At the AEI fiscal theory event last Tuesday Tom Sargent and Eric Leeper made some key points about the current situation, with reference to lessons of history.

Tom's comments updated his excellent paper with George Hall "Three World Wars" (at pnas, summary essay in the Hoover Conference volume). Tom and George liken covid to a war: a large emergency requiring immense expenditure. We can quibble about "require" but not the expenditure.

(2008 was a little war in this sense as well.) Since outlays are well ahead of receipts, these huge temporary expenditures are financed by issuing debt and printing money, as optimal tax theory says they should be.

In all three cases, you see a ratcheting up of outlays after the war. That's happening now, and in 2008, just as in WWI and WWII.

After WWI and WWII, there is a period of primary surpluses -- tax receipts greater than spending -- which helps to pay back the debt. This time is notable for the absence of that effect.

We see that most clearly by plotting the primary deficits directly. The data update since Tom and George's original paper (dots) makes that clear. To a fiscal theorist, this is a worrisome difference. We are not following historical tradition of regular, full employment, peacetime surpluses.

The two world wars were also financed by a considerable inflation. The important consequence of inflation is that it inflates away government debt. Essentially, we pay for part of the war by a default on debt, engineered via inflation.

1947 is an interesting case. As now, inflation broke out, the Fed left interest rates alone, and the inflation went away once it had inflated away enough debt. That too is an interesting episode in the debate whether the Fed must move rates more than one for one to keep inflation from spiraling away.

The effect of inflation is clearer in the next graph, which plots the real return on government bonds:

Yes, the inflation of 1920 did inflate away a lot of the WWI debt, though the deflation of 1921 brought a lot of that back. (This is an episode we would do well to remember more! The price level

doubled from 1916 through 1920. It then retreated by a third in 1920-1921. There was a sharp recession, but the economy recovered very quickly with no stimulus or heroic measures. The conventional wisdom that wringing out WWI inflation caused the UK 1920s doldrums needs to consider this counterexample. But back to our point)

This is also consistent with standard optimal tax theory, which says that in the event of a disaster that happens once every 50 years or so, it is right to execute a "state contingent default" (Lucas and Stokey), and inflation is a natural way to do it.

But... "state contingent default" is supposed to happen at the beginning of a war. These inflations happened at the end of the war. How did governments sell bonds to people who should have expected them to be inflated away? Yes, there were some price controls and financial repression, but it's still an important puzzle to standard public finance theory.

My concern, of course, is that we've had two once in a hundred year events in a row (2008, 2020), I can think of lots more that might come soon, and you can only do this occasionally. Hit people over the head a few too many times and they start to duck. We will head to the next crisis with no history of steady surpluses in good times, 100% debt to GDP ratio, and a painful reminder of what happens if you lend to the US right in the rear view mirror.

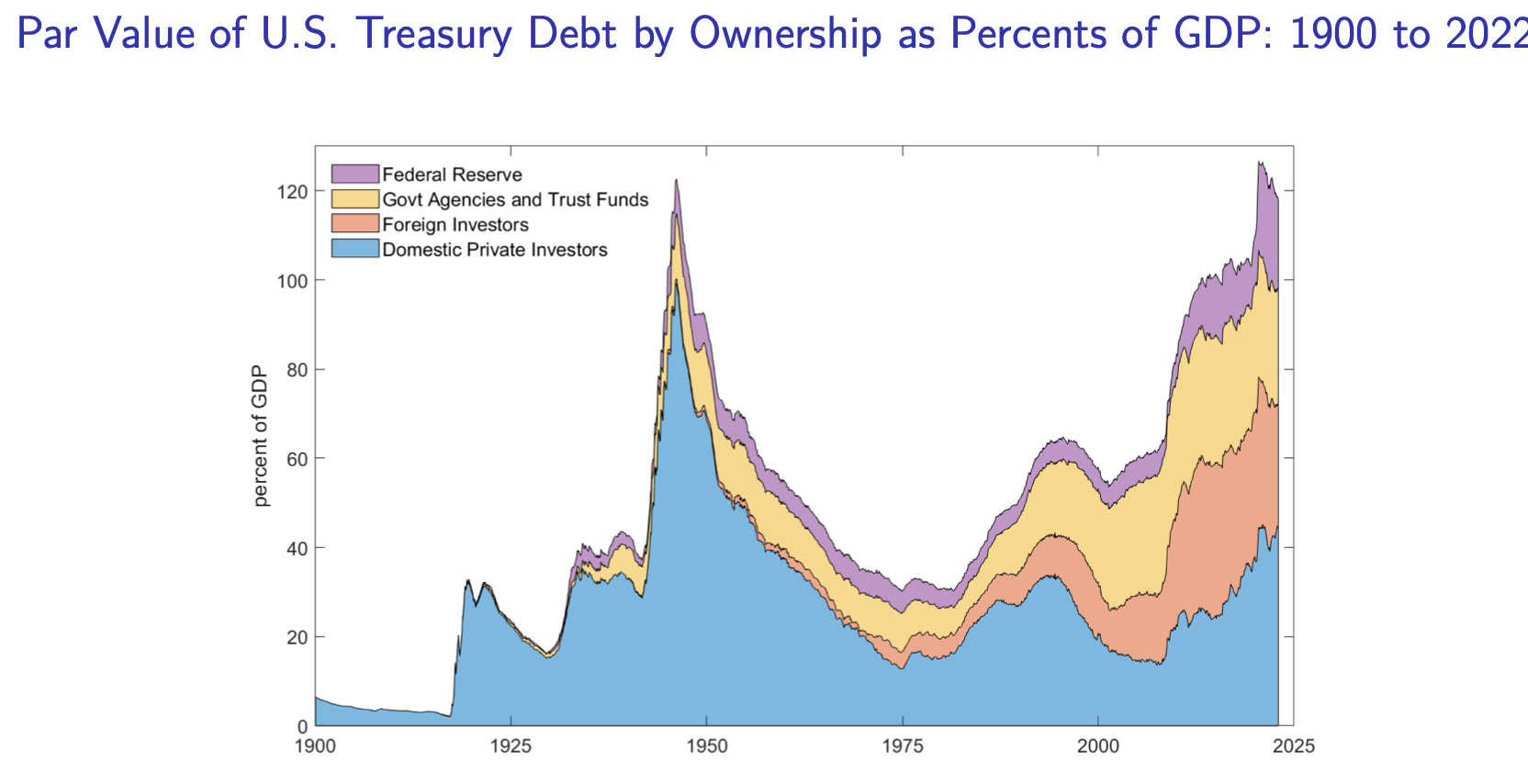

We start the H5N1/Taiwan war crisis with the same debt we had at the end of WWII. And who owns the debt leads to some fascinating speculation which I'll let you fill in with your chat GPT.

Tom closed by echoing my favorite bright idea for avoiding the debt limit: Since the limit applies to par value not market value, the Treasury can issue all the perpetuities it wants. That's far better than the trillion dollar coin, though I suspect the Supreme Court would take just as dim a view of it.

Eric brought up a great point from his super

Recovery of 1933 paper with Margaret Jacobson and Bruce Preston.

In 1933, we had a disastrous deflation. The gold standard is a lovely fiscal commitment device to try to contain inflation, but it has an Achilles heel. If there is a deflation, the government has to raise taxes to pay an unexpected real windfall to bondholders. In 1933, the Roosevelt Administration abrogated the gold standard. It was a default on the legal terms of the bonds. And look what happened to inflation!

Eric also brought up a second central point of his 1933 paper: The Roosevelt Administration separated the budget into a "regular" budget, in which we should expect deficits to be paid back, and an "emergency" budget, unbacked (in our language) by expected surpluses. That cleverly allowed inflationary finance in 1933, but once the "emergency" was over in 1941, it preserved the US reputation for repaying wartime debts with subsequent surpluses, and allowed it to borrow for WWII. This loss of "back to normal," of expectations that we are now in "regular" not "emergency" finance is worrisome today.

Finally, Eric brought some nice evidence to bear on the question, why 2020 but not 2008? Well, in part, we can look at statements of public officials. In 2008, they explicitly said, deficit now, repayment later. In 2020 they explicitly said the opposite.

("Offsets" is Washington-speak for "taxes" or later spending cuts.) Don't read a pejorative in this analysis. If you want to borrow, finance crisis expenditures and not create inflation, you "maintain the norm." If you want to create a "state contingent default" and pay for crisis expenditures by inflating away debt, you have to "violate the norm." That is darn hard -- ask the Japanese. How do you convince people you're not going to repay some part of the debt, despite a good reputation, but just some part, and if WWII comes along you're good for additional debts? Well, announcing your intentions helps!

And it worked. We very quickly inflated away the debt. Creating a state contingent default via inflation is not easy. Still to be seen though is whether we can return to "normal" "Hamilton norm" once it's over.

Robert Barro also had great comments, but more directed at the book and with no great graphs to pass along. Thanks anyway!

"But... "state contingent default" is supposed to happen at the beginning of a war. These inflations happened at the end of the war. How did governments sell bonds to people who should have expected them to be inflated away?"

ReplyDeletePeople are contractually obligated to accept government debt in exchange for good/services. I feel like this is in part an extension of the question "Why are prices sticky?". Also price controls/optics around raising prices during a war.

Rational actors will always exchange bonds for money regardless of the government's fiscal stance.

Interestingly I think to create a "state contingent default" the government has to either have very high credibility or no credibility at all.

Your point that we should see a strategic default at the beginning and not the end is interesting but in this case who was the patsy that "bought the debt" that was to be inflated away? Well, it was the Fed and they are basically in on the joke so it doesn't neatly fit the usual model. A simpler and somewhat more traditional interpretation is simply that the UST borrowed a ton of money, the Fed financed it by printing money (reserves), and inflation re-established balance in the "equation of exchange". Understanding that IOR makes the analysis a little different I think the basic point here is largely correct and not all that complex.

ReplyDeleteSeems to me rather the result of discretion, which is of course state dependent, rather than preset returns that are functions of states (which to me are the defining feature of state contingency). If anything, the very fact that people did not seems to anticipate it show that we're talking about discretion.

ReplyDelete“I would be very pleased if the data we receive on inflation and the labor market this month show signs of moderation. But wishful thinking is not a substitute for hard evidence in the form of economic data.”

ReplyDelete— Fed governor Christopher Waller (quoted in the The Wall Street Journal, 3/3/2023).

It would appear that FRB governor Waller is an 'adaptive expectations' decision-maker. The 'data' that he is relying on as a basis of his decision-making is derived from activities that took place in the past. On the lessons from John's lectures (here) and his recent publication (celebrated in the two video-tapped discussion published in his last blog post), should we expect the inflation to spiral away (instability) in accordance with the predictions of instability arising from adaptive expectations in the new-Keynesian DSGE models in his earlier blog posts?

It will certainly be interesting to watch the results come in going forward from where we are today.

In another article published in today's The Wall Street Journal, Prof. Furman (Harvard) is advocating for a 50 basis-point rise in the Fed-funds rate this month. He bases this advocacy on the annualized trailing 3-month change in the price level through January of this year, and what he perceives to be the inflationary effect of job position openings in excess of the numbers of unemployed workers potentially available to fill those openings. He also adds that the annualized 5% growth rate in the (weighted-)average wage rate is compatible with a 4% annualized rate of inflation but incompatible with a the FOMC's target PCE inflation rate of 1% to 3% per annum (2% central target rate). Mr. Furman asserts that the FOMC should lift the 'ceiling' of the Fed-funds rate to 6% per annum and ramp up the rate increases to achieve that level in the shortest period practicable. He likens the situation to 1980-1 which led to the recession of 1981-2 (the 'Volcker recession').

ReplyDeleteThe simple and fundamental premise of the fiscal theory of inflation is well-founded in the historical record of past inflationary periods and fiscal deficits. Central banks have very few tools with which to manage ('control') inflationary expectations when fiscal deficits drive inflationary periods. In 2020 central banks doubled down on the supply of liquidity to financial markets. The double effect of fiscal deficits and central bank injections of liquidity into financial markets caused inflationary pressures to double-up. Jaw-boning by politicians (cf., Obama’s promise is cited in the slide headed "The Hamilton Norm") may help shape expectations but that is small beer when the same politicians fail to deliver (as Obama failed to deliver) on fiscal surpluses. In the present case (Trump-Biden) we have seen the head of state (Trump) jaw-bone the central bank (Powell) to continue providing liquidity to the financial markets, and the current head of state (Biden) jaw-bone Congress to pass legislation that increases the fiscal deficits.

The historical record is replete with inflationary periods stoked by political decisions that continued fiscal deficits, driving the deficits deeper. The current outlook is negative.

If Mr. Furman is correct in his fears for inflation, we may be looking forward to inflation rates centered on 4% per annum, rather than centered on 2% per annum.

That is far cry from the 12%/yr. that prevailed in the early-mid '70s of the 20th Century, or the 18%/yr. that Volcker wrestled down to high single-digits in the 1980-5 period. All things are relative to expectations. We lived through the '50s, '60s, '70s, '80s, and '90s and survived. The fiscal challenges we face in the 2020's are significant, but no more so than in the 1970's to the 2000's.

What the Fiscal Theory of the Price Level informs us is just what history has taught us. Tame inflation by running fiscal surpluses. Not just the expectation of future fiscal surpluses, but fiscal surpluses in fact.

"Windfalls" to holders of Treasury bills, notes and bonds, are simply the penalty we pay for being profligate and spend-thrift in earlier periods.

ReplyDeleteThe ideal target for the rate of inflation is zero (+/- 1 percentage point), according to the new-Keynesian DSGE model.

ReplyDeleteAt zero inflation, the 'output gap', x, goes to zero, and the rate of interest goes to the rate of time preference ( - log(Beta)). The rate of unemployment goes to the natural rate of unemployment (Okun's Law).

What could be simpler? This is theory. The real world stuff is a shade more complex. Nevertheless, if the new-Keynesian DSGE holds, this is the ideal that should be strived for.

During the discussion, Eric Leeper remarked on the situation of Great Britain during the post-war period 1918-1925, or thereabouts, suggesting that period in Great Britain’s monetary history would be a fruitful source of research viz. the fiscal theory of the price level.

ReplyDeleteThe following passages quoted from Chapter VIII “The Problem of Exchange Rates: The Gold Standard”, pp. 152-156, in Monetary Theory and Practice, J. L. Hanson, 1957, London: Macdonald & Evans, Ltd., describe the circumstances and the policy environment in Great Britain during the 1920s.

“Great Britain in effect left the gold standard on the outbreak of war in 1914, but this fact was not openly acknowledged until the end of the war. Inflation during that war reduced the internal value of the pound, although the external value did not fall to the same extent. That this country would return to the gold standard after the war was generally anticipated, and the Cunliffe Committee, whose Interim Report appeared in 1918, recommended that this course should be adopted as soon as conditions allowed.

“Few people disagreed with this proposal at the time, but there was less agreement on the question of the value to be given to the pound when it came to be linked to gold. Should the pound be given its pre-war parity of 4.86 ²/₃ U.S. dollars, or should it be devalued to a parity more in keeping with its internal purchasing power? In the light of after events the answer to this question is clear; it was less clear to the British monetary authorities at the time. The difficulties of Great Britain in the decade 1921-31 were at least seriously aggravated by the decision to return to gold at the pre-1914 parity. Nevertheless, the motives which inspired this decision are understandable. Before 1914 this country had been the financial centre of the world, a position from which it derived a considerable “invisible” income. To restore Great Britain to this position seemed to be a first essential of post-war policy, and it was thought that this country’s prestige required it to show that it was financially sound enough to resume its former role. Only a return to the gold standard at the old parity, it was felt, would make this clear to the rest of the world.

“... there was some inflation as a result of which the value of the pound had depreciated and the national debt had increased by ten times, ... this country had fought the war without having to increase its net borrowing abroad (the amount borrowed from the United States was less than Britain had lent to its Allies), and apart from a loss of gold to the United States and capital losses in Russia, there had been no depletion of its foreign investments.”

“It was the internal situation which showed this policy to be mistaken. To return to the gold standard at the old parity required the internal value of the pound to be raised, and this involved a reduction of prices and the volume of purchasing power—that is, deflation. The result was a sharp end to the brief post-war boom, and unemployment quickly followed.”

“Maldistribution of gold among the countries on the standard left many of them with inadequate reserves. The United States had too much; other countries had too little. Gold was fixed at the pre-1914 price, but nearly all other prices were very much higher. Consequently, credits or debits in the balances of payments, even if no larger in volume than before, represented a much larger quantity of gold. ... Throughout the period of the restored standard Great Britain, although it held three times as much gold as in 1913, was hampered by its inadequate gold reserves. The amount of deflation required to ease the strain was greater than the country’s economy could bear.”

In the 1920s it was more difficult to carry out a policy of deflation: trade unions were able to resist efforts to reduce wages; “... unemployment was already severe, and to push deflation further could only deepen the depression.”

When is a temporary loan no temporary? When the issuer things they have an open check book and creditors accept the debt; but there eventually is a cost to such behavior. Sadly, the American public elects economically and financial ignorant people to Congress. And economists in the Administration buy in to the party line and drink the cool-ade.

ReplyDeleteWhat do you propose is the mechanism for central banks to "get the memo" that fighting inflation takes a back seat to inflating away debt?

ReplyDeleteIs it explicit Treasury influence? Is it that the financial system becomes unstable? Does it become difficult to sell debt? Does unemployment rise quickly with such a backdrop?

"In 1933, the Roosevelt Administration abrogated the gold standard. It was a default on the legal terms of the bonds. And look what happened to inflation! "

ReplyDeleteI don't want to put words in your mouth, but I'm assuming you mean to say that it was this "default" that lead to inflation as the price level adjusted per the FTPL.

Given that assumption, I pulled out my trusted copy of "A Monetary History" by Friedman and Schwartz to one of their wonderful, pullout graphs (p 678 in my edition) and noted that the rate of increase in the monetary base increased noticeably at this same time along with the money stock (as F&S measure it). Given this, surely at least part of the benefit of going of the gold standard was not that it was an implicit default but rather that it freed up the Fed to increase the monetary base (though arguably they could have done this regardless). Or was this just a happy coincidence?

- Foam-flecked economist

"The two world wars were also financed by a considerable inflation. The important consequence of inflation is that it inflates away government debt. Essentially, we pay for part of the war by a default on debt, engineered via inflation." -- JHC.

ReplyDelete"... engineered via inflation." ?

The design and production of gliders (a form of aircraft) is engineered. The glider's tug (another form of aircraft) is engineered. The M1A1 "Abrams" tank is engineered. The F-35 interceptor is engineered. A cyclotron is engineered, as is an oil refinery producing motor fuels and lubricants. Economic policy is not engineered, though it may contrive to effect specific policies bearing on economic decisions in financial and real markets in a way that favors certain special interests over others.

Contrive (v.) is the better choice, rather than engineer (v.), when it comes to politics and economics. Viz., "The government contrived an inflation to ensure a soft default on its debt obligations to creditors, and to spare its taxpayers the pain of higher remittances to pay the 'butcher's bill'--the debt incurred to pad their investment accounts and avoid penury during the recent war (pandemic, &c.)"

It would be of interest to examine the Biden administration's proposed budget provisions through the lens of the fiscal theory of the price level. The proposed budget (yet to be published) is said to provide for $3 billion in deficit reduction while retaining the 2017 Trump-Ryan tax cuts for households with adjusted gross incomes of $400,000 or less.

ReplyDelete