely has lower or nil excess savings.

The authors break down the 2020-21 stimulus components by type and estimate the amount of stimulus provided by each type. Income tax receipts by governments provide an offset of roughly $745 billion, through 2022:Q2.

The graphics provided with the report will prove of interest to those who wish to understand the impact of the stimulus payments and transfers during the pandemic period. The extensive footnotes provide important explanatory information, both as to method and uncertainty, as well as adding granularity where justified to improve readers’ understanding of the study and its results.

The authors do not answer the implied question: "How will this picture of 'excess savings' affect the FOMC's tightening of monetary policy, going forward?" Will the FOMC members decide to target 'excess savings' for reduction, just as they have targeted 'job openings', to justify the FOMC's policy interest rate hikes? The authors note that the 'excess savings' will act as a buffer to lessen the severity of a FED-induced recession arising from the FOMC's policy to reduce the rate of inflation from its current level to the FOMC's preferred target rate of 2% +/- 100 b.p. Is this a license to hike the policy interest rate without constraint? If so, then we can expect that the bottom quartile and the lower half of the next to bottom quartile will be adversely affected more that the highest and second highest income quartiles. Does this factor at all in the FOMC's 'calculus'?

Changes in prices should always be expected to be toward the market efficient price. There is no equilibirum in that change, as it depends on the difference between current market prices and whatever the efficient equilibirum is.

ReplyDeleteThe mistake economists are making is trying to figure out what the rate is without anchoring it to what the price should be.

To figure out what prices should be, just poll real-estate investors on their actions and whether their conditions for buying a place have gone up or down. Investors have skin in the game.

Does anyone have the link to the original document where this chart came from?

ReplyDelete