Torsten's conclusion:

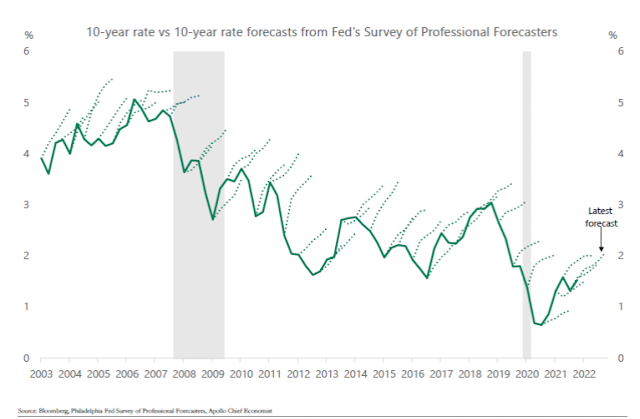

The forecasting track record of the economics profession when it comes to 10-year interest rates is not particularly impressive, see chart [above]. Since the Philadelphia Fed started their Survey of Professional Forecasters twenty years ago, the economists and strategists participating have been systematically wrong, predicting that long rates would move higher. Their latest release has the same prediction.

Well. Like the famous broken clock that is right twice a day, note the forecasts are "right" in times of higher rates. So don't necessarily run out and buy bonds today.

Can it possibly be true that professional forecasters are simply behaviorally dumb, refuse to learn, and the institutions that hire them refuse to hire more rational ones?

My favorite alternative (which, I admit, I've advanced a few times on this blog): When a survey asks people "what do you 'expect'?" people do not answer with the true-measure conditional mean. By giving an answer pretty close to the actual yield curve, these forecasters are reporting a number close to the risk-neutral conditional mean, i.e. not \(\sum_s\pi(s)x(s)\) but \(\sum_s u'[c(s)]\pi(s)x(s)\). The risk-neutral mean is a better sufficient statistic for decisions. Pay attention not only to how likely events are but how painful it is to lose money in those events. Don't be wrong on the day the firm loses a lot of money. The weather service also tends to overstate wind forecasts. I interpret the forecast of 30 mph winds as "if you go out and capsize your boat in a 30 mph gust, don't blame us." "If you buy bonds and they tank, don't blame us" surely has to be part of a finance industry "forecast."

If the risk-neutral mean equals the market price, do nothing. And do nothing has to be the advice to the average investor. Reporting the forecast implied by the yield curve directly has a certain logic to it.

Economists rush too quickly, I think, from surveys where people are asked "what do you expect?" to bemoaning that the answers do not represent true-measure conditional means, and blaming that on stupidity. As if anyone who answers the question has the vaguest idea what the definitions of mean, median, mode, conditional and true vs. risk-neutral measure are. We might have a bit more humility: They're giving us a sensible answer, to a question posed in English, but since we asked the question in a foreign language, it is an answer to a different question.

(Teaching is good for you. Most of my students did not understand that "risk" can mean you earn more money than you "expected," at the beginning of the class. I hope they got it by the end! But they were not wrong. In English, "risk" means downside risk. In portfolio analysis, it means variance. Know what words mean.)

But that also means, do not interpret the answers as true-measure conditional means!

This graph is particularly challenging since it concerns the 10 year rate only. Similar graphs of short-term rates also show consistent bias toward forecasting higher rates that don't happen. But that is more excusable as a risk-neutral mean, since the yield curve slopes up in the first few years. A rising forecast of 10 year yields corresponds to slope from 10 years to longer maturities, which is typically smaller. Torsten, if you're listening, a comparison to the forecast implied by the forward curve at each date would be really interesting!

***

Update: The same students who used the English meaning of "risk" to be "downside risk" also used the English meaning of "expected" to be "what happens if nothing goes wrong," somewhere in the 90th percentile. The two meanings do make some sense, properly understood, especially in a world with skewed distributions -- the lion gets you or does not, the plan crashes or does not, the bomb explodes or does not. Many important distributions are not normal, so mean and variance aren't appropriate!

I don't mean to say that surveys are useless. They are very important data, that can be very useful for forecasting events. If the survey forecast points up, that tells you something. A forecasting regression that includes survey data can be very useful. Just don't interpret it directly as conditional mean and blather about irrationality if it isn't.

The variation across people in survey forecasts is the really interesting and under-studied part of all this. The graph is the average forecast across forecasters. But individual forecasters say wildly different things. Even these, who are professional forecasters. Why do survey forecasts vary across people so much, though the people have the same information? Why do trading positions not vary over time or across people anything like the difference between survey forecasts and market prices says they should? I think we're missing the interesting part of surveys -- their heterogeneity, with little heterogeneity of actions.

As it was explained to me: forward curves allow you to bet against the consistency of your counterparty's trades, not their accuracy

ReplyDeleteFor the last 40 years, the macroeconomics profession has expected higher rates of inflation, thus higher nominal interest rates. Instead, we saw disinflation and lower rates.

ReplyDeleteThe last year has been most welcome in the profession.

“The risk-neutral mean is a better sufficient statistic for decisions” is there a resource for a formal theory of sufficient statistics (including risk neutral means) in decision theory? Or are you using sufficient statistic loosely?

ReplyDeleteWould be interesting to see this graph over a long period of rising interest rates.

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteThe 10 yr bond interest rate forecasts are available for analysis at:

ReplyDeletehttps://www.philadelphiafed.org/surveys-and-data/tbond

The forecasts of the individual forecast professionals can be downloaded as an Excel file. Mean and median statistics are also available in Excel format but, as summary statistics, these measures are less useful for purposes of analysis of forecasting accuracy, e.g., (expected minus actual)/actual.

Forecasts are given by calendar quarter, enabling analysis of dynamic recalibration by individual forecaster. The result is greater "color" in the data available to the data analyst.

Torsten Slok's remark is hardly newsworthy. Forecasts are usually taken with a grain of salt. It is not the mean, or the median, forecast that is useful, but the individual forecaster whose forecasting ability has demonstrated a consistent record of accuracy that is worth listening to. Find that individual or handful of individuals and pay attention to their estimates and expressed expectations. The forecast survey data, not the statistical measures, is the critical information.

This is a GREAT graph and great post. I have grabbed this chart and shared it with friends on numerous occasions whenever we speak of inflation/rates and they go into...but the market isn't expecting...

ReplyDeleteBroader question - what does a chart say about standard economic theories that depend on correct long-run expectations - should we still be making predictions based on P=E[mX] when "E" can be so screwed up for so long....? Of course we can re-classify the mistake into "the required rate of return" but that seems so unappealing.

I think you are missing the point: long run expectations are already embedded in the price, but that price also embeds the cost of risk. You can't distill true expectations unless you have a perfect pricing model that can calculate the price of risk.

DeleteAs a shorthand, media and market participants refer to "market expectations" all the time. Knowingly or not, those are only pseudo expectations, accurate solely in a risk neutral world. Forecasters, intriguingly, seem to do the same thing.

Very interesting graph. When I was at Booth I did a paper on market sentiment/forecasters and correlation with the following periods of market movement. It was focused on the short term in commodity markets, but sentiment was generally correlated well with the previous period--recent rally, expect more of the same. The only forecasters with good records were forecasters in markets with positive serial correlation (long trends).

ReplyDeleteThis "broken clock syndrome" is interesting in the long run. And I've had my issues with the wind forecasts from NOAA as well. As a devout windsurfer, I grew frustrated with the forecasts always well above the measured windspeeds. I even did an unscientific study and contacted NOAA about the perils of crying wolf. No reply, but forecasts today are much more accurate than in the past.

https://www.vwl.uni-mannheim.de/media/Lehrstuehle/vwl/Adam/AdamMatveevNagel_JME.pdf

ReplyDeleteThis JME paper shows quite convincingly that your explanation of risk-neutral or pessimistically-tilted expectations cannot be correct.

This comment has been removed by the author.

ReplyDelete