The Social Security Trust fund is set to run out in a few years. Who cares? Is the total US Federal debt $31,456,554,630,496.28, including Treasury debt held by the Social Security trust fund and other agencies? or is it "only" $24,629,050,125,670.81 held by the public? (Source.)

I've been mulling these questions over, prodded by conversations with some colleagues.

The "trust fund" exists because for a while, Social Security taxes were larger than Social Security payments. Social Security used the extras to buy Treasury debt. Now there are fewer workers, more retirees and more generous benefits, so Social Security taxes are smaller than payments. Social Security sells off its "trust fund." And it seems we're in trouble when the "trust fund" runs out.

But that's not how it works at all. Treasury debt is not an asset like a stock or bond, or Uncle Scrooge's pool of gold coins. Treasury debt is a claim against future income taxes. Cashing in Treasury debt just means paying for benefits with income taxes.

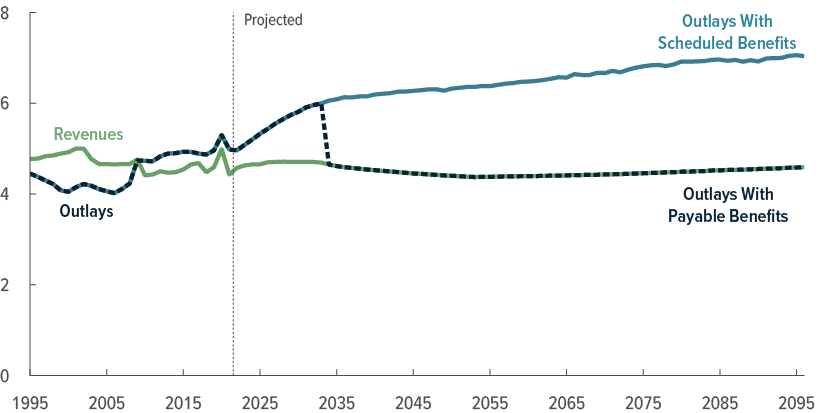

The ups and downs of the trust fund just reflect a change in how we finance spending. While payroll taxes > social security spending, which was the case until 2007, then payroll taxes are financing other spending. When payroll taxes < social security spending, then income taxes or increases in debt are financing social security spending, which (graph below) was the case after 2008.* The trust fund just adds up this change over time. But exhausting the trust fund is, in this view, really irrelevant.

|

| source: CBO |

That doesn't mean we can all go to sleep, for two reasons. First, when payroll taxes < Social Security outlays, and the trust fund is winding down, then income taxes or additional public debt must finance the shortfall. The government has to spend less on other things, raise income tax receipts, or borrow which means raising future taxes. And, per the graph, the numbers are not small. 1% of GDP is $230 billion. The extra strain on income taxes, other spending, or debt, happens right now, when the trust fund is positive but decreasing.

Zero matters only because by law, when the trust fund goes to zero, Social Security payments must be automatically cut to match Social Security taxes. That's the sudden drop in the graph. The program was set up as if the trust fund were buying stocks and bonds, real assets, and would not lay claim on income tax revenues. But it was not; social security taxes were used to cover other spending, and now income taxes must start to pay social security benefits.

What happens when the trust fund runs out, then? Congress has a choice: automatically cut benefits, as shown, or change the law so that the government can pay Social Security benefits from income taxes, or, more realistically, by issuing ever more debt, until the bond vigilantes come. (Or raise payroll taxes, or reform the whole mess.) I bet on change the law.

So what's the right measure of debt? It's conventional to look only at debt in public hands. But there is a case to look at the total debt, i.e. including the trust funds. Those are the total claims against the income tax. Looking at it this way, however, one could also go on and count unfunded future social security benefits as a debt -- the present value of the difference between the two lines above, which leads to immense numbers, per Larry Kotlikoff.

I have usually not considered the present value of unfunded promises as "debt," because Congress can change the payments at any time. Changing debt repayment to the public is a default, with financial and legal consequences; changing social security benefits is legislation. You can't sell your future social security benefits as you can sell your treasury debt. The trust fund is half way on this scale. What would be the consequence of a haircut or rescheduling of trust fund debt? Would that trigger something like cross-default clauses in corporate debt? I don't know. The event is unlikely anyway. The left pocket defaulting on the right pocket doesn't help pay the bills. The trust fund is certainly unlikely to run, and its debt is not used as collateral in financial transactions. As a somewhat meaningless accounting identity, it's a lot less "debt" than the debt in public hands.

I think this all goes to remind us that paying off the existing debt is not the US central fiscal problem. The central problem is vast unfunded future promises. Defaulting or inflating away current debt does nothing to fund those promises.

I look forward to comments on this one, especialy if there are standard views on these apparently simple questions that I'm not aware of.

*In the end,

payroll taxes + income & other taxes + increase in public debt = Social Security spending + other spending.

The trust fund nets out.

You might want to get away from accounting measures altogether, and just look at the allocation of real output between workers and retirees. Compare the path of output/worker to (benefits/retiree)(retirees/worker). Including Medicare, benefits/retiree are going up. Retirees/worker are going up because of demographics--Baby Boom bulge, longer life expectancy, smaller population growth, declining labor force participation. What does the path of consumption/worker look like? Maybe retirees give back some of their benefits via intergenerational transfers. But workers who do not receive transfers are going to have growth in per capita consumption that is low and possibly negative.

ReplyDeleteWhat do we not have enough of?

DeleteYour analysis that the "trust fund" is irrelevant is of course true. It is simply an accounting gimmick along the lines of putting your money in different jars - one for rent, one for food and so on. Money is fungible and creating artificial "accounts" is little more than political gimmickry. As you point out, however, the exhaustion of the trust fund does say something meaningful about US demographics and our ability to continue to fund retirement benefits for everyone over the age of 65. At current benefit levels, that is simply not feasible given the demographics and the economics. Most people forget that social security was adopted after the Depression for the purpose of ending poverty among the elderly. It was never designed as a government retirement program. Means testing social security (perhaps based on lifetime average income levels to avoid gaming) would restore social security to achieve its original purpose without bankrupting future generations.

ReplyDeleteWhat do we not have enough of to "fund" the obligations?

DeleteIf you believe that taxes on output, such as income taxes, reduce output, then you could argue we have over promised "real" benefits to retirees. So the answer to your question is the pie is not big enough and is not growing fast enough to provide the promised benefits for retirees and not over burden the working age population. I would be interested in hearing if raising taxes on corporate profits seems like the most likely solution to helping fill the shortfall

DeleteSo, what do we not have enough of?

DeleteI wrote a paper on the coming shortfall in social security in my high school economics class in 1976 - 47 years ago! So why hasn't the government fixed this before now?

ReplyDeleteHave you considered that perhaps it's because its not a problem?

DeleteA little adjustment to what happens when the trust fund is exhausted. This is a conflict of two laws - by law, entitlements continue until changed, and by law, you can’t use money from other sources.

ReplyDeleteCongress must amend Social Security to cut benefits, otherwise they are still owed, perhaps to be paid in arrears. So, without action some benefits must, by law, be delayed.

Congress can either fund the funds or eliminate the "trusts" altogether and simply pay the obligations. Not a problem.

DeleteExactly. The Reason libertarians keep talking about the automatic 25% cut that SS is going to have in 2030 +/- a few years but in a world where the Republicans yelled at Biden when he claimed that they wanted to cut SS it is vanishingly unlikely that that course is a realistic option. The trillion dollar coin is more possible than the US government cutting Grandma’s check by a quarter all at once.

ReplyDeleteSo they're raising taxes then? Or just adding to the debt which is already at stratospheric levels from the past 3 years?

DeleteThe US government debt is not a problem in any way shape or form. In fact, it can be repaid tomorrow without a negative repercussion. That would simply involve replacing government bonds with deposits at the Federal Reserve Bank with similar interest and maturities. The similar or even better risk/reward terms assure no change in investor savings/spending preference or desire to hold dollars. Not recommending this course of action, just pointing out that it is possible.

DeleteWell written and as a liberal it justifies a more progressive tax system.

ReplyDeleteI ignore the "Intragovernmental Holdings" because this is just debt that the gov't owes itself. This debt is not economically meaningful. It just overstates both assets and debt of the consolidated gov't entity. The assets of the trust funds and debt owed to them by the "general fund" exactly offset.

ReplyDeleteIf the gov't decided to just eliminate the intragovernmental holdings and get rid of the trust funds, it would change nothing, except for the bookkeeping. The gov't would still need to collect cash via taxes and borrowing to pay benefits.

The only economically meaningful aspect of the trust funds is the prohibition against running a deficit after they are depleted. This could be fixed with bookkeeping entries to the general fund and the trust funds. The general fund could debit net assets and credit debt owed to the trust funds, and the trust funds could debit assets and credit net assets.

Problem solved! Okay, not really, because you still have to deal with the fact that these entitlement programs are running deficits that will get much larger.

Where does money come from?

DeleteA few years ago, I ran across a couple pieces I found useful in thinking about the financial irrelevancy of the Social Security Trust Fund:

ReplyDeletehttp://fee.org/freeman/a-college-fund-on-the-social-security-model/

http://cafehayek.com/2015/08/quotation-of-the-day-1445.html

"Congress has a choice: automatically cut benefits, as shown, or change the law so that the government can pay Social Security benefits from income taxes, or, more realistically, by issuing ever more debt, until the bond vigilantes come."

ReplyDeleteCongress can allow the Fed (your bond vigilantes) to do it's job and this will rise:

https://fred.stlouisfed.org/series/L313071A027NBEA

Or Congress can convert the rest of it's financing needs to be more like Social Security (non-guaranteed income) - this:

https://musingsandrumblings.blogspot.com/2019/09/the-case-for-equity-sold-by-u.html

"In the end, payroll taxes + income taxes + increase in public debt = Social Security spending + other spending"

ReplyDeleteNope, not even close.

https://fred.stlouisfed.org/series/W006RC1Q027SBEA

Total tax receipts (3rd Qtr - 2022) - $3.2 Trillion

https://fred.stlouisfed.org/series/FGRECPT

Total federal receipts (3rd Qtr - 2022) - $5.0 Trillion

You are missing about $1.8 Trillion in federal receipts from your equation.

That is simply the BEA separating out "Contributions for government social insurance." Prof Cochrane is a bit loose with his terminology, but the idea is correct. (As I understand it, technically speaking payroll taxes include withholding taxes on income, so there would be some double-counting with income taxes in the equation as written?)

DeleteAlso,

DeletePayroll taxes + income taxes must always be greater than interest payments on the debt (part of that other spending that John references).

Paying interest on the debt with new debt issuance is Ponzi finance and is illegal in the U.S. (even for the federal government)

John apparently is referring to FICA taxes when he speaks of 'payroll taxes'. BEA's 'contributions for government social insurance' include taxes on social security income of some social security recipients (depending on the taxpayer's taxable income that is above a dollar threshold set under the income tax code).

Delete"Congress has a choice: automatically cut benefits, as shown, or change the law so that the government can pay Social Security benefits from income taxes, or, more realistically, by issuing ever more debt, until the bond vigilantes come."

ReplyDeleteCongress has a lot of choices. Because Social Security benefits are indexed to inflation, they could allow prices to fall and by extension nominal Social Security benefits would fall as well.

When assessing sovereign debt crisis risk, the trust fund debt should be included because that debt has to be paid unless social security is massively curtailed – a politically unacceptable option. In other words, trust fund debt should be included because it is senior to other government debt. For example, even after suffering severe debt crises, the European PIIGS only modestly curtailed their versions of social security. See my year-end 2016 letter: https://www.hcapital.llc/public-letters

ReplyDeleteI agree that suggests some unfunded social security benefits should also be included. However I generally do not do that because it complicates historical and cross-country comparisons.

The European PIIGS are not monetary sovereigns and more comparable to say Florida rather than the US. A sovereign (Treasury combined with the Federal Reserve Bank), like the US, that:

Deletea. issues,

b. borrows in, and

c. floats

its own currency - and can feed itself - can NEVER run out of cash.

It is a misnomer to call it a trust fund given the traditional meaning of a trust fund. Excess funds in SS are loaned to gen gov account and in return receive back non marketable Treasury instruments- special type of T instrument ..

ReplyDeleteGood question then regarding overall indebtedness of USG as reported and whether it includes these special non marketable T obligations owed to SS. Hard not to include it in overall USG debt and yes issues down the road in a great many respects regarding it.

The cure for SS and for all such welfare programs, since they are all being funded out of tax revenues and debt already, no matter how those tax receipts are being parsed, ghosted, and spun, is means testing. In the end all of them will answer the bond vigilantes with those two words: "means testing". Understand: everyone will for a certainty be sent all of the money they've been promised, but just because you were given cash does not mean you'll be allowed to keep it. There is no other politically viable answer.

ReplyDeleteMeans test? You made plenty your time whole life to have a good retirement. What? You spent all the money? No social security for you then. Said no politician ever. It’s the same problem with medical insurance. Until society allows a reckoning for bad behavior (which is almost impossible to discriminate from bad luck) everyone knows the safety net is there and acts accordingly.

DeleteI have said many times that the cap on taxation of payroll of people making more than $160,200 (in 2023) should be eliminated.

ReplyDeleteThe Democrats proposed removing the cap for people making more than $400,000 showing you who their constituents are. but, to the devil with them.

Incentive effects? I don't care.Those people are more Democrat voters than the poorest ghetto. They have asked for it and they deserve it.

Other changes. In 2027, the normal retirement age will be set at 67 for people born in 1960. We should continue to increase it until it is 70. the minimum retirement age should be increased from 62 to 65 over the same time frame.

The era of incentive effects is over. The budget will run out of control if the debt remains over the GDP and interest rates exceed growth rates. Both of those conditions are closing in us. So is Cold War with China. We also need to double the defense budget.

Sorry folks, the party is over; the punch bowl is empty. The politics of the 1980s will never come back. life is hard. life is earnest.

Lifting the cap has many problems, first that benefits paid out are linked to contributions, so that has to change. It means a full 12%+ rise in tax rate for high cash earners, on top of 40% fed and 12% state rates plus other taxes in places like NY and CA. This will create massive distortions to avoid cash compensation. Changing all this means a huge change to a full redistribution welfare scheme that makes Europe look cheap, and create large disincentive effects, and by calcs eg by Riedl will not cover the shortfall. It has to involve taxes on the breadth of the middle class

Delete

Delete"benefits paid out are linked to contributions, so that has to change."

Easy peasy. Cap benefits at any level that makes you happy and is politically feasible.

Conceptually, it is not hard. politically?

"It means a full 12%+ rise in tax rate for high cash earners, on top of 40% fed and 12% state rates plus other taxes in places like NY and CA."

There is no group in the United States that I have less sympathy for than the high earners of New York and California. They have become the bulwark of the Democrat Party. Their favorite politicians like Warren and Sanders continually hector us that the rich are not paying their fair share. Okay then, let the rich pay more, a lot more. They have worked for it. They have earned it. And they should get it. Hard. Until it hurts.

"This will create massive distortions to avoid cash compensation."

We have been here before. Remember that until the late 1980s, top marginal rates were well above where they have been since then. The IRS has lots of tools for dealing with non-cash compensation. It will be fun to see them trotted out again.

"Changing all this means a huge change to a full redistribution welfare scheme that makes Europe look cheap"

What makes you think we are not there? I think Phil Graham's new book goes into this in more depth, but the US is doing massive redistribution. It is just being done by a chaotic assemblage of miscellaneous uncoordinated programs. And, don't forget the massive programs like public schools that are in kind redistributions.

"and create large disincentive effects"

Yup. But, as I wrote above: "The era of incentive effects is over. Sorry folks, the party is over; the punch bowl is empty. The politics of the 1980s will never come back. life is hard. life is earnest."

We are in a real pickle, we have spent the money already our choices are raise taxes, grow out of the problem, or suffer hyperinflation.

I am very skeptical about the prospects for growth. We have spent much of the last 50 years creating anti-growth polices and agencies. How much has the EPA cost us? The FDA is a tremendous drag on the economy. And, don't get me started about the federal courts. I have often written that we will see no progress until the last lawyer is strangled with the entrails of the last environmentalist.

Nor do I believe there is technological magic up anybody's sleeve. Read "Tech Progress Is Slowing Down: Despite utopian hopes, the exponential growth of computer technology can’t be replicated in other key areas" by Vaclav Smil • https://www.wsj.com/articles/tech-progress-is-slowing-down-b7fcaee0

Further we have a demographic problem in common with other advanced economies. Our total fertility rate has dropped well under 2. Immigration could help, but importing Central American peasants who are illiterate in 3 languages is a very slow fix.

As for hyperinflation. I urge you to read "The World of Yesterday: Memories of a European" by Stefan Zweig. https://www.amazon.com/World-Yesterday-Stefan-Zweig/dp/0803226616 His description of the Post-WWI hyperinflation is hair raising. Honestly, you do not want to go there. When Zweig finished writing the book, he committed suicide.

There you have it. Taxes, growth, or hyperinflation. The last is a horror. The middle term is an opium dream. So taxes it must be.

"and by calcs eg by Riedl will not cover the shortfall. It has to involve taxes on the breadth of the middle class"

Yes, we need taxes. Lots of taxes. At the very least a VAT. If global warming is a real problem we should impose a carbon tax and a carbon tariff. And, no talk of rebates. Extra money must go to rebuild the Navy. Like I said we are in real trouble.

You ask: “So what's the right measure of debt?” The correct answer is of course 42! Or for those who are not familiar with Douglas Adams' work, any apparent ambiguity in the answer is really due to ambiguity in the question.

ReplyDeleteOf course we all knew the answer was 42 already, but we're having trouble getting the question right.

DeleteAm unrelated to the author in any way, and a good book by Cogen is The Cost of Good Intentions.

ReplyDeleteI agree entirely with the economic argument that the Trust Fund nets out in the public spending equation.

ReplyDeleteI think of the assets held by pension funds, and the corresponding liabilities for the tax payers in terms of government bonds, is as a form of mental accounting of the present value of the promises that we have made to others and the future. In that sense the "debt crisis" means that we have made promises that will be very expensive to honor. We may not be as rich as we believe, and somebody will be disappointed.

All liabilities are assets to somebody. If you consolidate far enough, you eliminate all debt and are left with only assets and equity.

DeleteThe Old Age & Survivors Insurance ("OASI") Trust Fund ended 2022 with a balance of $2.7119 trillion (source: https://www.ssa.gov/oact/STATS/table4a1.html ).

ReplyDeleteFederal Intragovernmental Holdings ended 2022 with a balance of $6.9021 trillion (source: https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/debt-to-the-penny ).

The second source cited allows the reader to view the federal government indebtedness in tabular form or in graphical form. The reader can select the time interval from 1, 5, 10, or all years in the database, measured back from the current period date. The graphical presentation of all years is the most informative for the purposes of the current debate. It clearly shows the prior to the 2008-2009 recession that total federal debt (public holding and intragovernmental) was trending at steady but moderate and had reached a nominal dollar value of just ~ $5 trillion. The financial crisis of 2008-9 and subsequent deficit spending in ensuing years up to Q1-2020 lifted the publicly held nominal dollar debt to ~ $17 trillion, versus ~ $6 trillion (nominal $) for federal intragovernment debt at Q1-2020. The COVID-19 fiscal and monetary blowout from Q2-2020 through to 2/16/2023 hoisted the publicly held federal debt to $24.629 trillion (nominal $) while the intragovernmental obligations increased to $6.828 trillion (nominal $).

Where lies the fault? While the obligations forecast for OASI to social security beneficiaries are concerning for the reasons you cite, neither OASI social security at $2.7 trillion nor the balance of other intragovernmental debt of $4.19 trillion are significant contributors to the current debt problem.

While it is true that the OASI Trust Fund balance will be exchanged for publicly held debt to be issued in future years if the current trends in workforce participation continue unabated, it is not beyond conception that a majority of both houses of Congress decide to act to avoid insolvency of OASI forecast for the year 2032. Congress has done so in past years for Disability Insurance. It could do so again for OASI.

Assuming that Congress does act to prevent insolvency of OASI, then that would leave the publicly held nominal federal debt to be addressed.

While social security is clearly a bugaboo that conservative and republican party politicians object to on a fundamental level as unaffordable "entitlements" needing reform or repeal, social security is not the principal cause of the debt crisis. The more pressing need is to address the federal government General Fund annual primary deficit which has gotten out of control under both principal political parties. The matter is most urgent in light of the increasing assertiveness of the Peoples Republic of China, the unrational behavior of the leadership of Russia and its satellite N. Korea, and the diminishing capability of the U.S. airforce and navy.

You have described SS as it actually operates. As Milton Friedman once said, "It is a chain letter." However, it wasn't sold to the public that way. It was sold, essentially, as a government run annuity program with benefits based on contributions. Many still believe that it operates no differently than a Vanguard fund would. If the program doesn't even attempt to try to act like a real annuity there will be problems in the future. How will benefits be determined: equality or equity? What will getting rid of any pretense that it isn't a welfare program do to the incentive to save for retirement? Since the elderly are the biggest voting bloc when based on actual turnout, politicians will pander to them even more by increasing benefits. As the late economist, Herb Stein, said; "If a trend can't continue, it won't." None of the SS trends can continue, the only question is, Do we have the backbone to implement meaningful reforms before the system blows up and forces draconian changes?

ReplyDeleteWhy are draconian changes necessary? Where do you think money comes from?

DeleteDoes the phrase "full faith and credit" mean anything today, in an American context? I ask this question because of the musings that John has put forward in his blog post, above.

ReplyDeleteAre the "special issue" bonds and certificates held by the various trust funds holding intragovernmental debt issued by the Department of the Treasury not to be held to the same standard as the Treasury securities issued to the American public and foreign investors?

If the Treasury Department, on instructions from Congress, were to dishonor the redemption request of trustees on behalf of the fund on the maturity date of an issue of "special issue bonds" or "special issue certificates", would that not have an impact on the market value of Treasury securities held by the public and foreign governments and institutions? It is hard to credit the argument that it would not. As an event it would certainly end payment of current social insurance benefits (not just social security benefits) immediately to those eligible to receive those benefits. Would the ensuing social costs and social disruption be worth dishonoring the claims on the federal government General Fund held in the various trust funds under the administration of the various trustees legally appointed to oversee those funds?

The trust funds are held to be mere accounting "gimmicks". Are they? In law they are not. If you are proposing to be 'fast and loose' with this law, then what law will you not also be 'fast and loose' with?

On a 'cash flow' basis, the algebra set out in the footnote to the blog post holds on a consolidated account basis. But on a legal basis, it does not hold. Since economists seem to fail to distinguish legal interests of the various agents in the economy, esp. true of 'macro', the solutions offered by economists tend to exist in a metaphysical twin of the real world. If so, then what use is the advice of such thinkers? It cannot be applied in the real world except as a theoretical approximation in policy space. It may serve as a guide in the absence of legal or physical constraints, provided it does not cross societal norms and mores. Otherwise, it exists as a form of art or literature—more philosophical than substantive.

It is not true that the level of federal debt is not a concern. Running a primary deficit while the federal debt publicly held is at 100% +/- of gross domestic product, currently and for the foreseeable future without end, must end in calamity at some point, almost surely. If the FTPL is anything other than a mathematical curiosity, then the level of federal debt and the era of primary deficits must be addressed resolutely if default and dishonor is to be avoided.

I wish the historical part of your chart went back further, because it looks like the "outlays with payable benefits" is reverting back to its historical mean circa 1995-2005.

ReplyDeleteThe following report is illuminating -- "Management's Discussion & Analysis: Financial Report of the United States Government, Fiscal Year 2021." Bureau of the Fiscal Service, Dept. of the Treasury.

ReplyDeletehttps://www.fiscal.treasury.gov/reports-statements/financial-report/mda-unsustainable-fiscal-path.html

Chart 8 and Chart 9 present the Bureau's estimates of the path of expenditures by object and the expected growth in the federal debt held by the public, respectively.

By the numbers in Chart 8:

(A) Primary deficit (% of GDP): -0.8 (1980); -1.1 (2005); -7.4 (2010); -1.2 (2015); -13.3 (2020); -4.7 (2025f); -5.0 (2030f); -5.9 (2035f); -6.2 (2040f); -6.2 (2045f); -6.1 (2050f); &c.

(B) Social security (% of GDP): 4.2 (1980); 4.0 (2005); 4.7 (2010); 4.9 (2015); 5.2 (2020); 5.4 (2025f); 5.8 (2030f); 6.0 (2030f); 6.0 (2035f); 6.0 (2040f); 6.0 (2045f); 6.0 (2050f); &c.

(C) Medicare (% of GDP): 1.1 (1980); 2.3 (2005); 3.1 (2010); 3.0 (2015); 3.7 (2020); 3.6 (2025f); 4.1 (2030f); 4.6 (2035f); 4.9 (2040f); 4.9 (2045f); 4.9 (2050f); &c.

(D) Medicaid (% of GDP): 0.5 (1980); 1.4 (2005); 1.8 (2010); 2.2 (2020); 2.4 (2025f); 2.7 (2030f); 2.9 (2035f); 3.0 (2040f); 3.2 (2045f); 3.2 (2050f); &c.

(E) Total Social Ins. (% of GDP): 5.8 (1980); 7.7 (2005); 9.6 (2010); 9.8 (2015); 11.1 (2020); 11.4 (2025f); 12.6 (2030f); 13.5 (2035f); 13.9 (2040f); 14.1 (2045f); 14.1 (2050f); &c.

(F) Defense spending (% of GDP): 4.8 (1980); 3.8 (2005); 4.7 (2010); 3.2 (2015); 3.4 (2020); 3.2 (2025f); 3.1 (2030f); 3.2 (2035f); 3.2 (2040f); 3.1 (2045f); 3.1 (2050f); &c.

(G) Other non-interest spending (% of GDP): 8.7 (1980); 6.3 (2005); 7.7 (2010); 6.2 (2015); 15.1 (2020); 7.9 (2025f); 8.0 (2030f); 8.0 (2035f); 8.0 (2040f); 8.0 (2045f); 8.0 (2050f); &c.

(H) Interest on debt (% of GDP): 1.8 (1980); 1.4 (2005); 1.4 (2010); 1.2 (2015); 1.7 (2020); 2.3 (2025f); 3.6 (2030f); 6.7 (2035f); 8.7 (2040f); 10.6 (2045f); 12.5 (2050f); 14.4 (2055f); 16.4 (2060f); 18.4 (2065f); 20.5 (2070f); 22.7 (2075f); &c.

(I) Total spending (% of GDP): 21.1 (1980); 19.2 (2005); 23.4 (2010); 20.4 (2015); 31.3 (2020); 24.8 (2025f); 27.3 (2030f); 31.4 (2035f); 33.8 (2040f); 35.8 (2045f); 37.7 (2050f); 39.7 (2055f); 41.7 (2060f); 43.9 (2065f); 46.1 (2070f); 48.4 (2075f); &c.

(J) Total receipts (% of GDP): 18.5 (1980); 16.7 (2005); 14.6 (2010); 18 (2015); 16.3 (2020); 17.8 (2025f); 18.7 (2030f); 18.8 (2035f); 18.9 (2040f); 19 (2050f); 19.1 (2055f); 19.3 (2055f); 19.4 (2060f); 19.6 (2065f); 19.7 (2070f); 19.9 (2075f); etc.

These forecasts paint a picture of Bleak House, a.s. Interest on public debt is forecasted to mount rapidly, rising to 48% of GDP by 2075 and thence continue to rise through 2096 without cease.

Total Social Insurance is forecast to rise to 14.1% of GDP by 2045 and reach a peak of 14.6% by 2077 then fall to 14.1% by 2096. Social security, a component of total social insurance, is forecast to rise to 6.2% of GDP by 2070 and hold at that level until 2082 then gradually decline to 5.9% by 2096.

These forecasts will challenge a 30% tax-exclusive national sales tax rate right out of the box.

By the numbers, at 6% of GDP, social security is not the long-pole in the tent. Total social insurance spending at 14% of GDP should be compared to other OECD members' total of social security, social welfare, and healthcare spending for comparability.

The rate of interest, r , likely exceeds the growth rate, g , for most if not all of the forecast period.

As the publication notes, running a balanced budget going forward is not sufficient. Running a primary surplus is required, for several years if not decades to come. Doing so will require a majority in both houses of Congress. Given the split in the country, a bipartisan majority will have to be formed. In the face of the current emerging external threats, sooner is better than later.

I do appreciate this in light of earlier comments that in no way should the elderly have to bear an equal burden in taxation a la the "fair tax".

DeleteSo if you had a printing press in your garage and could print $1,000 bills legally - would you worry about your Visa bill? Honest question. And if so, why?

DeleteAnon., the Fair Tax Act of 2023 would impose a tax on "old savings" (savings accrued prior to the enactment of the "Fair Tax"). "Old savings" includes fixed capital as well as bank savings account balances and savings held in the form of money market account balances. This defect of the Act has been known since the first introduction of the "Fair Tax" in the 1980s-90s. The 30% tax rate on tax-exclusive prices (retail tax-exclusive prices) was not considered to be sufficient to result in the same amount of revenue raised by the income tax it is proposed to replace. Earlier versions of the "Fair Tax" were examined by economists with experience in public finance and taxation. Two such economists concluded that the 30% tax rate would have to increase to 60% to achieve revenue neutrality with the income tax code that the Fair Tax would replace. So, you see that there are two problems, not just one, with the "Fair Tax". The confiscation of "old savings" that would be achieved under the Fair Tax Act of 2023 is distributed to the well-to-do younger population cohorts (which is what makes the "Fair Tax" attractive to the Republicans), and the 30% tax rate is a "teaser rate", or "come-on" to make the "Fair Tax" palatable in the sense that the tax-inclusive tax rate is 23% of the tax-inclusive price (as though it were a form of income tax). The tax-inclusive tax rate equivalent to the tax-exclusive tax rate of 60%, is 37.5%. Who is paying an average income tax of 37.5% under today's income tax code? Do you see the picture?

DeleteDoDeals, the $1,000 bill is no longer printed (legally) -- it was discontinued in 1969.

Where did that "old savings" come from? Was it not likely the result of 60+ years of transferring wealth from the future through government deficit spending? At some level, you can't just run up the bill and leave the table before everyone else, a great generational "dine and dash" if you will. And, regardless what the rate is, it doesn't matter where the tax legally takes place since incidence of taxation all depends on relative elasticities. Having a 60% tax on your bill will at least let you know how much you are actually paying to the government and will certainly save millions (billions?) for the poorest people who rely on tax preparation services because they are afraid of how complicated the tax code is and how scary the IRS is. That's a net social positive all around for our democracy.

Delete"Where did old savings come from?" Labor.

Delete"Was it not likely the result of 60+ years of transferring wealth from the future through government deficit spending?" One needs to examine when the borrowing occurred. 60 years ago, it was 1963. Our parents (or, grandparents) were working and saving -- include paying off the mortgage as savings. In 2021, the parents (or, grandparents) sold their last house and moved into an assisted living institution. Their accumulated savings included the proceeds of sale of their last house (less taxes on capital gains and title transfer excise taxes) plus the money they had salted away in savings accounts, IRAs, and stock market share holdings. In the course of that 60 year period of time, government spending built highways, ports, airports, and other public goods. All of the public goods that government produced accrue to the following generations, not just the generation that came of age 60 years ago. Even transfers to households (so-called “entitlements”) have produced public goods in the form of a healthier citizenry with less destitution and higher educational attainment than earlier generations that lacked access to those public goods.

Now, it’s common that governments will get carried away with concern for social welfare of their citizens, especially their least endowed citizens and their children. If it is easy to borrow, then where governments face resistance to taxation to provide government resources, borrowing will be resorted to. This occurred during 2008-2020, and 2020-2022, in recent years. From the end of 2007 to the present, the federal public debt to GDP ratio increased from 62.7% to 134.8% (Q2-2020) to 120.2% (Q3-2022). In 13 short years, the federal public debt:GDP ratio doubled. Source: Federal Reserve Bank of St. Louis -- https://fred.stlouisfed.org/graph/?g=YcQu .

Here is a snapshot of this progression: Prior to Volcker's recession (Q3-1981 thru Q4-1982) debt:GDP = 30.7%; at the end of 1995 debt:GDP = 64.2%; at the start of Alan Greenspan's recession (Q1-2001 thru Q4-2001) debt:GDP = 55.1%; at the start of Ben Bernanke's recession (Q4-2007 thru Q3-2009) debt:GDP = 62.7%; at the start of the recent pandemic (Q1-2020) debt:GDP = 107.8%; at the end of Q2-2020 debt:GDP peaked at 134.8%; at Q3-2022 debt:GDP = 120.2%.

When we borrow are we transferring wealth from the future? In the sense that saving is transferring wealth from the present to wealth in the future through investment, one might be tempted to agree, but savings in the present are transferred to governments in the present in exchange for promissory notes that will be paid in the future. Wealth in the future is expected to be greater than wealth in the present and the expectation that the promissory notes will be repaid is therefore the basis of the transfer of wealth from the households that save in the present to households that spend in the present via the mechanism of government borrowing and expenditures.

This is the economic basis of all borrowing, and investment – that the money (savings) advanced to the borrower will be returned with interest in the future. If the contrary held, then all borrowing would be at an end, and government would be compelled to spend less or tax more ("pay as you go"). Perhaps that is our future state.

John,

ReplyDeleteThanks for your insightful posts!

~1.5 years ago, I did a deep dive into SocSec, taking data regarding its liabilities from the 2021 Trustees Report and my historic Treasury rate data, and came with a few standard income cohorts. I did not use any current asset levels and therefore did not have a current deficit #. I look at assumption shocks to estimate a partial difference analysis. Let me know if you want a PDF of my 23 page analysis. Here are the highlights:

Analysis Highlights

1) For Social Security to be economically viable on the marginal, go forward basis (ignoring the accrued to-date funding shortfall), real interest rates need to increase to CPI+2-3%.

2) Yield suppression in the 1940s through mid-1960s was a significant contributing factor of Social Security’s current funding crisis.

3) Systemic suppressing of interest rates since 2000 is a major cause of Social Security’s current funding crisis, and that keep real rates at low levels will make the funding crisis significantly worse.

4) Workers having an average working career shorter than 35-years combined with the income redistribution tiering of benefits are significant sources of the Social Security funding shortfall.

5) Having an income mix of more low-income workers vs. high income will make funding worse.

6) Actual Social Security Dependent Benefits as a ratio of PIA have clearly deceased over time, going from 133% of Retiree Benefit in 1940 to 22% in 2019.

7) Social Security Disability Benefits as a ratio of PIA shows more of a business cycle-based behavior, with a slight increase over time. SSDI benefits peak during recessionary periods.

8) Social Security has a large generational inequity issue, on a PV basis:

a. Birth Years of ~1875-1930 receive much more in benefits than they paid in taxes.

b. Birth Years from late-1940s until mid-1960s receive much less in benefits than they paid in taxes.

c. Benefit/Tax ratios progressively improve for Birth Years after 1960 until ~1990.

9) Benefit/Tax ratios are much better for lower income cohorts than higher income cohorts.

a. Average Benefit/Tax ratios of all post-1920 Birth Years, were:

i. 1000hr/Yr Min Wage: 217%

ii. 2000hr/Yr Min Wage: 159%

iii. Age Median: 110%

iv. National Average: 105%

v. SocSec Max: 76%

vi. 2x SocSec Max: 66%

b. All income cohorts for Birth Years between early-1940s and early-1970s pay more in tax compared to benefits, with the worst being 1958 BY ranging from 10% to 25% (high>low income).

c. No income based life expectancy difference, within reason, will equalize the Benefit/Tax ratios. (I assume highest income cohorts live 6 years longer than the lowest income cohort.)

10) Factors that drive Benefit/Tax ratios higher (& Surplus lower) are:

a. Birth Years which had low FICA tax rates and low taxable maximums

b. Birth Years which had more generous benefit calculation rules

c. Low wage income

d. Low real interest rates during working years

e. Low real interest rates at FRA

f. Shorter working careers

g. Longer lifespan

h. High percentage of single wage earner household with dependents

i. High percentage qualifying for SSDI Disability Income

Birth years of the 1950s-1960s receive much less from Social Security than other generations because of several factors: most or all of their work history had high FICA tax rates, high Social Security maximum wage limits, higher Social Security benefit age (FRA), benefits being taxed at an increasing level, and high real interest rates (opportunity cost) during their early work history. The birth year with the absolute worst benefit/tax ratio is 1958, after which benefit/tax ratios start to improve, as less and less of their FICA withholding is done in years with high real interest rates.

ReplyDeleteThe benefit ratio deterioration starting in 1990 BY is due to my assumption of gradual normalization of real interest rates (starting from mid-2021 low rates).

Estimates for birth years after 1960 get more and more speculative, as I assume future CPI, wage growth, and interest rates move towards an assumed “normal” levels of: 2% CPI growth, 0.80% real wage growth, and 4% T30Yr rates by 2030.

Such total nonsense. Like alot of doggies with small paws, the Grump is measuring the wrong things. The Federal Debt is totally irrelevant. It doesn't even have to be measured, much less reported breathlessly. Of course the Fed can buy up all the securities necessary to fund whatever Congress legislates. The limitation is the current spending vis a vis the productive capacity of the economy, as measured by inflation. Really? We're going to run out of resources to produce what the geezers are buying? Really???? What? Shuffleboards? Cable prescriptions? Cat food? Such total Grumpy nonsense.

ReplyDeleteYour entire economic theory is self-serving. You work in the world of raising funds for people, and the sure way to be able to raise funds is to ensure loose monetary policy and a bunch of deficit financing. Your entire ploy is to make money today, telling people that the "sovereign can just print more money", use that money to buy assets to hedge against the inevitable inflation and over all just hope it doesn't get too bad before you leave the country. Why should we believe anyone who acts like a Twitter crypo shill bot?

DeleteTwo thoughts I have had for a while now:

ReplyDelete1. how inflation and current monetary policy (higher rates) affect the projected deficit. Specifically, if inflation rises to meet current interest rates (which is one theory), seems the future deficit goes exponential at a higher order with COLAs.

2. Any opinions on whether reality will hit and a return to tax brackets of the immediate post WWII period will repeat (up to 91%)?

The sovereign, like the US, can:

Deletea. issue currency to spend and buy anything the economy produces,

b. up to the productive capacity of the economy (adjusted for turnover/velocity),

c. without creating inflation.

In other words the US government can issue currency and hire any and all unemployed and underemployed folk. The constraint is the productive capacity of the economy, as measured by wage inflation. If prices do rise above an acceptable level, they can be controlled by i) selling government securities, ii) raising interest paid on deposits at the fed, iii) raising taxes across the board (on income, sales/vat, and asset values), or iv) a cut in spending.

The MMT Inflation policy tool:

Inflation is easily managed through several tools including

1) down payment and margin requirements on real estate and securities,

2) targeted supply chain actions, and

3) broad based tax increases/decreases.

For example, the Job Gty/Green New Deal law should include AUTOMATIC across-the-board tax increases that kick in when certain monthly wage inflation targets are hit-say for 6 months in a row. These can include:

a) Income Taxes,

b) Sales/VAT Taxes

c) Asset Value (or Wealth) Taxes

That'll cool things off pronto. When inflation has cooled, the taxes automatically return to a base level.

Easy Peasy.

Why is the projected "deficit" (private sector surplus) a problem? Why are we even discussing it. It's irrelevant. Current interest rates have a stimulative effect - injecting net financial assets into the private sector - but also depressive effect - downward pressure on real estate prices, credit card spending, and fixed asset investment. A mixed bag. Why would inflation necessarily rise to meet interest rates?

Delete"The sovereign, like the US, can:

Deletea. issue currency to spend and buy anything the economy produces,

b. up to the productive capacity of the economy (adjusted for turnover/velocity),

c. without creating inflation"

Such total nonsense. Like alot of doggies with small paws.

"Why would inflation necessarily rise to meet interest rates?"

DeleteJohn has already explained this in great detail. If you can't be bothered to educate yourself, there is no point in continuing.

Because it worked so well for Argentina

DeleteMy wife and I are reasonably well off. We get more money from Social Security every year than we pay in Federal taxes. Some of that Social Security money is hers, even though she paid Social Security taxes for only a few months (public school teacher back when they weren't covered.) I'm not complaining, but this seems strange.

ReplyDeleteMy impression, though I don't have data, is that Medicare is in even more serious straits than Social Security, and it's a program which, unlike Social Security, wouldn't benefit much from raising the eligibility age.

It still puzzles me why the government doesn't run an actual independent pension scheme with a diversified asset pool.

ReplyDelete